Academic Profile

Statistics

Similar Authors

Papers on arXiv

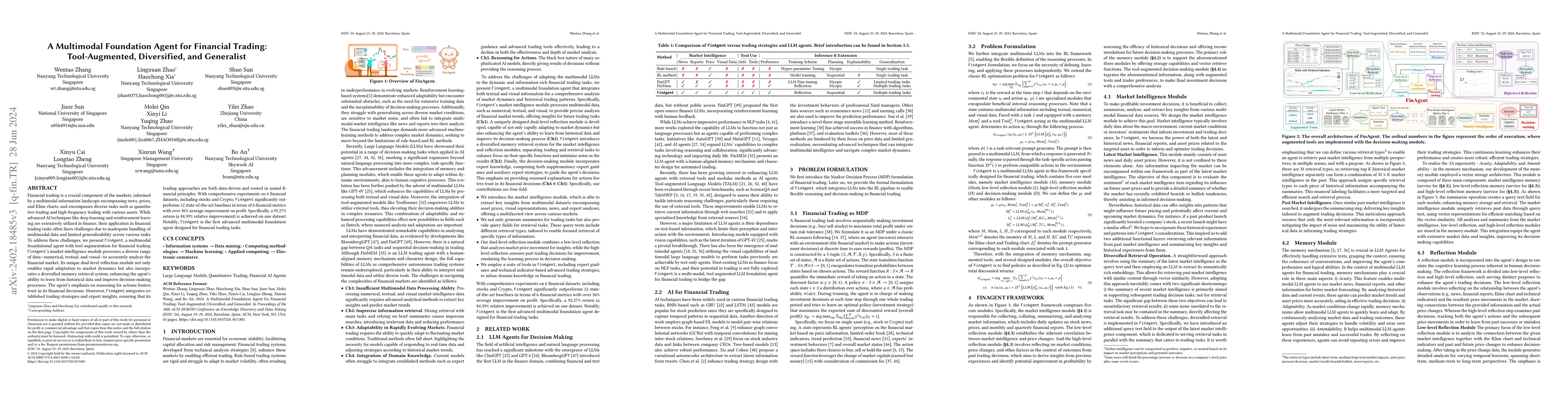

Financial trading is a crucial component of the markets, informed by a multimodal information landscape encompassing news, prices, and Kline charts, and encompasses diverse tasks such as quantitative ...

