Academic Profile

Statistics

Similar Authors

Papers on arXiv

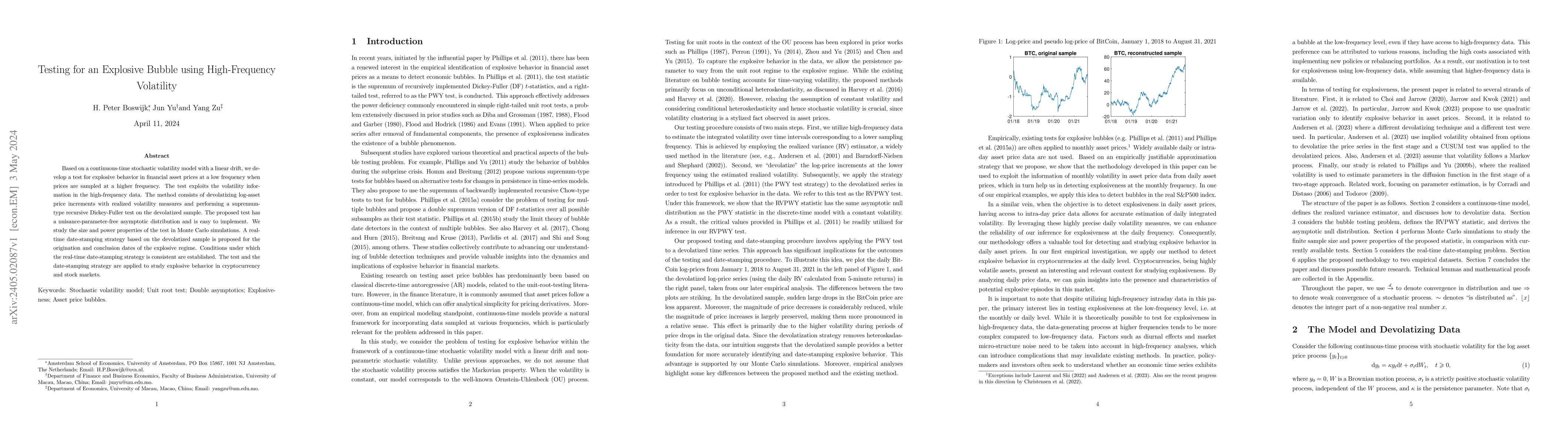

Based on a continuous-time stochastic volatility model with a linear drift, we develop a test for explosive behavior in financial asset prices at a low frequency when prices are sampled at a higher ...

We develop a novel filtering and estimation procedure for parametric option pricing models driven by general affine jump-diffusions. Our procedure is based on the comparison between an option-implie...

Standard methods, such as sequential procedures based on Johansen's (pseudo-)likelihood ratio (PLR) test, for determining the co-integration rank of a vector autoregressive (VAR) system of variables...

In this paper we investigate how the bootstrap can be applied to time series regressions when the volatility of the innovations is random and non-stationary. The volatility of many economic and fina...