Academic Profile

Statistics

Similar Authors

Papers on arXiv

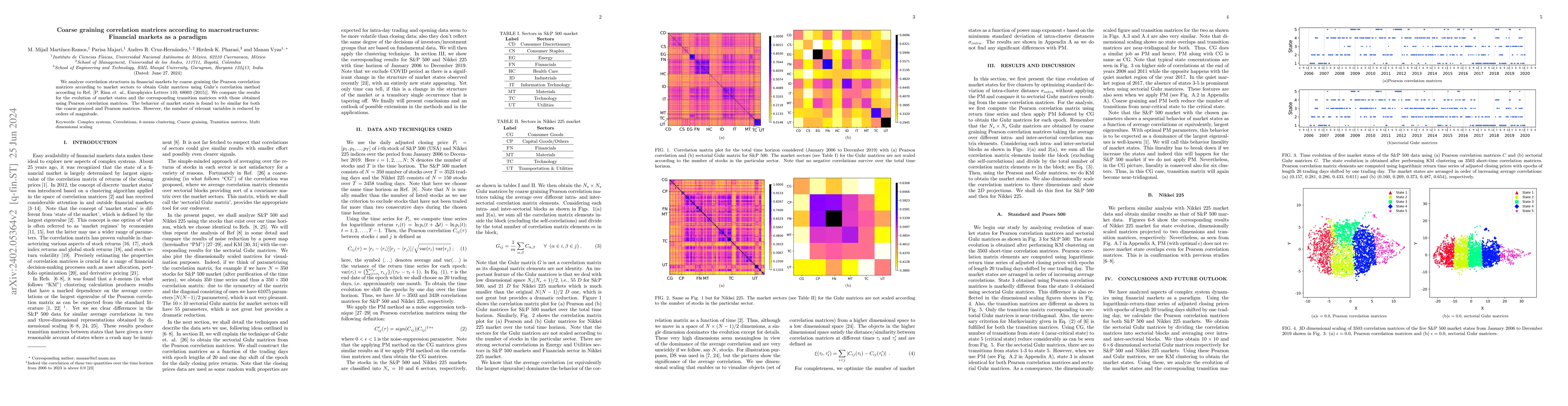

We analyze correlation structures in financial markets by coarse graining the Pearson correlation matrices according to market sectors to obtain Guhr matrices using Guhr's correlation method accordi...

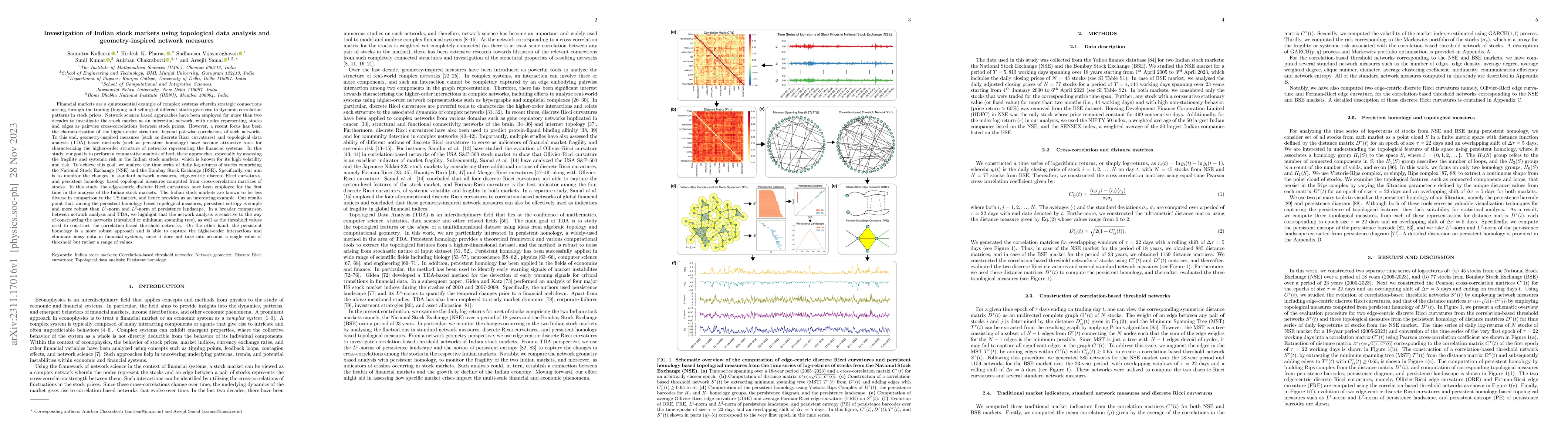

Geometry-inspired measures (such as discrete Ricci curvatures) and topological data analysis (TDA) based methods (such as persistent homology) have become attractive tools for characterizing the hig...

