Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a discrete time formulation of the semi martingale optimal transport problembased on multi-marginal entropic transport. This approach offers a new way to formulate and solve numerically t...

We propose machine learning methods for solving fully nonlinear partial differential equations (PDEs) with convex Hamiltonian. Our algorithms are conducted in two steps. First the PDE is rewritten i...

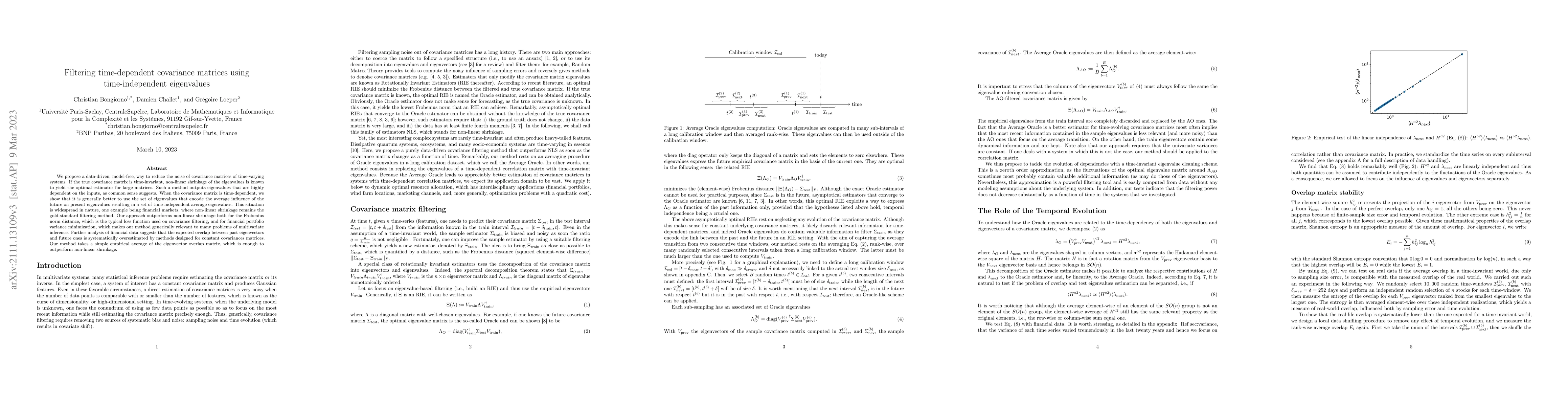

We propose a data-driven way to reduce the noise of covariance matrices of nonstationary systems. In the case of stationary systems, asymptotic approaches were proved to converge to the optimal solu...

In a multi-dimensional diffusion framework, the price of a financial derivative can be expressed as an iterated conditional expectation, where the inner conditional expectation conditions on the fut...

We propose two deep neural network-based methods for solving semi-martingale optimal transport problems. The first method is based on a relaxation/penalization of the terminal constraint, and is sol...

Using Dupire's notion of vertical derivative, we provide a functional (path-dependent) extension of the It\^o's formula of Gozzi and Russo (2006) that applies to C^{0,1}-functions of continuous weak...

This paper studies a portfolio allocation problem, where the goal is to prescribe the wealth distribution at the final time. We study this problem with the tools of optimal mass transport. We provid...

The recently developed rough Bergomi (rBergomi) model is a rough fractional stochastic volatility (RFSV) model which can generate more realistic term structure of at-the-money volatility skews compa...

This paper addresses the problem of utility maximization under uncertain parameters. In contrast with the classical approach, where the parameters of the model evolve freely within a given range, we...

The calibration of volatility models from observable option prices is a fundamental problem in quantitative finance. The most common approach among industry practitioners is based on the celebrated ...

We propose a discrete time formulation of the semi-martingale optimal transport problem based on multi-marginal entropic transport. This approach offers a new way to formulate and solve numerically th...

Entropic Optimal Transport (EOT), also referred to as the Schr\"odinger problem, seeks to find a random processes with prescribed initial/final marginals and with minimal relative entropy with respect...