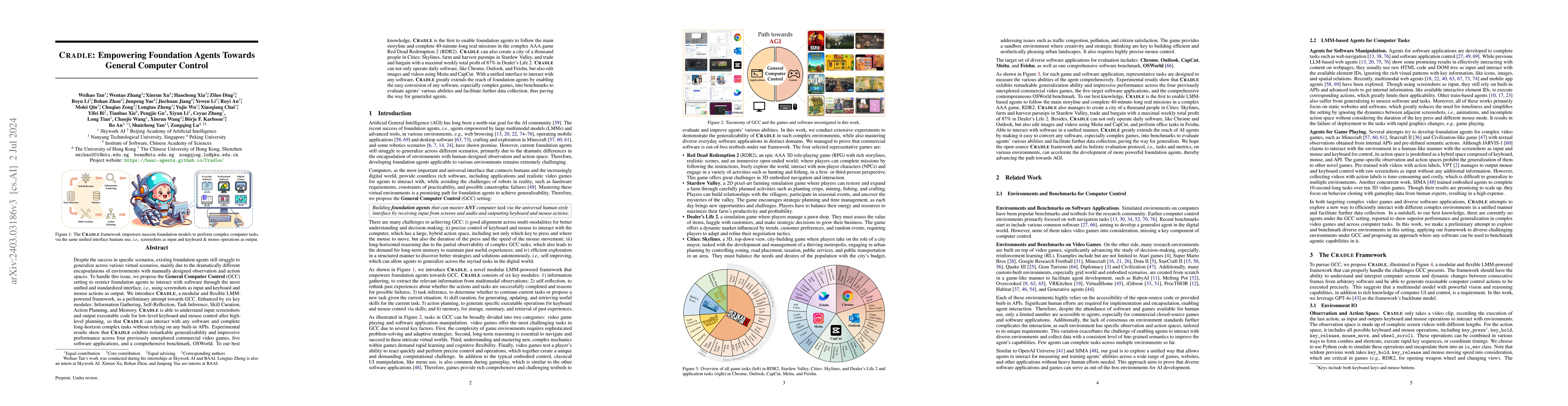

Despite the success in specific scenarios, existing foundation agents still struggle to generalize across various virtual scenarios, mainly due to the dramatically different encapsulations of enviro...

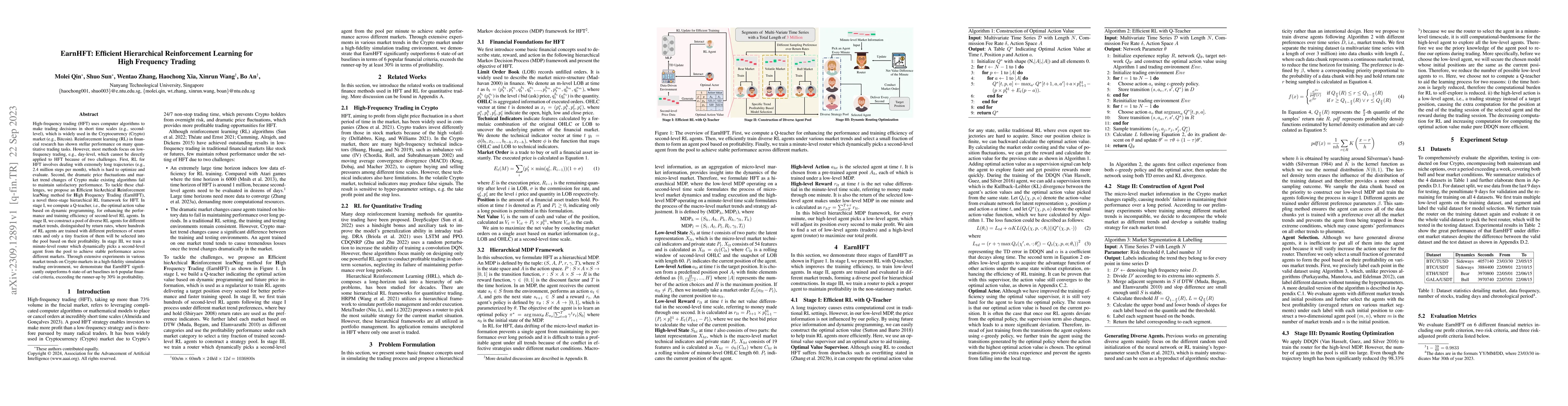

High-frequency trading (HFT) uses computer algorithms to make trading decisions in short time scales (e.g., second-level), which is widely used in the Cryptocurrency (Crypto) market (e.g., Bitcoin)....

