Consistent asset modelling with random coefficients and switches between regimes

Publication

Metrics

AI Quick Summary

This research develops a stochastic model with random coefficients and regime switches to capture external influences and parameter uncertainty in asset dynamics. The model allows for regime changes dictated by random or deterministic variables and is mathematically consistent through local volatility models.

Paper Preview

Abstract

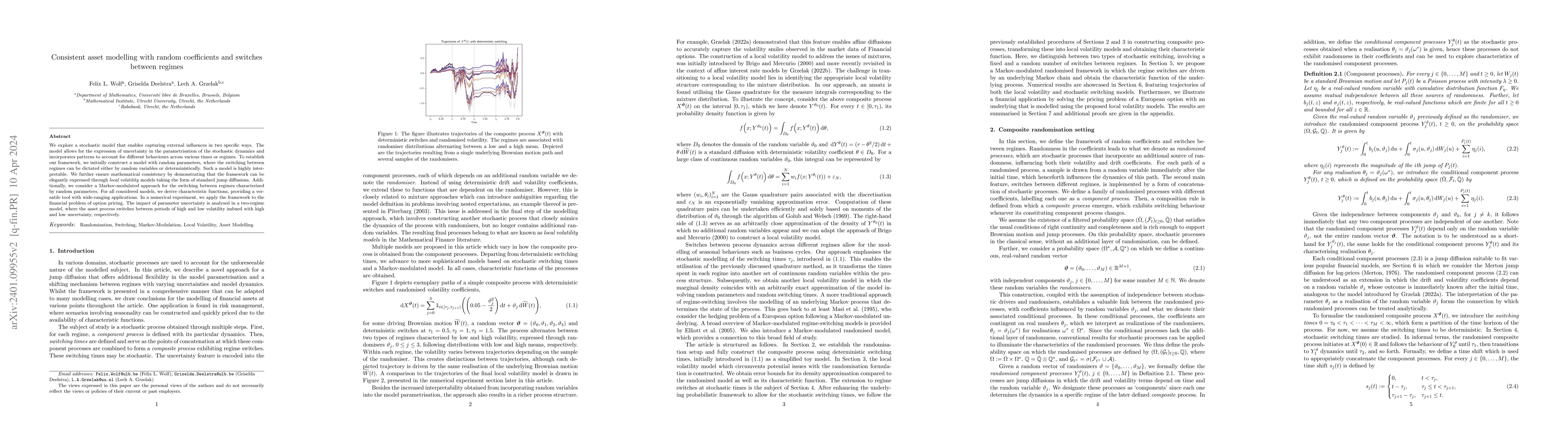

We explore a stochastic model that enables capturing external influences in two specific ways. The model allows for the expression of uncertainty in the parametrisation of the stochastic dynamics and incorporates patterns to account for different behaviours across various times or regimes. To establish our framework, we initially construct a model with random parameters, where the switching between regimes can be dictated either by random variables or deterministically. Such a model is highly interpretable. We further ensure mathematical consistency by demonstrating that the framework can be elegantly expressed through local volatility models taking the form of standard jump diffusions. Additionally, we consider a Markov-modulated approach for the switching between regimes characterised by random parameters. For all considered models, we derive characteristic functions, providing a versatile tool with wide-ranging applications. In a numerical experiment, we apply the framework to the financial problem of option pricing. The impact of parameter uncertainty is analysed in a two-regime model, where the asset process switches between periods of high and low volatility imbued with high and low uncertainty, respectively.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0