Academic Profile

Statistics

Papers on arXiv

Bayesian Optimization is a popular approach for optimizing expensive black-box functions. Its key idea is to use a surrogate model to approximate the objective and, importantly, quantify the associate...

Bayesian bandit algorithms with approximate Bayesian inference have been widely used in real-world applications. Nevertheless, their theoretical justification is less investigated in the literature, e...

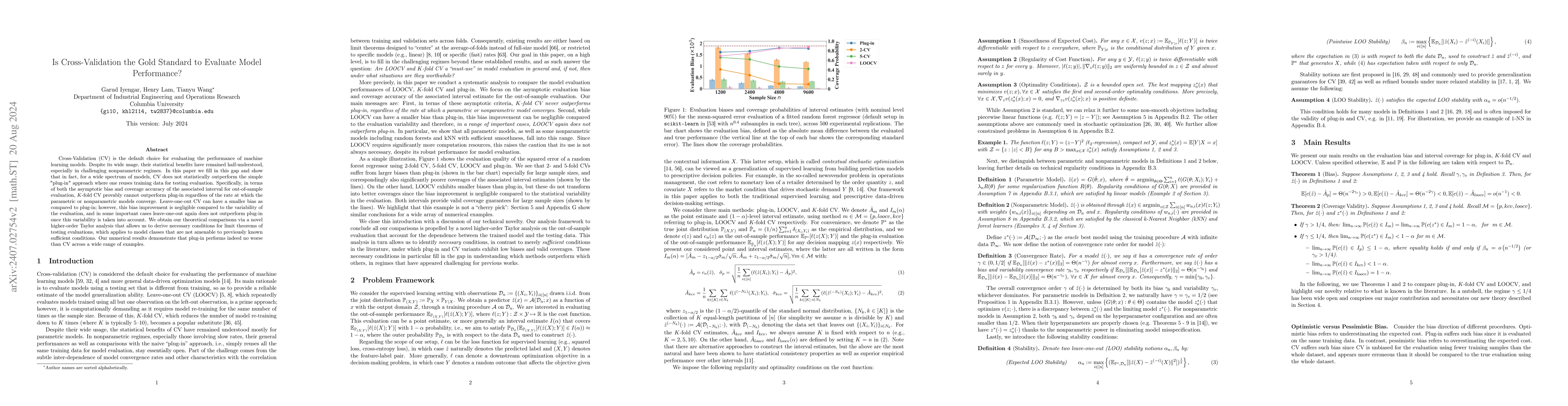

Cross-Validation (CV) is the default choice for evaluating the performance of machine learning models. Despite its wide usage, their statistical benefits have remained half-understood, especially in...

Shape-constrained optimization arises in a wide range of problems including distributionally robust optimization (DRO) that has surging popularity in recent years. In the DRO literature, these probl...

