Academic Profile

Statistics

Similar Authors

Papers on arXiv

A continuous-time financial portfolio selection model with expected utility maximization typically boils down to solving a (static) convex stochastic optimization problem in terms of the terminal we...

We propose an innovative data-driven option pricing methodology that relies exclusively on the dataset of historical underlying asset prices. While the dataset is rooted in the objective world, opti...

As the COVID19 spreads across the world, prevention measures are becoming the essential weapons to combat the pandemic in the period of crisis. The lockdown measure is the most controversial one as ...

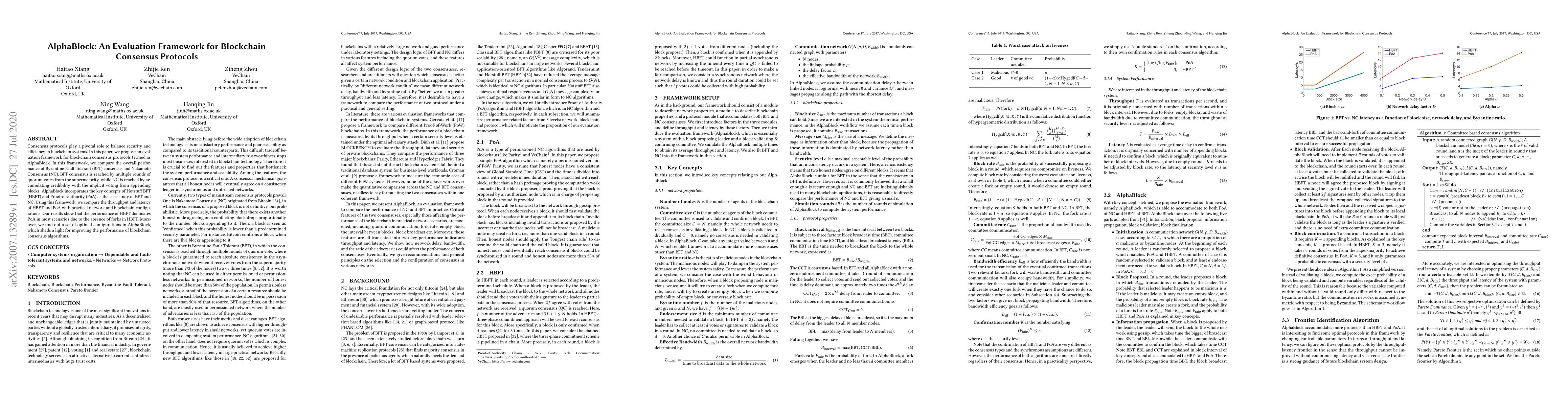

Consensus protocols play a pivotal role to balance security and efficiency in blockchain systems. In this paper, we propose an evaluation framework for blockchain consensus protocols termed as Alpha...

We study portfolio selection in a complete continuous-time market where the preference is dictated by the rank-dependent utility. As such a model is inherently time inconsistent due to the underlyin...

This paper studies the continuous time mean-variance portfolio selection problem with one kind of non-linear wealth dynamics. To deal the expectation constraint, an auxiliary stochastic control prob...

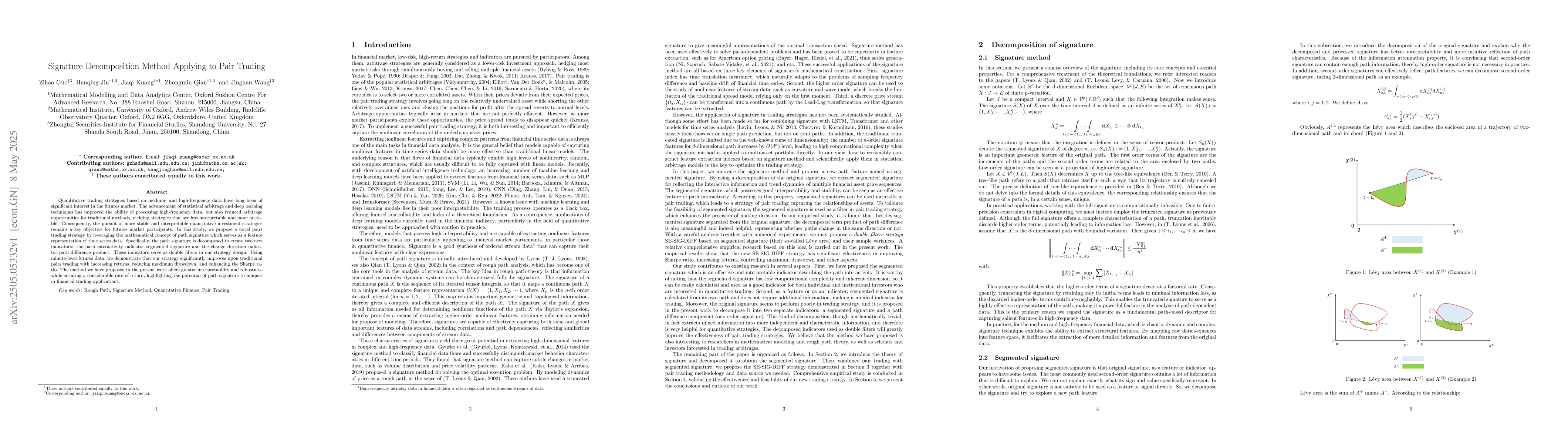

Quantitative trading strategies based on medium- and high-frequency data have long been of significant interest in the futures market. The advancement of statistical arbitrage and deep learning techni...

We study reinforcement learning for controlled diffusion processes with unbounded continuous state spaces, bounded continuous actions, and polynomially growing rewards: settings that arise naturally i...

In this paper, we propose a new framework for solving a general dynamic optimal stopping problem without time consistency. A sophisticated solution is proposed and is well-defined for any time setting...