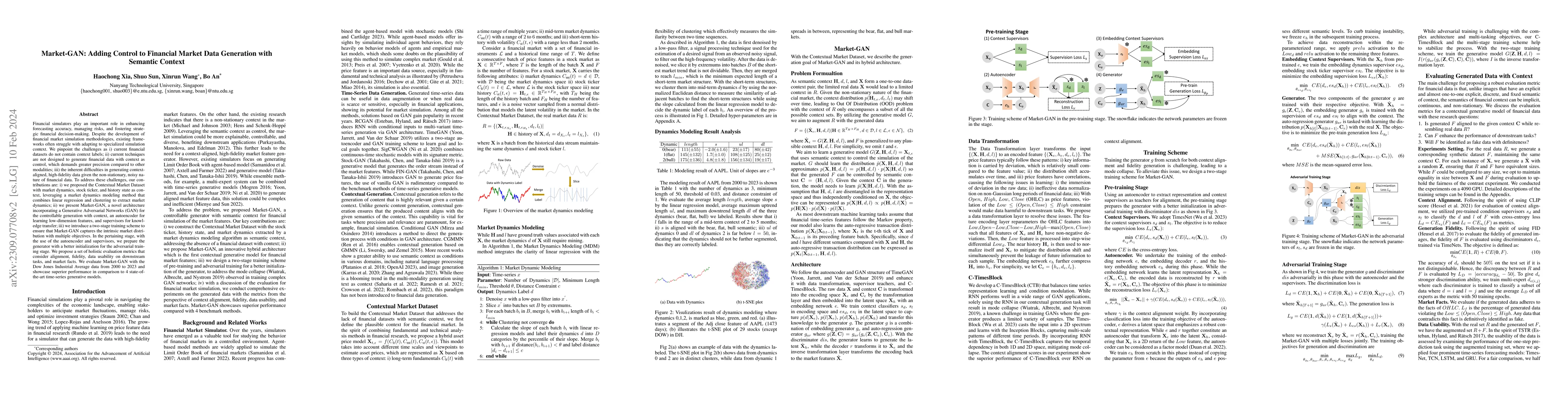

Financial simulators play an important role in enhancing forecasting accuracy, managing risks, and fostering strategic financial decision-making. Despite the development of financial market simulati...

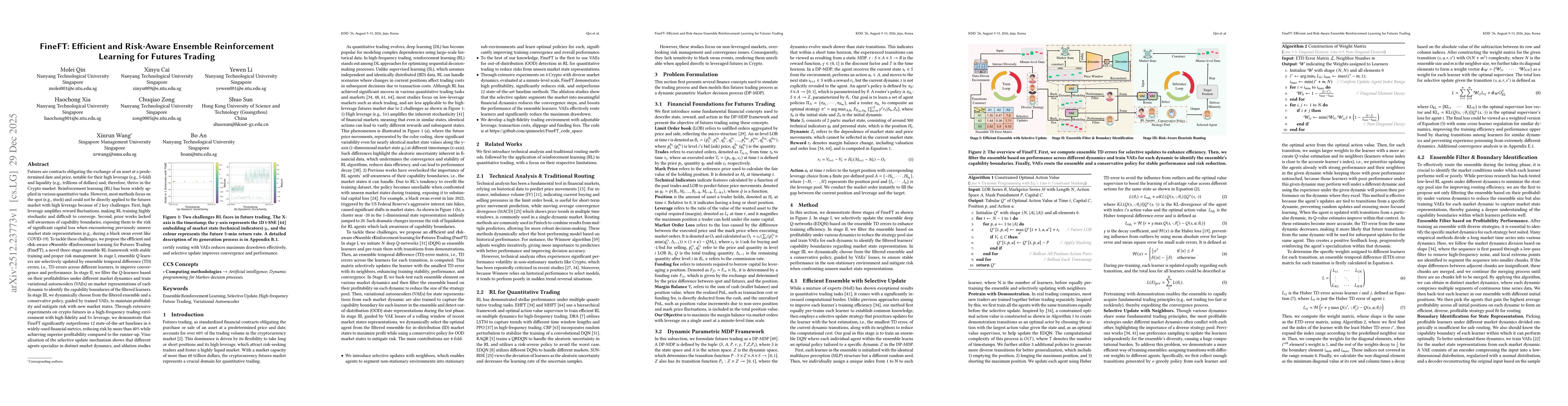

Futures are contracts obligating the exchange of an asset at a predetermined date and price, notable for their high leverage and liquidity and, therefore, thrive in the Crypto market. RL has been wide...