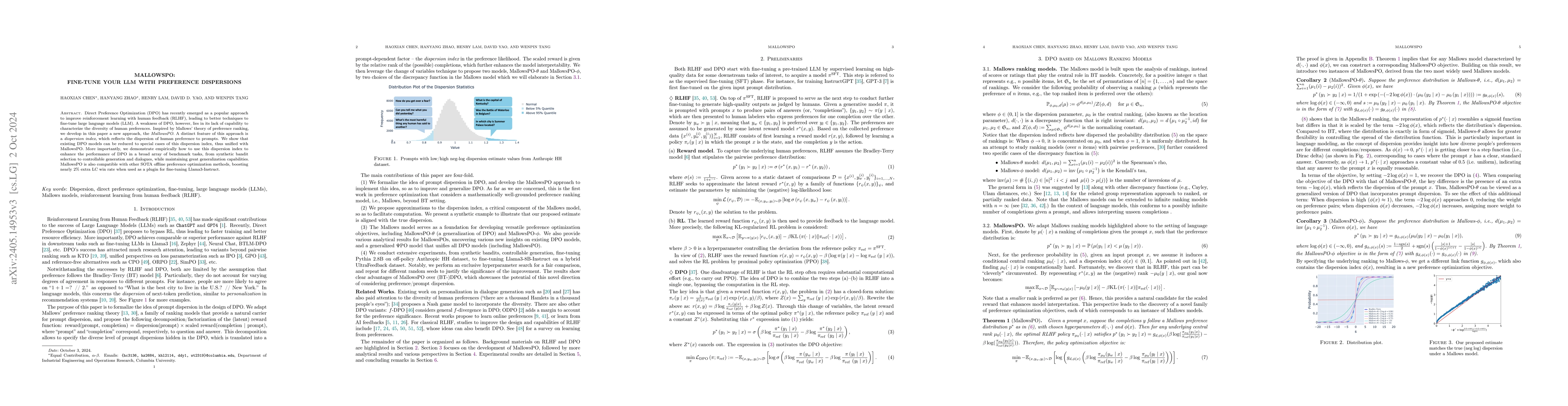

Direct Preference Optimization (DPO) has recently emerged as a popular approach to improve reinforcement learning with human feedback (RLHF), leading to better techniques to fine-tune large language...

Bagging is a popular ensemble technique to improve the accuracy of machine learning models. It hinges on the well-established rationale that, by repeatedly retraining on resampled data, the aggregat...

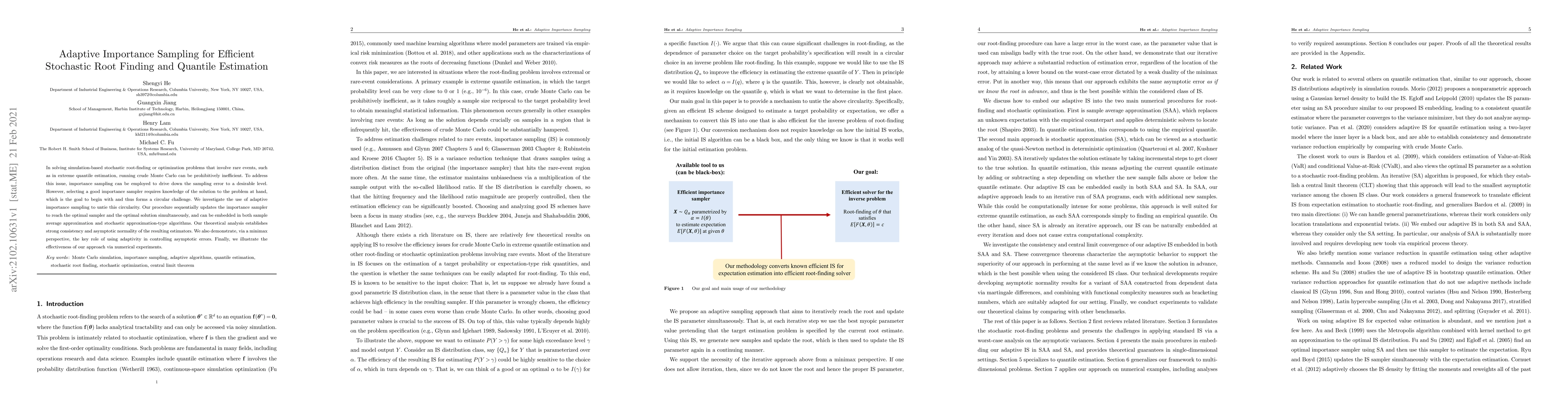

In stochastic simulation, input uncertainty refers to the propagation of the statistical noise in calibrating input models to impact output accuracy, in addition to the Monte Carlo simulation noise....

Offline reinforcement learning (RL) offers a promising direction for learning policies from pre-collected datasets without requiring further interactions with the environment. However, existing meth...

We consider the estimation of small probabilities or other risk quantities associated with rare but catastrophic events. In the model-based literature, much of the focus has been devoted to efficien...

Stochastic gradient descent (SGD) or stochastic approximation has been widely used in model training and stochastic optimization. While there is a huge literature on analyzing its convergence, infer...

In data-driven optimization, sample average approximation (SAA) is known to suffer from the so-called optimizer's curse that causes an over-optimistic evaluation of the solution performance. We argu...

