Academic Profile

Statistics

Similar Authors

Papers on arXiv

Inventory matching is a standard mechanism/auction for trading financial stocks by which buyers and sellers can be paired. In the financial world, banks often undertake the task of finding such matc...

We present a method for finding optimal hedging policies for arbitrary initial portfolios and market states. We develop a novel actor-critic algorithm for solving general risk-averse stochastic cont...

We present an actor-critic-type reinforcement learning algorithm for solving the problem of hedging a portfolio of financial instruments such as securities and over-the-counter derivatives using pur...

We construct realistic spot and equity option market simulators for a single underlying on the basis of normalizing flows. We address the high-dimensionality of market observed call prices through a...

We present a machine learning approach for finding minimal equivalent martingale measures for markets simulators of tradable instruments, e.g. for a spot price and options written on the same underl...

We present a numerically efficient approach for learning a risk-neutral measure for paths of simulated spot and option prices up to a finite horizon under convex transaction costs and convex trading...

We construct realistic equity option market simulators based on generative adversarial networks (GANs). We consider recurrent and temporal convolutional architectures, and assess the impact of state...

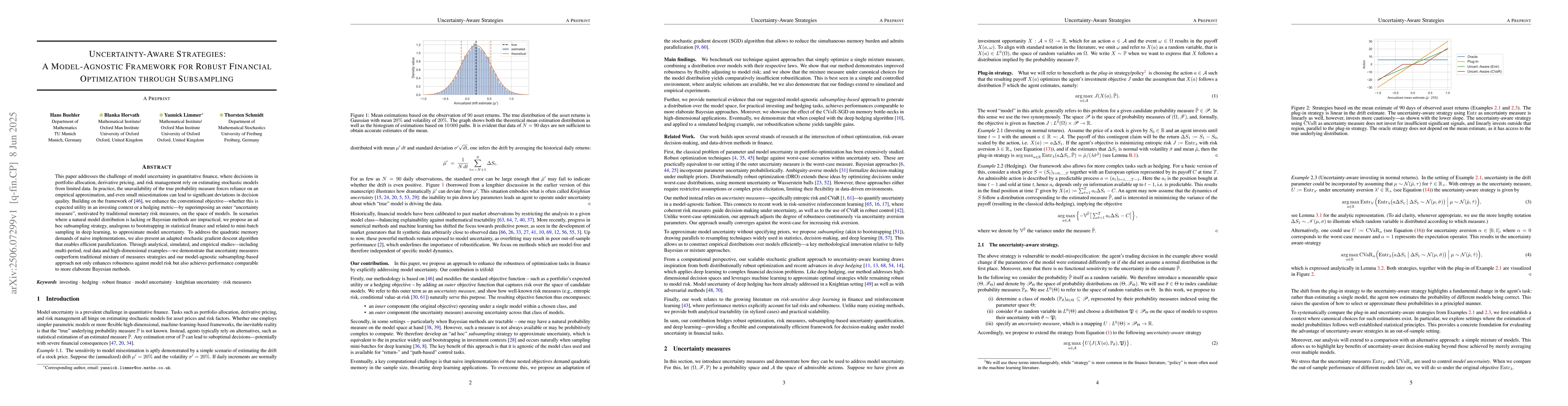

This paper addresses the challenge of model uncertainty in quantitative finance, where decisions in portfolio allocation, derivative pricing, and risk management rely on estimating stochastic models f...

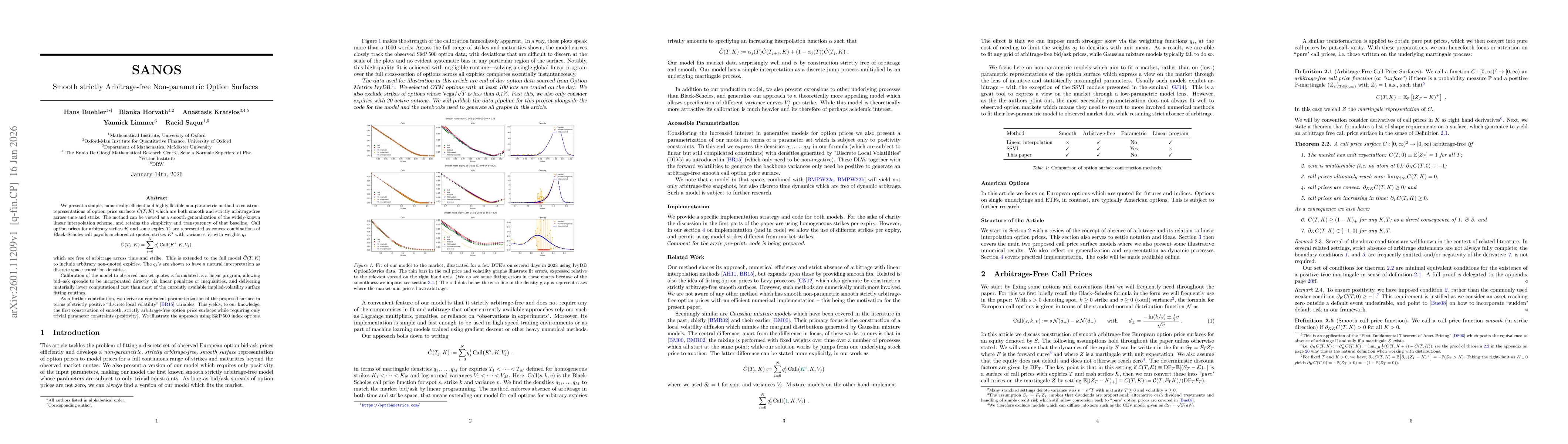

We present a simple, numerically efficient but highly flexible non-parametric method to construct representations of option price surfaces which are both smooth and strictly arbitrage-free across time...

Modern option-learning systems operate in two coordinates: price space, where markets quote and no-arbitrage constraints are most naturally enforced, and implied volatility (IV) space, where volatilit...