Academic Profile

Statistics

Similar Authors

Papers on arXiv

The pricing of derivatives tied to baskets of assets demands a sophisticated framework that aligns with the available market information to capture the intricate non-linear dependency structure amon...

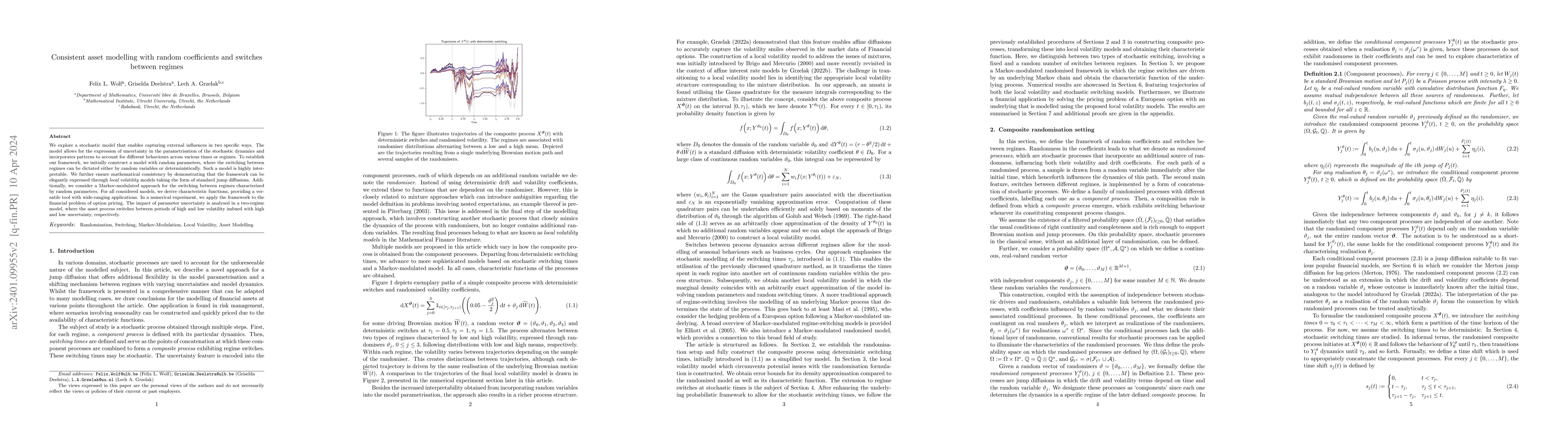

We explore a stochastic model that enables capturing external influences in two specific ways. The model allows for the expression of uncertainty in the parametrisation of the stochastic dynamics an...

Monte Carlo simulation is widely used to numerically solve stochastic differential equations. Although the method is flexible and easy to implement, it may be slow to converge. Moreover, an inaccura...

Exposure simulations are fundamental to many xVA calculations and are a nested expectation problem where repeated portfolio valuations create a significant computational expense. Sensitivity calcula...

We focus on extending existing short-rate models, enabling control of the generated implied volatility while preserving analyticity. We achieve this goal by applying the Randomized Affine Diffusion ...

We propose a new, data-driven approach for efficient pricing of - fixed- and float-strike - discrete arithmetic Asian and Lookback options when the underlying process is driven by the Heston model d...

The class of Affine (Jump) Diffusion (AD) has, due to its closed form characteristic function (ChF), gained tremendous popularity among practitioners and researchers. However, there is clear evidenc...

The collateral choice option allows a collateral-posting party the opportunity to change the type of security in which the collateral is deposited. Due to non-zero collateral basis spreads, this opt...