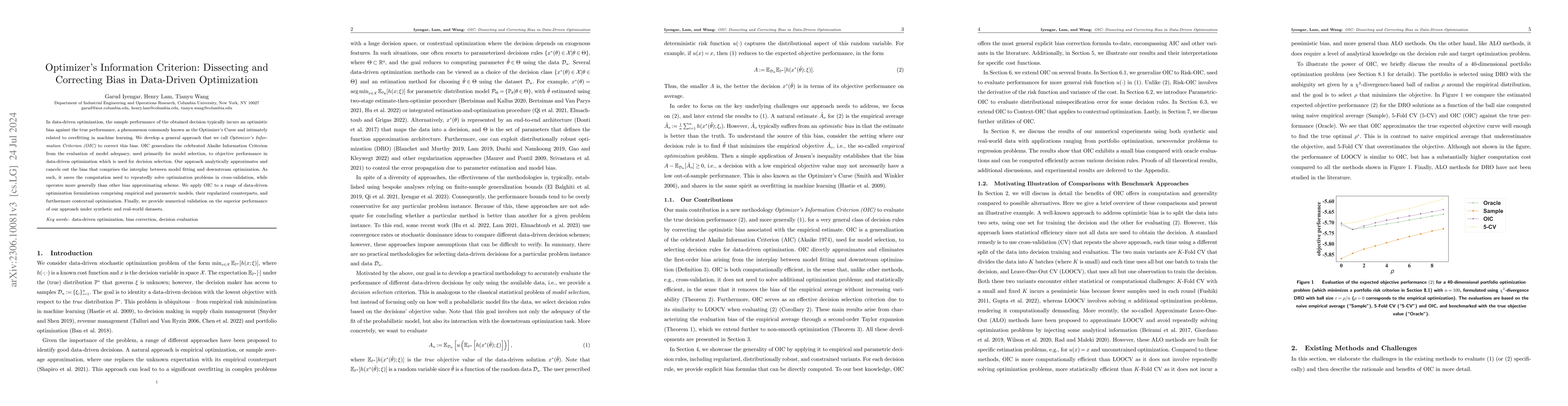

In data-driven optimization, the sample performance of the obtained decision typically incurs an optimistic bias against the true performance, a phenomenon commonly known as the Optimizer's Curse an...

Uncertainty quantification (UQ) is important for reliability assessment and enhancement of machine learning models. In deep learning, uncertainties arise not only from data, but also from the traini...

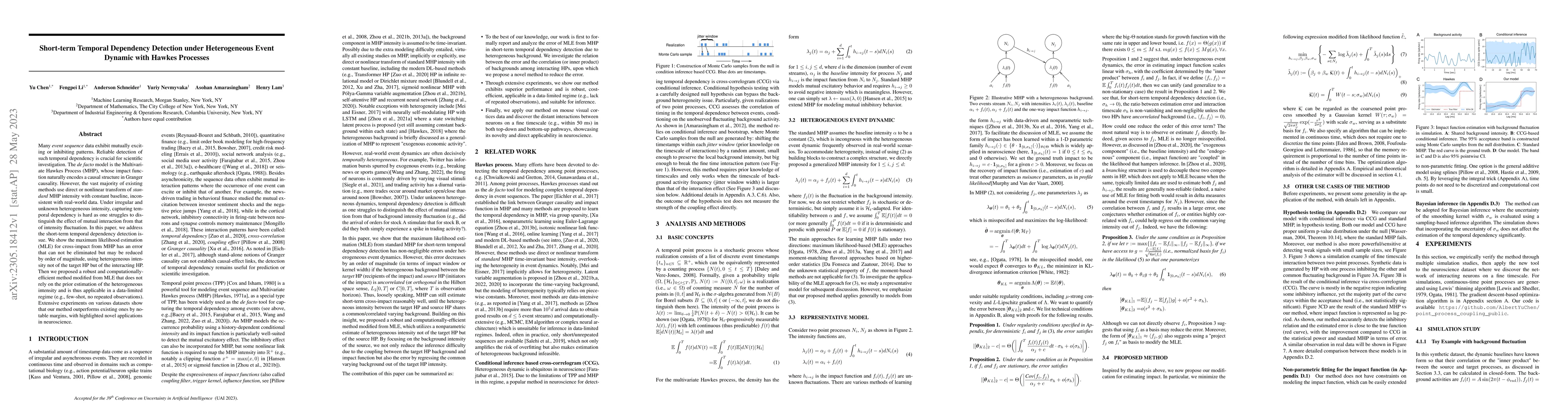

Many event sequence data exhibit mutually exciting or inhibiting patterns. Reliable detection of such temporal dependency is crucial for scientific investigation. The de facto model is the Multivari...

