Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present new numerical schemes for pricing perpetual Bermudan and American options as well as $\alpha$-quantile options. This includes a new direct calculation of the optimal exercise barrier for ...

We present numerical methods based on the fast Fourier transform (FFT) to solve convolution integral equations on a semi-infinite interval (Wiener-Hopf equation) or on a finite interval (Fredholm eq...

We show how spectral filters can improve the convergence of numerical schemes which use discrete Hilbert transforms based on a sinc function expansion, and thus ultimately on the fast Fourier transf...

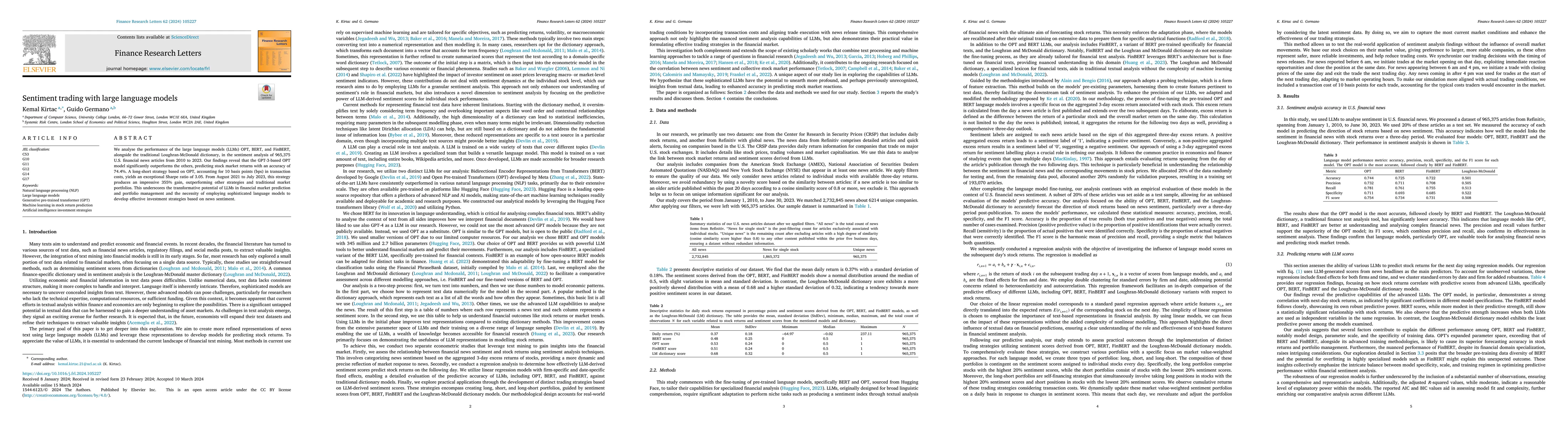

We investigate the efficacy of large language models (LLMs) in sentiment analysis of U.S. financial news and their potential in predicting stock market returns. We analyze a dataset comprising 965,375...

