Academic Profile

Statistics

Similar Authors

Papers on arXiv

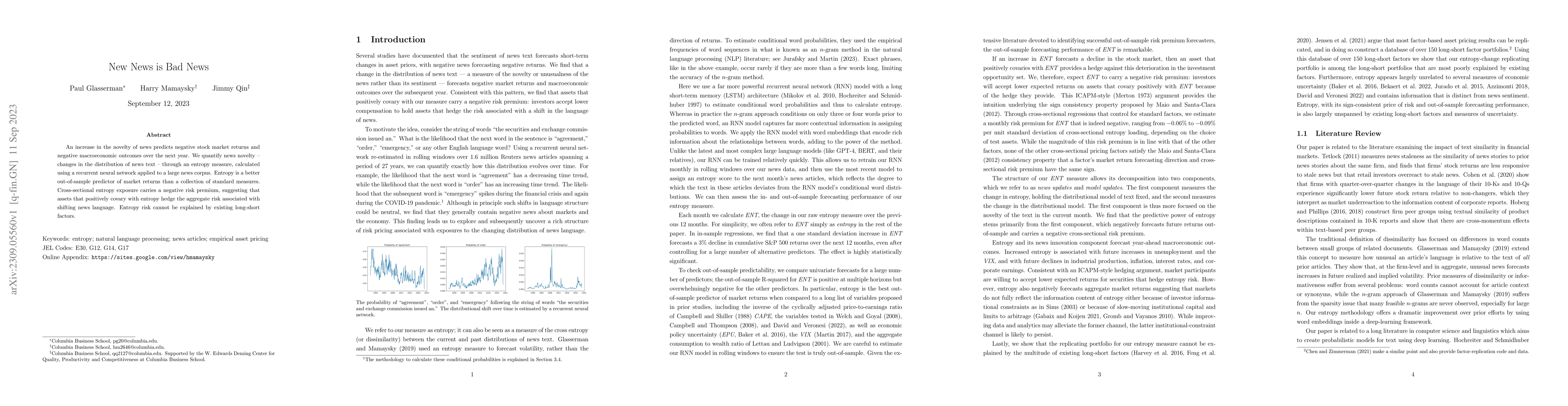

An increase in the novelty of news predicts negative stock market returns and negative macroeconomic outcomes over the next year. We quantify news novelty - changes in the distribution of news text ...

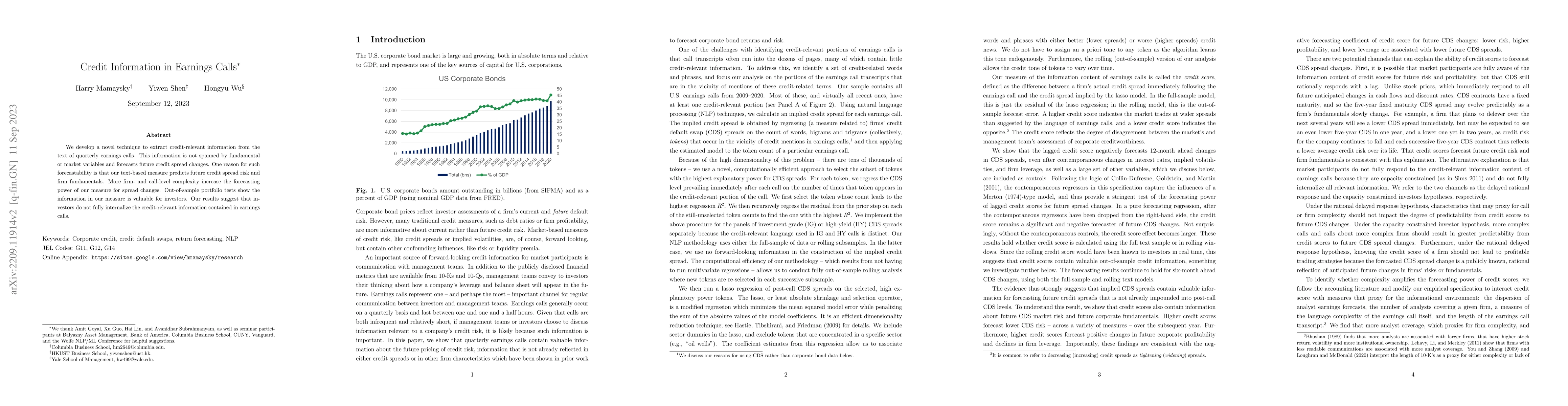

We develop a novel technique to extract credit-relevant information from the text of quarterly earnings calls. This information is not spanned by fundamental or market variables and forecasts future...

We analyze methods for selecting topics in news articles to explain stock returns. We find, through empirical and theoretical results, that supervised Latent Dirichlet Allocation (sLDA) implemented ...

Over the past 30 years, nearly all the gains in the U.S. stock market have been earned overnight, while average intraday returns have been negative or flat. We find that a large part of this effect ca...