We consider the estimation of rare-event probabilities using sample proportions output by naive Monte Carlo or collected data. Unlike using variance reduction techniques, this naive estimator does n...

In data-driven stochastic optimization, model parameters of the underlying distribution need to be estimated from data in addition to the optimization task. Recent literature considers integrating t...

Conventional methods for extreme event estimation rely on well-chosen parametric models asymptotically justified from extreme value theory (EVT). These methods, while powerful and theoretically grou...

Empirical risk minimization (ERM) and distributionally robust optimization (DRO) are popular approaches for solving stochastic optimization problems that appear in operations management and machine ...

We study the problem of multi-task non-smooth optimization that arises ubiquitously in statistical learning, decision-making and risk management. We develop a data fusion approach that adaptively le...

One key challenge for multi-task Reinforcement learning (RL) in practice is the absence of task indicators. Robust RL has been applied to deal with task ambiguity, but may result in over-conservativ...

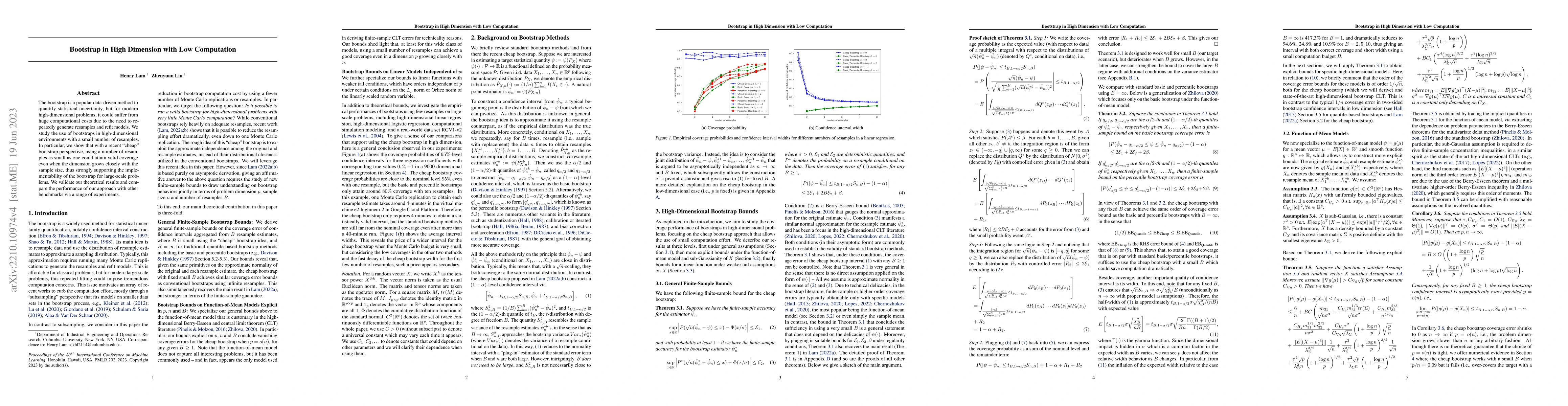

The bootstrap is a popular data-driven method to quantify statistical uncertainty, but for modern high-dimensional problems, it could suffer from huge computational costs due to the need to repeated...

Aleatoric uncertainty quantification seeks for distributional knowledge of random responses, which is important for reliability analysis and robustness improvement in machine learning applications. ...