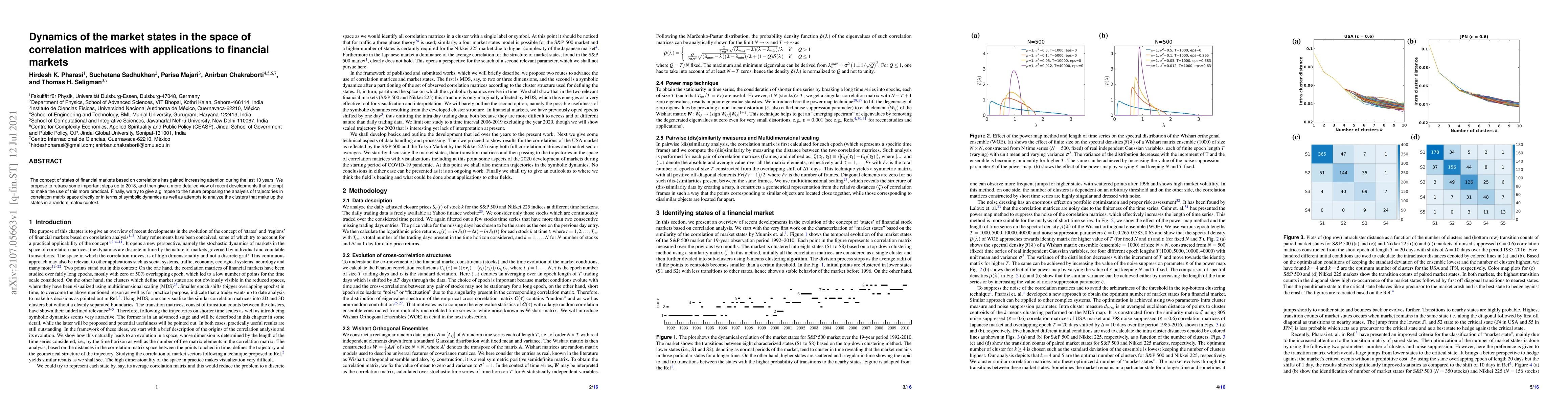

The concept of states of financial markets based on correlations has gained increasing attention during the last 10 years. We propose to retrace some important steps up to 2018, and then give a more...

Previous research explored various conditions of financial markets based on the similarity of correlation structures and classified as market states. We introduce modifications to previous selection...

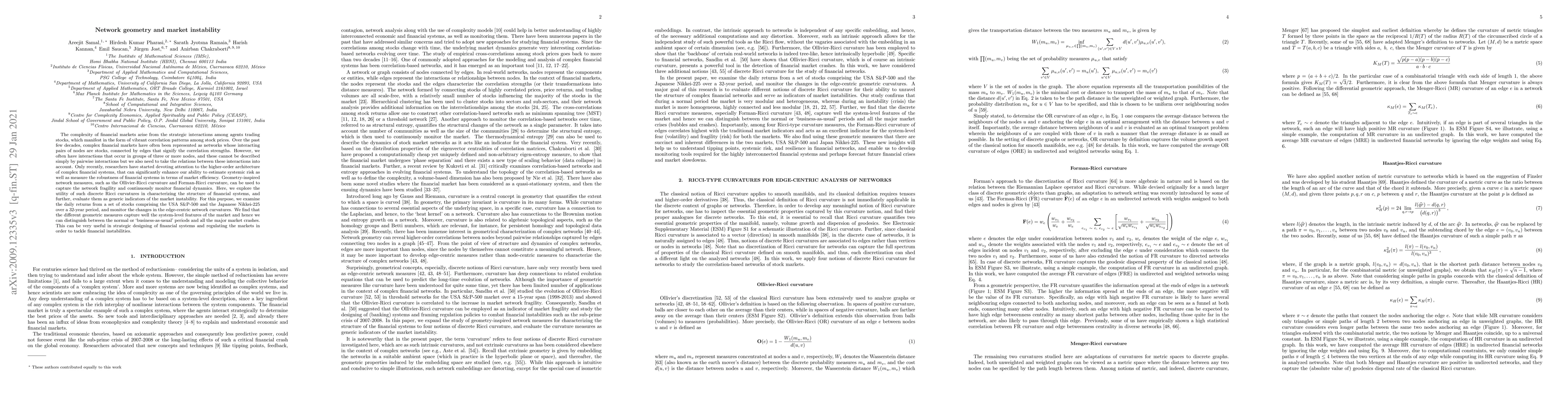

The complexity of financial markets arise from the strategic interactions among agents trading stocks, which manifest in the form of vibrant correlation patterns among stock prices. Over the past fe...

