Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a new autocorrelation measure for functional time series that we term spherical autocorrelation. It is based on measuring the average angle between lagged pairs of series after having bee...

We consider the problem of consistently estimating the conditional distribution $P(Y \in A |X)$ of a functional data object $Y=(Y(t): t\in[0,1])$ given covariates $X$ in a general space, assuming th...

The cumulative sum (CUSUM) process is often used in change point analysis to detect changes in the mean of sequentially observed data. We provide a full description of the asymptotic distribution of...

Motivated by the goal of evaluating real-time forecasts of home team win probabilities in the National Basketball Association, we develop new tools for measuring the quality of continuously updated ...

For sequentially observed functional data exhibiting multiple change points in the mean function, we establish consistency results for the estimated number and locations of the change points based o...

This paper deals with two-sample tests for functional time series data, which have become widely available in conjunction with the advent of modern complex observation systems. Here, particular inte...

Invertible processes naturally arise in many aspects of functional time series analysis, and consistent estimation of the infinite dimensional operators that define them are of interest. Asymptotic up...

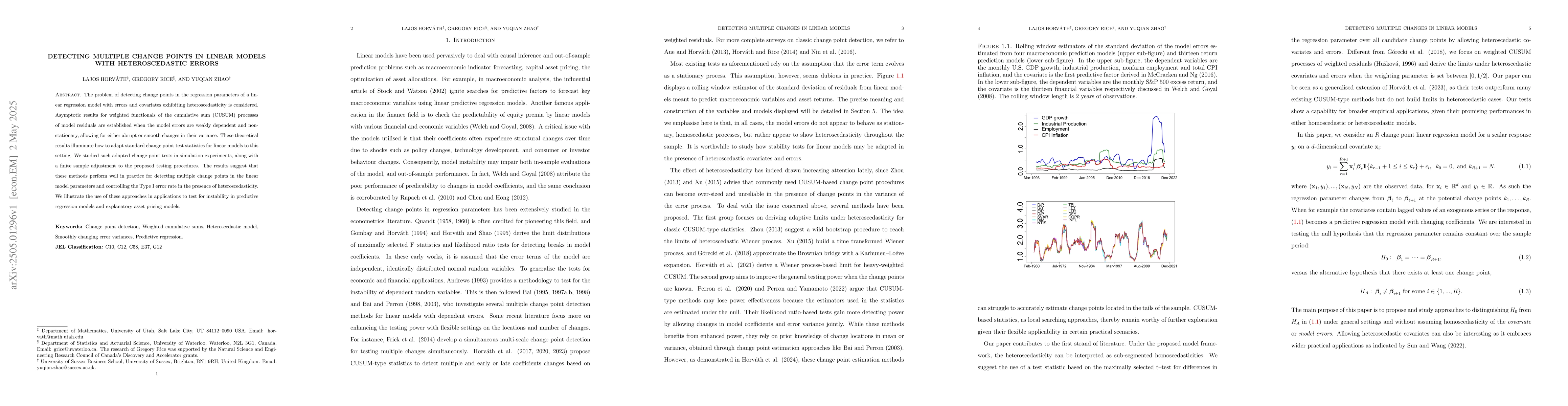

The problem of detecting change points in the regression parameters of a linear regression model with errors and covariates exhibiting heteroscedasticity is considered. Asymptotic results for weighted...

AutoRegressive Conditional Heteroscedasticity (ARCH) models are standard for modeling time series exhibiting volatility, with a rich literature in univariate and multivariate settings. In recent years...