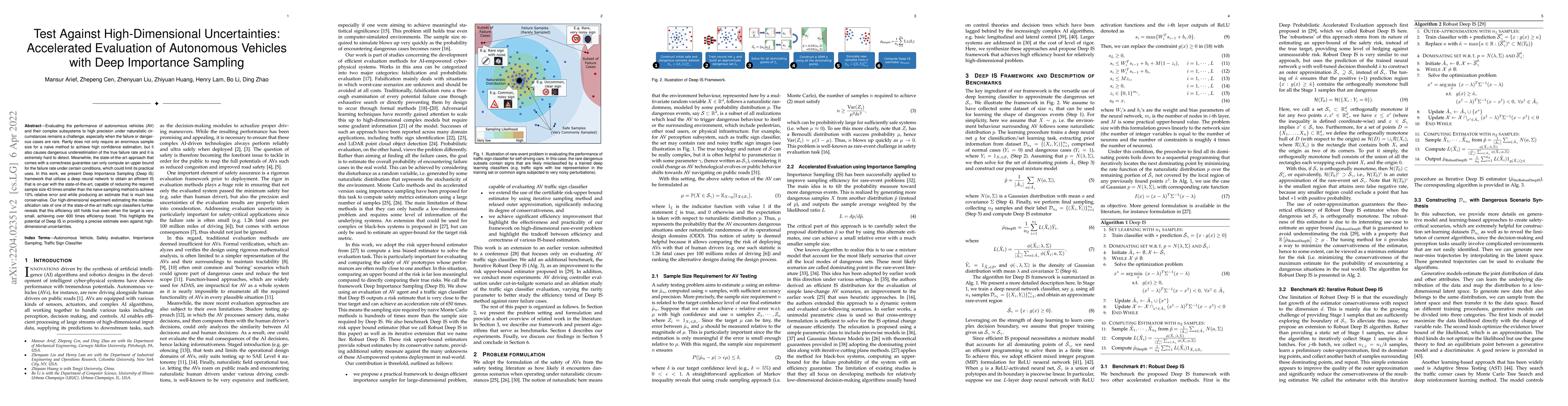

Evaluating the performance of autonomous vehicles (AV) and their complex subsystems to high precision under naturalistic circumstances remains a challenge, especially when failure or dangerous cases...

Simulation metamodeling refers to the construction of lower-fidelity models to represent input-output relations using few simulation runs. Stochastic kriging, which is based on Gaussian process, is ...

The bootstrap is a versatile inference method that has proven powerful in many statistical problems. However, when applied to modern large-scale models, it could face substantial computation demand ...

Bayesian bandit algorithms with approximate Bayesian inference have been widely used in real-world applications. However, there is a large discrepancy between the superior practical performance of t...

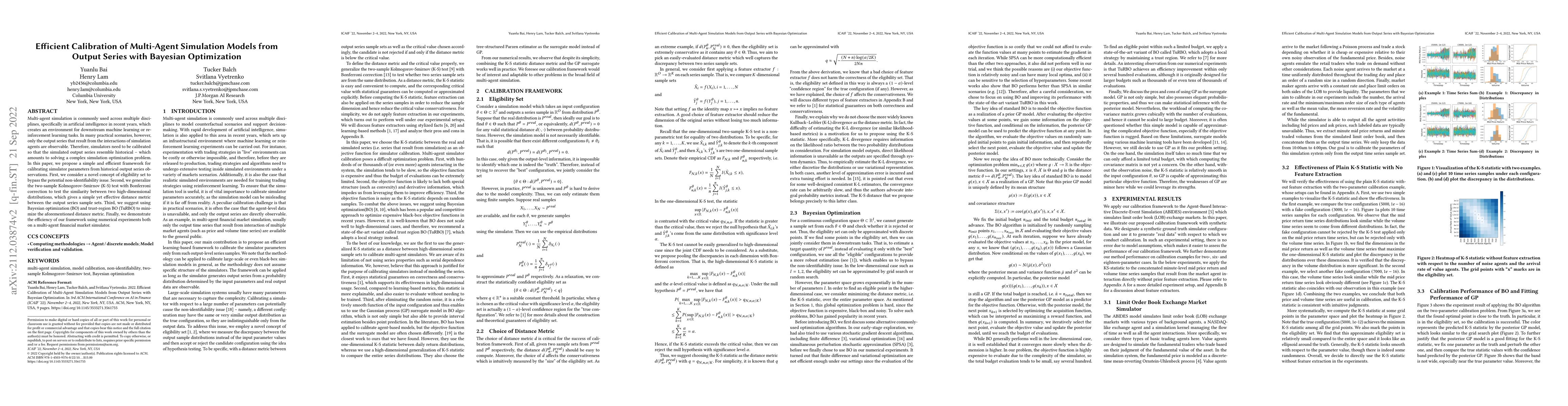

Multi-agent simulation is commonly used across multiple disciplines, specifically in artificial intelligence in recent years, which creates an environment for downstream machine learning or reinforc...