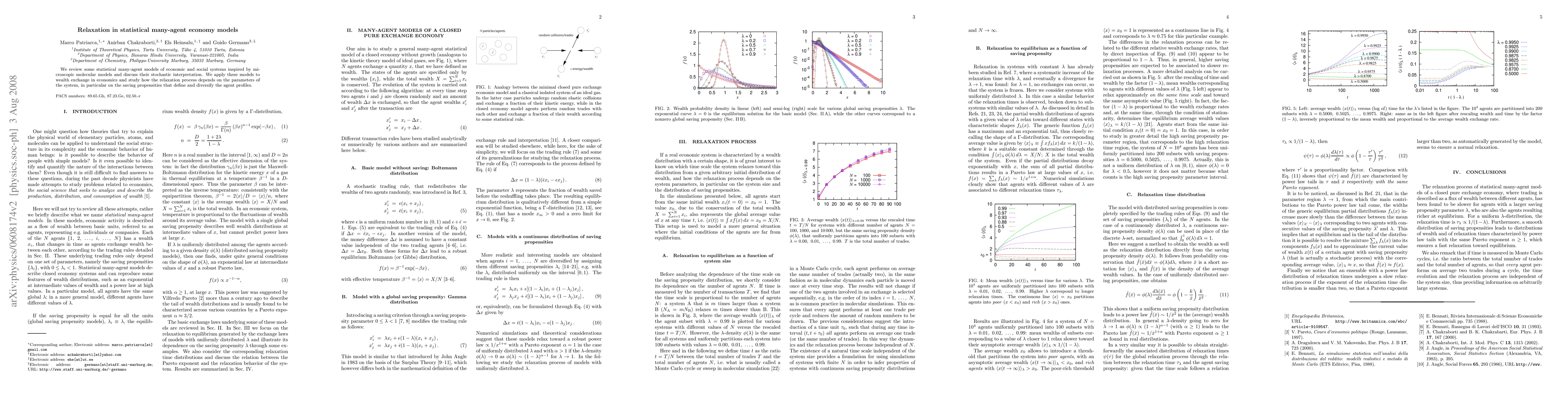

We review some statistical many-agent models of economic and social systems inspired by microscopic molecular models and discuss their stochastic interpretation. We apply these models to wealth exchan...

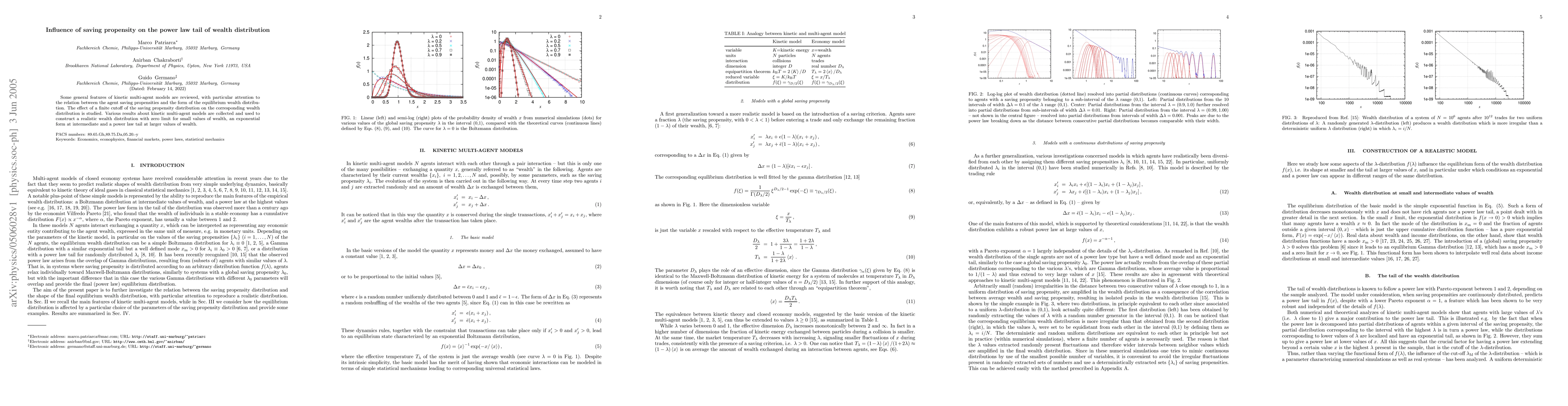

Some general features of kinetic multi-agent models are reviewed, with particular attention to the relation between the agent saving propensities and the form of the equilibrium wealth distribution. T...

Various multi-agent models of wealth distributions defined by microscopic laws regulating the trades, with or without a saving criterion, are reviewed. We discuss and clarify the equilibrium propertie...

Financial sentiment has become a crucial yet complex concept in finance, increasingly used in market forecasting and investment strategies. Despite its growing importance, there remains a need to defi...

We review some statistical many-agent models of economic and social systems inspired by microscopic molecular models and discuss their stochastic interpretation. We apply these models to wealth exchan...

Some general features of kinetic multi-agent models are reviewed, with particular attention to the relation between the agent saving propensities and the form of the equilibrium wealth distribution. T...

Various multi-agent models of wealth distributions defined by microscopic laws regulating the trades, with or without a saving criterion, are reviewed. We discuss and clarify the equilibrium propertie...