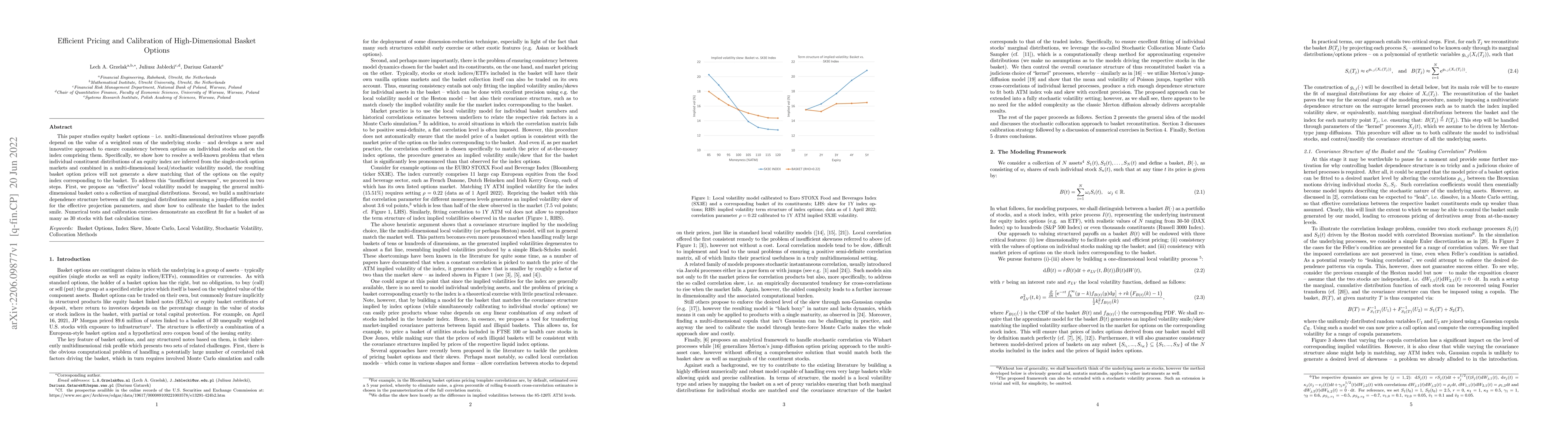

This paper studies equity basket options -- i.e., multi-dimensional derivatives whose payoffs depend on the value of a weighted sum of the underlying stocks -- and develops a new and innovative appr...

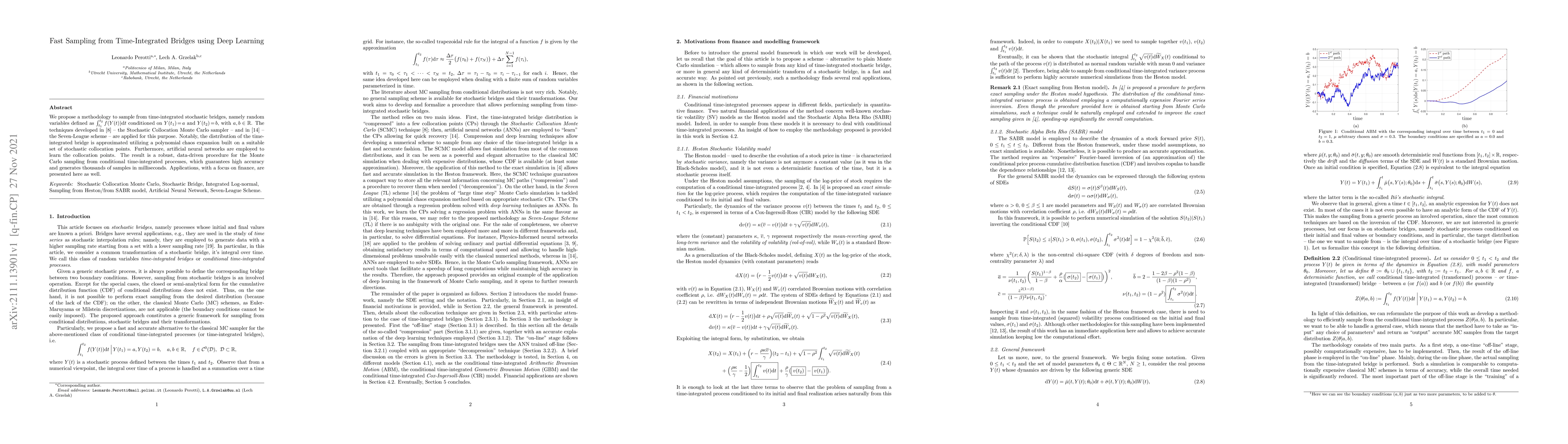

We propose a methodology to sample from time-integrated stochastic bridges, namely random variables defined as $\int_{t_1}^{t_2} f(Y(t))dt$ conditioned on $Y(t_1)\!=\!a$ and $Y(t_2)\!=\!b$, with $a,...