This paper studies a basic notion of distributional shape known as orthounimodality (OU) and its use in shape-constrained distributionally robust optimization (DRO). As a key motivation, we argue ho...

While batching methods have been widely used in simulation and statistics, it is open regarding their higher-order coverage behaviors and whether one variant is better than the others in this regard...

Rare-event simulation techniques, such as importance sampling (IS), constitute powerful tools to speed up challenging estimation of rare catastrophic events. These techniques often leverage the know...

In rare-event simulation, an importance sampling (IS) estimator is regarded as efficient if its relative error, namely the ratio between its standard deviation and mean, is sufficiently controlled. ...

Standard Monte Carlo computation is widely known to exhibit a canonical square-root convergence speed in terms of sample size. Two recent techniques, one based on control variate and one on importan...

Uncertainty quantification is at the core of the reliability and robustness of machine learning. In this paper, we provide a theoretical framework to dissect the uncertainty, especially the \textit{...

Distributionally robust optimization (DRO) is a worst-case framework for stochastic optimization under uncertainty that has drawn fast-growing studies in recent years. When the underlying probabilit...

Established approaches to obtain generalization bounds in data-driven optimization and machine learning mostly build on solutions from empirical risk minimization (ERM), which depend crucially on th...

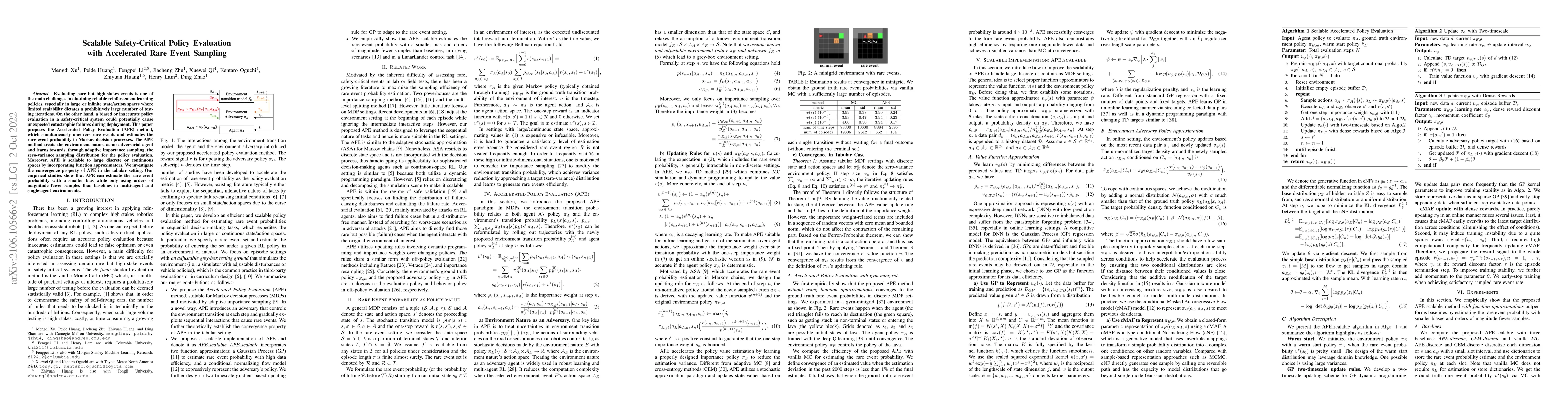

Evaluating rare but high-stakes events is one of the main challenges in obtaining reliable reinforcement learning policies, especially in large or infinite state/action spaces where limited scalabil...

