Academic Profile

Statistics

Similar Authors

Papers on arXiv

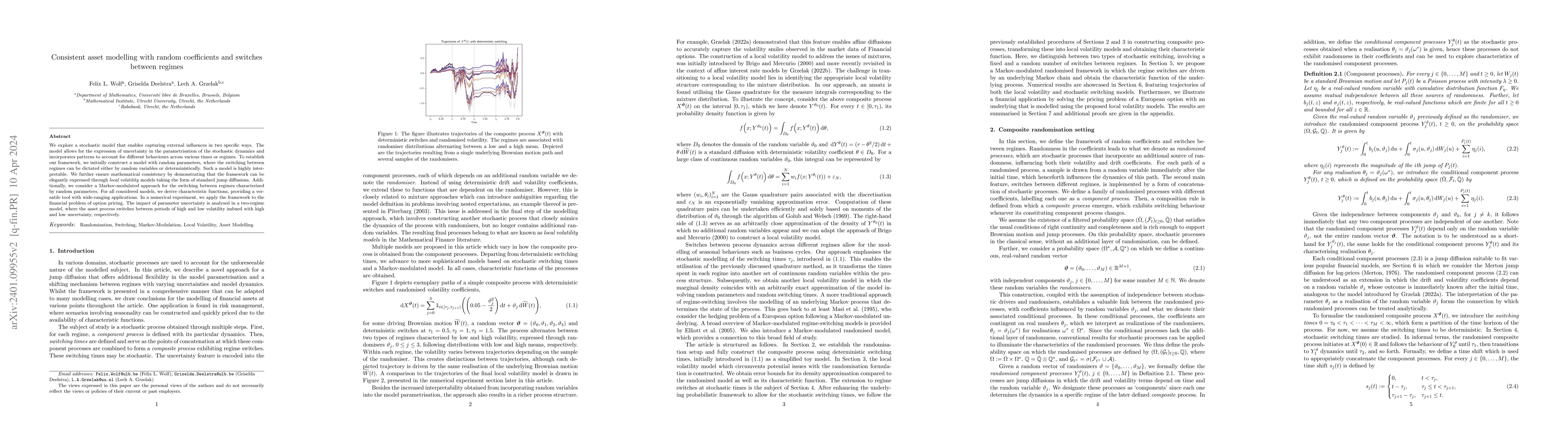

We explore a stochastic model that enables capturing external influences in two specific ways. The model allows for the expression of uncertainty in the parametrisation of the stochastic dynamics an...

Exposure simulations are fundamental to many xVA calculations and are a nested expectation problem where repeated portfolio valuations create a significant computational expense. Sensitivity calcula...

The collateral choice option allows a collateral-posting party the opportunity to change the type of security in which the collateral is deposited. Due to non-zero collateral basis spreads, this opt...

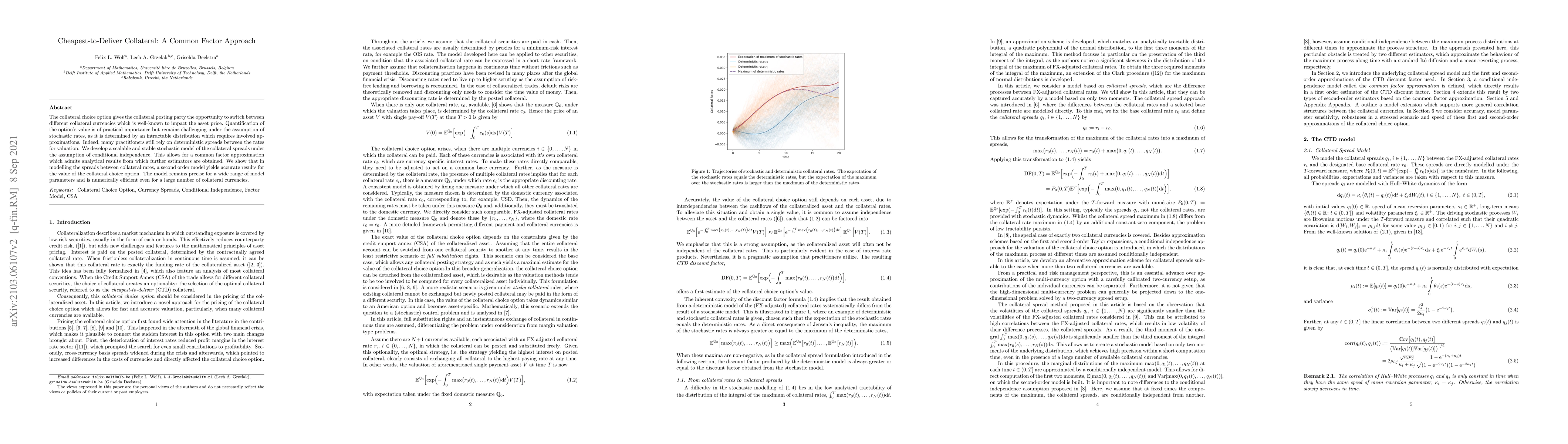

The collateral choice option gives the collateral posting party the opportunity to switch between different collateral currencies which is well-known to impact the asset price. Quantification of the...