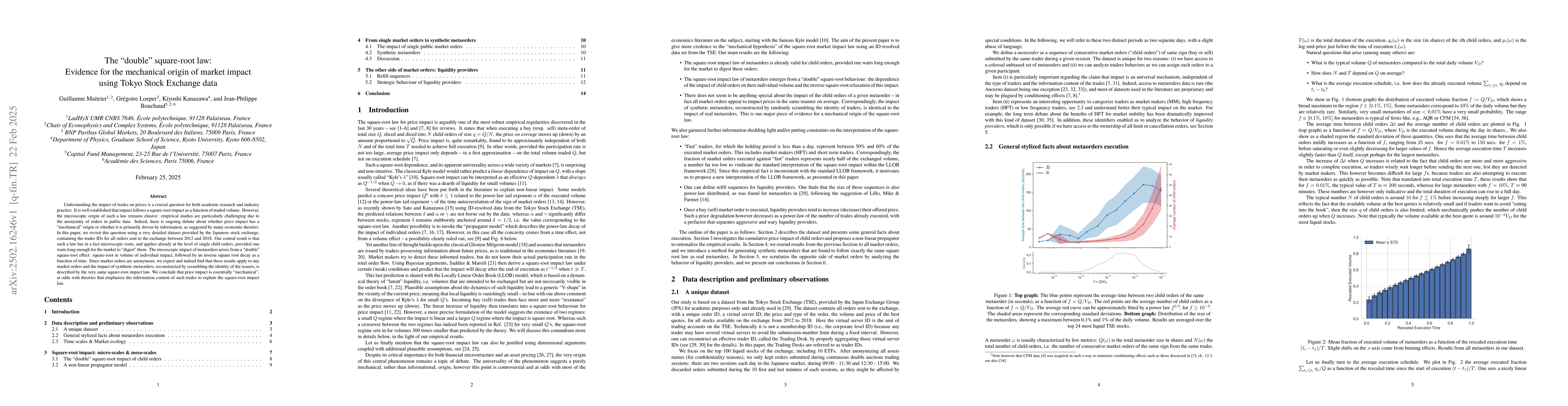

Understanding the impact of trades on prices is a crucial question for both academic research and industry practice. It is well established that impact follows a square-root impact as a function of tr...

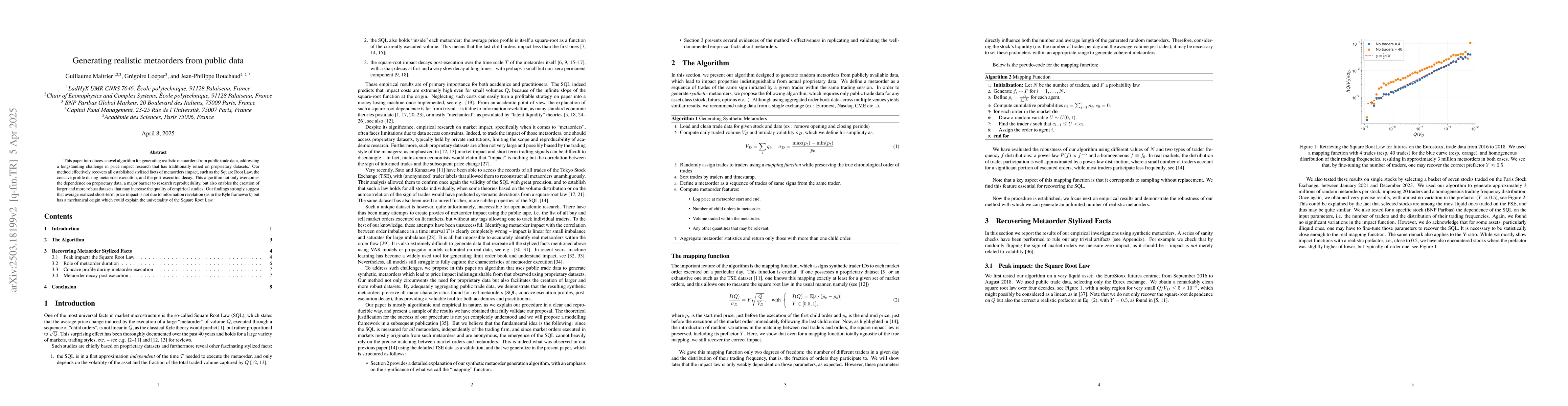

This paper introduces a novel algorithm for generating realistic metaorders from public trade data, addressing a longstanding challenge in price impact research that has traditionally relied on propri...

This work extends and complements our previous theoretical paper on the subtle interplay between impact, order flow and volatility. In the present paper, we generate synthetic market data following th...

This short paper announces the main results of \cite{SBB2026}, where the Schrödinger--Bass Bridge (SBB) problem is introduced and studied in full generality. Here we provide a direct PDE derivation of...

The Schrodinger Bridge and Bass (SBB) formulation, which jointly controls drift and volatility, is an established extension of the classical Schrodinger Bridge (SB). Building on this framework, we int...

We study a semimartingale optimal transport problem interpolating between the Schrödinger bridge and the stretched Brownian motion associated with the Bass solution of the Skorokhod embedding problem....

We study the problem of generating synthetic time series that reproduce both marginal distributions and temporal dynamics, a central challenge in financial machine learning. Existing approaches typica...

The multidimensional Uncertain Volatility Model leads to robust option pricing problems under joint volatility and correlation uncertainty. Their numerical resolution quickly becomes challenging becau...