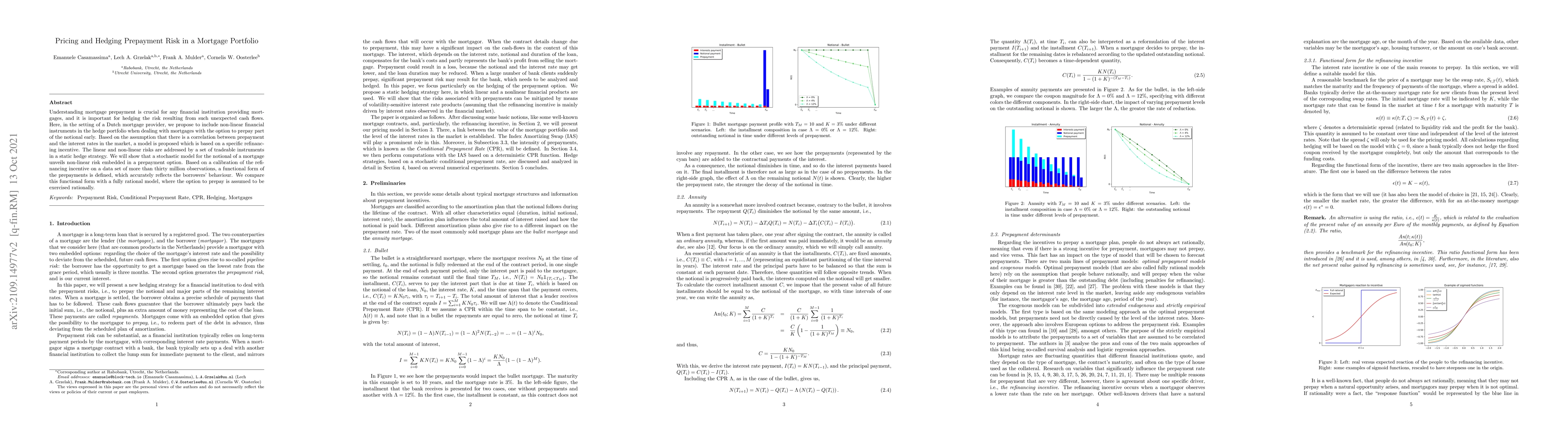

Understanding mortgage prepayment is crucial for any financial institution providing mortgages, and it is important for hedging the risk resulting from such unexpected cash flows. Here, in the setti...

Every "x"-adjustment in the so-called xVA financial risk management framework relies on the computation of exposures. Considering thousands of Monte Carlo paths and tens of simulation steps, a finan...

Generative adversarial networks (GANs) have shown promising results when applied on partial differential equations and financial time series generation. We investigate if GANs can also be used to ap...

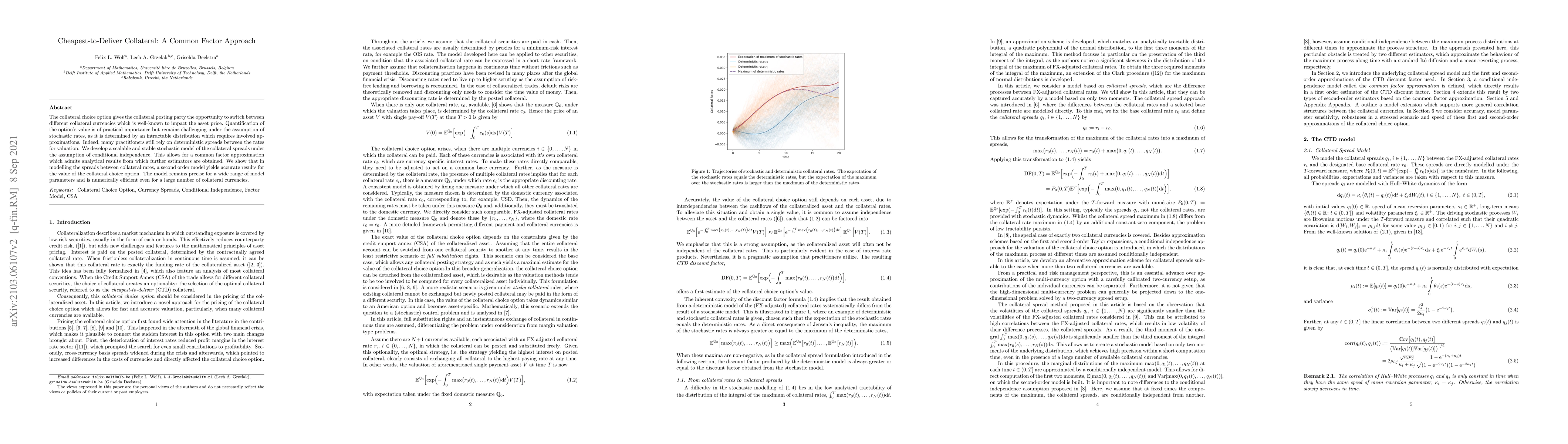

The collateral choice option gives the collateral posting party the opportunity to switch between different collateral currencies which is well-known to impact the asset price. Quantification of the...

A data-driven approach called CaNN (Calibration Neural Network) is proposed to calibrate financial asset price models using an Artificial Neural Network (ANN). Determining optimal values of the mode...