When the underlying probability distribution in a stochastic optimization is observed only through data, various data-driven formulations have been studied to obtain approximate optimal solutions. W...

Stochastic simulation aims to compute output performance for complex models that lack analytical tractability. To ensure accurate prediction, the model needs to be calibrated and validated against r...

We consider stochastic gradient estimation using only black-box function evaluations, where the function argument lies within a probability simplex. This problem is motivated from gradient-descent o...

We investigate the feasibility of sample average approximation (SAA) for general stochastic optimization problems, including two-stage stochastic programming without the relatively complete recourse...

We study the generation of prediction intervals in regression for uncertainty quantification. This task can be formalized as an empirical constrained optimization problem that minimizes the average ...

In solving simulation-based stochastic root-finding or optimization problems that involve rare events, such as in extreme quantile estimation, running crude Monte Carlo can be prohibitively ineffici...

We study a methodology to tackle the NASA Langley Uncertainty Quantification Challenge, a model calibration problem under both aleatory and epistemic uncertainties. Our methodology is based on an in...

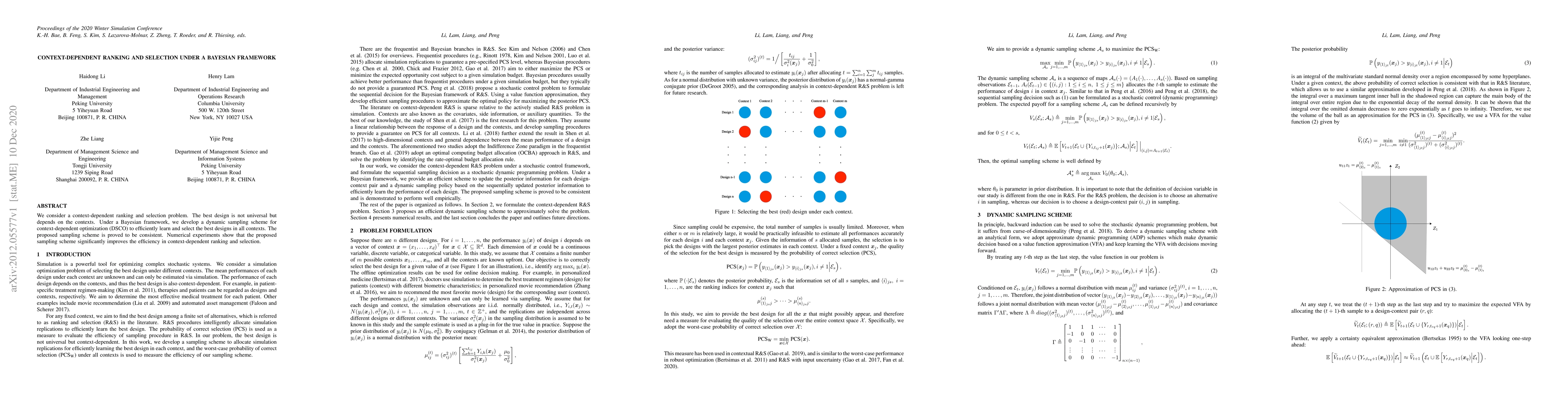

We consider a context-dependent ranking and selection problem. The best design is not universal but depends on the contexts. Under a Bayesian framework, we develop a dynamic sampling scheme for cont...

We study rare-event simulation for a class of problems where the target hitting sets of interest are defined via modern machine learning tools such as neural networks and random forests. This proble...

Quantile aggregation with dependence uncertainty has a long history in probability theory with wide applications in finance, risk management, statistics, and operations research. Using a recent resu...

We study a methodology to tackle the NASA Langley Uncertainty Quantification Challenge problem, based on an integration of robust optimization, more specifically a recent line of research known as d...

In many learning problems, the training and testing data follow different distributions and a particularly common situation is the \textit{covariate shift}. To correct for sampling biases, most appr...

We investigate statistical uncertainty quantification for reinforcement learning (RL) and its implications in exploration policy. Despite ever-growing literature on RL applications, fundamental ques...