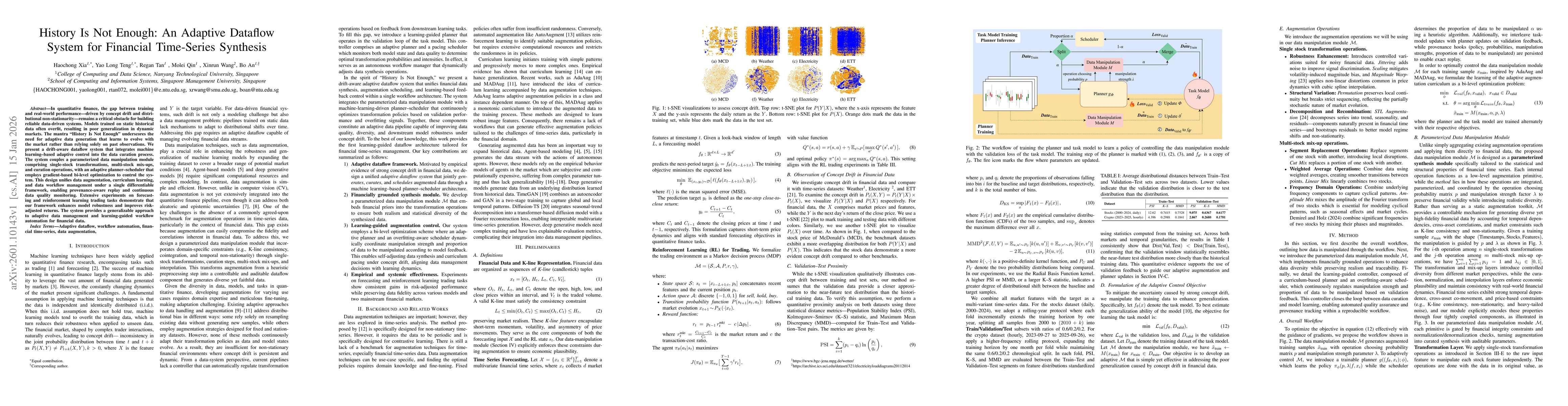

In quantitative finance, the gap between training and real-world performance-driven by concept drift and distributional non-stationarity-remains a critical obstacle for building reliable data-driven s...

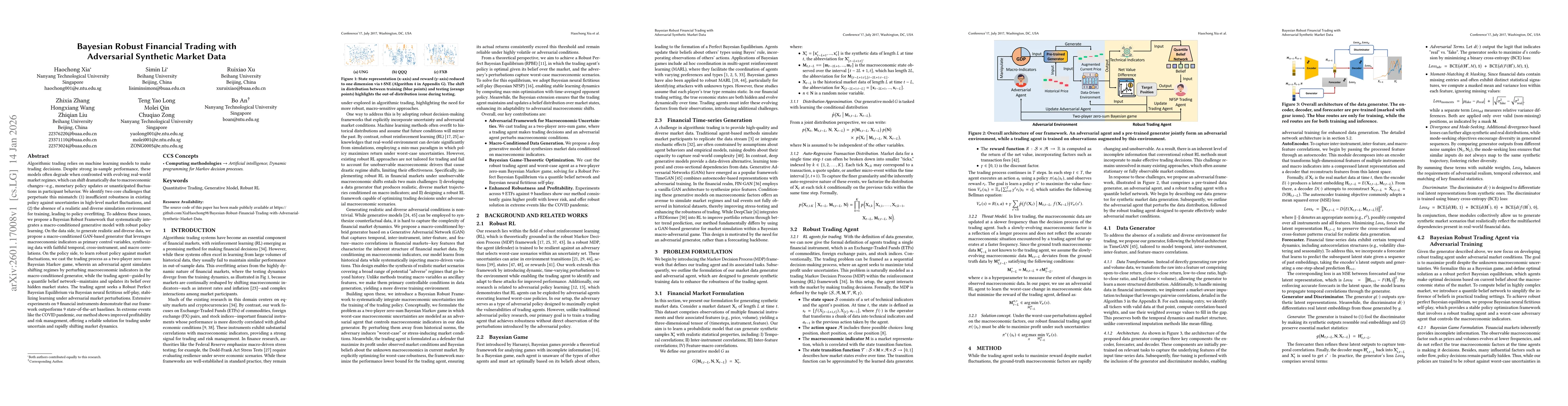

Algorithmic trading relies on machine learning models to make trading decisions. Despite strong in-sample performance, these models often degrade when confronted with evolving real-world market regime...