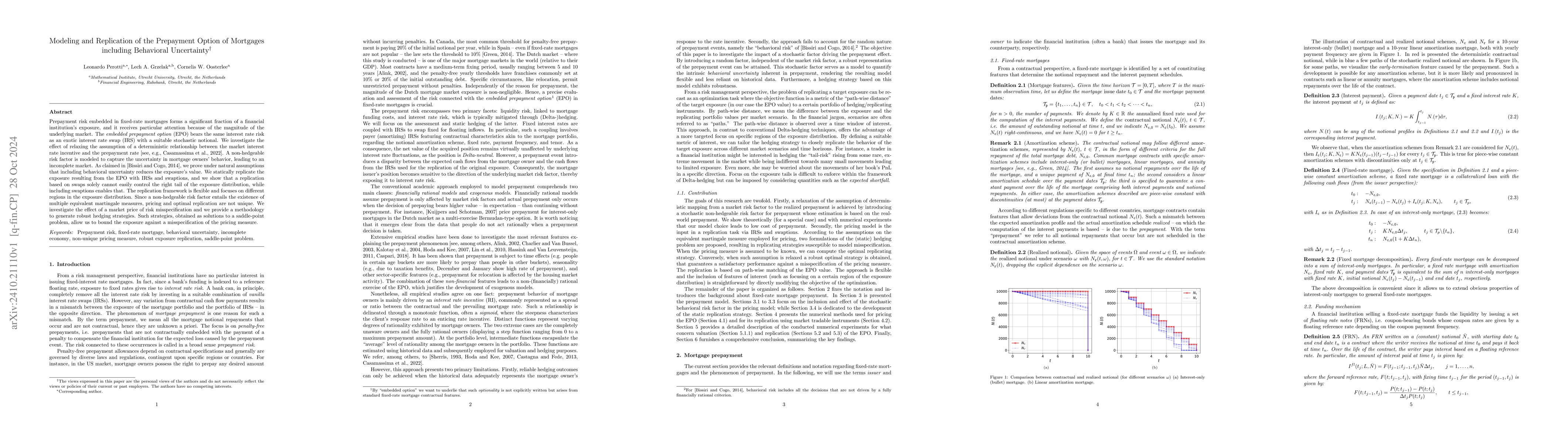

Prepayment risk embedded in fixed-rate mortgages forms a significant fraction of a financial institution's exposure, and it receives particular attention because of the magnitude of the underlying mar...

It is a market practice to express market-implied volatilities in some parametric form. The most popular parametrizations are based on or inspired by an underlying stochastic model, like the Heston mo...

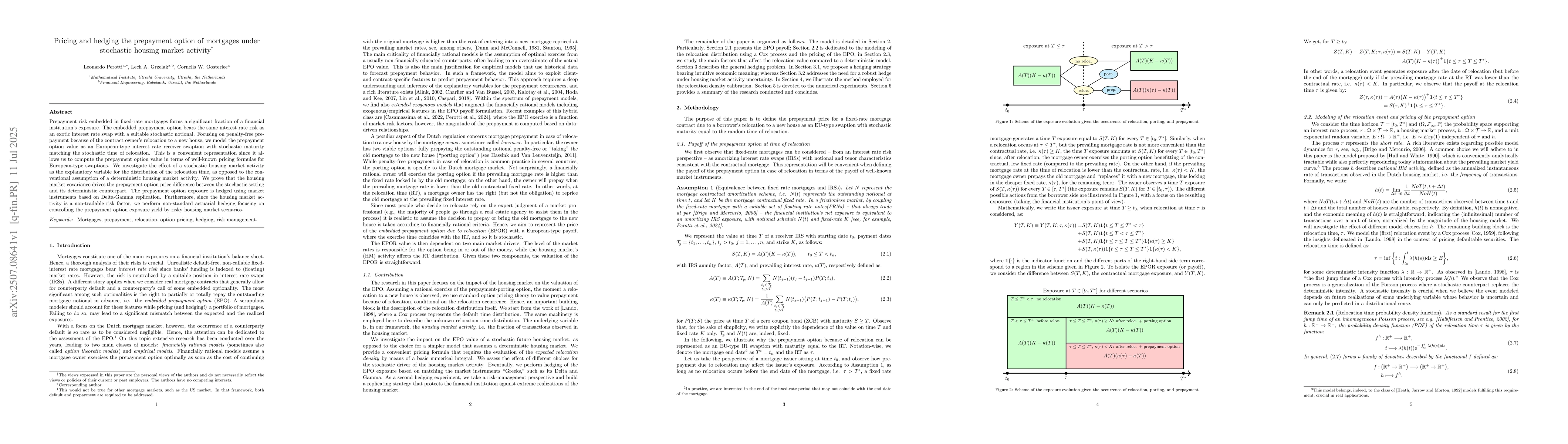

Prepayment risk embedded in fixed-rate mortgages forms a significant fraction of a financial institution's exposure. The embedded prepayment option bears the same interest rate risk as an exotic inter...

The lifted Heston model is a stochastic volatility model emerging as a Markovian lift of the rough Heston model and the class of rough volatility processes. The model encodes the path dependency of vo...