In data-driven optimization, solution feasibility is often ensured through a "safe" reformulation of the uncertain constraints, such that an obtained data-driven solution is guaranteed to be feasibl...

In stochastic simulation, input uncertainty refers to the output variability arising from the statistical noise in specifying the input models. This uncertainty can be measured by a variance contrib...

We study a statistical method to estimate the optimal value, and the optimality gap of a given solution for stochastic optimization as an assessment of the solution quality. Our approach is based on...

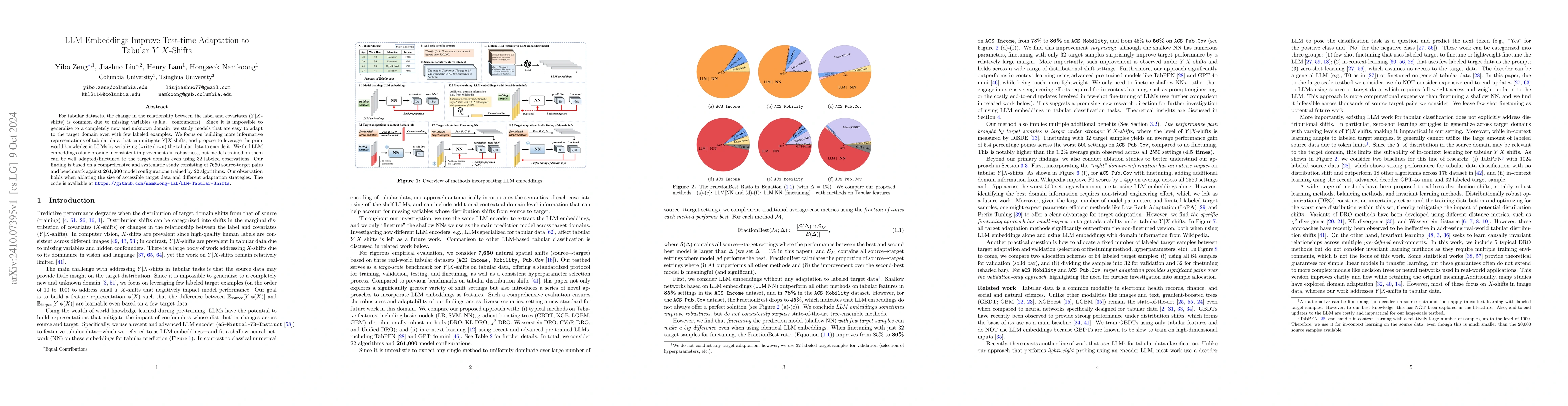

For tabular datasets, the change in the relationship between the label and covariates ($Y|X$-shifts) is common due to missing variables (a.k.a. confounders). Since it is impossible to generalize to a ...

Uncertainty quantification, by means of confidence interval (CI) construction, has been a fundamental problem in statistics and also important in risk-aware decision-making. In this paper, we revisit ...

Despite being an essential tool across engineering and finance, Monte Carlo simulation can be computationally intensive, especially in large-scale, path-dependent problems that hinder straightforward ...

Data-driven optimization aims to translate a machine learning model into decision-making by optimizing decisions on estimated costs. Such a pipeline can be conducted by fitting a distributional model ...

Importance Sampling (IS) is a widely used variance reduction technique for enhancing the efficiency of Monte Carlo methods, particularly in rare-event simulation and related applications. Despite its ...

Conformal prediction is a popular method to construct prediction intervals for black-box machine learning models with marginal coverage guarantees. In applications with potentially high-impact events,...

We introduce dro, an open-source Python library for distributionally robust optimization (DRO) for regression and classification problems. The library implements 14 DRO formulations and 9 backbone mod...

Data-driven stochastic optimization is ubiquitous in machine learning and operational decision-making problems. Sample average approximation (SAA) and model-based approaches such as estimate-then-opti...

The field of simulation optimization (SO) encompasses various methods developed to optimize complex, expensive-to-sample stochastic systems. Established methods include, but are not limited to, rankin...

Constrained simulation optimization (CSO) is a general framework for optimizing stochastic systems under performance constraints. It arises widely in practice where objective and constraint evaluation...