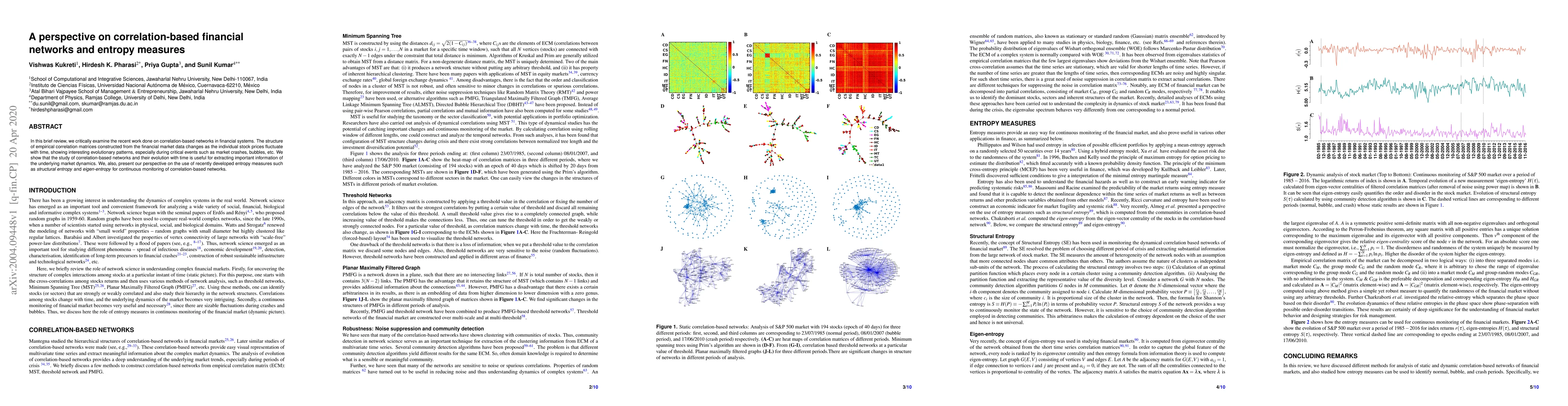

In this brief review, we critically examine the recent work done on correlation-based networks in financial systems. The structure of empirical correlation matrices constructed from the financial ma...

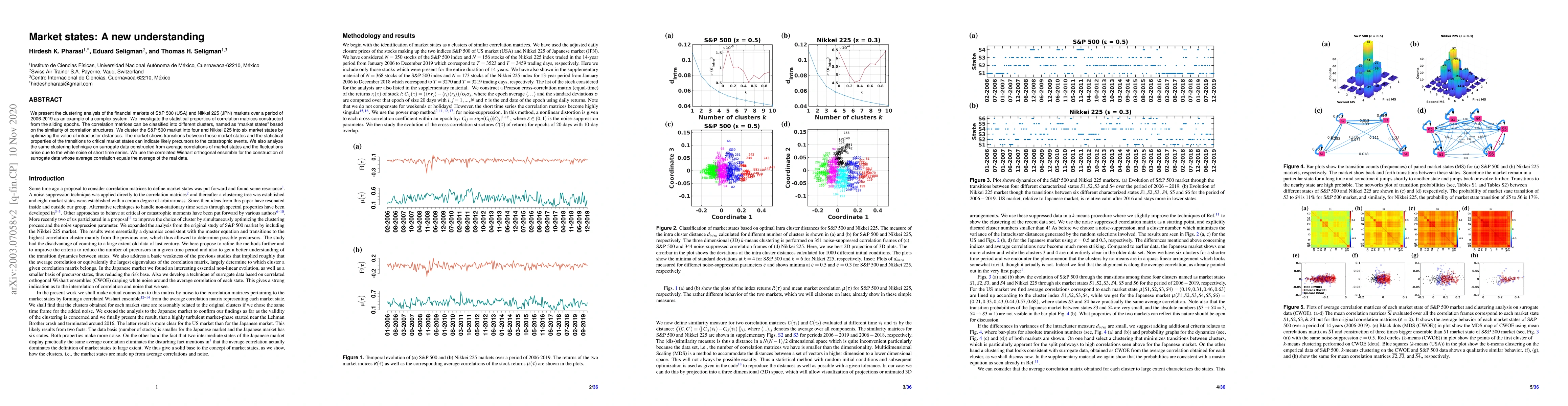

We present the clustering analysis of the financial markets of S&P 500 (USA) and Nikkei 225 (JPN) markets over a period of 2006-2019 as an example of a complex system. We investigate the statistical...

We investigate the impact of magnetic-field-induced feedback on the dynamics of a Hindmarsh-Rose neuron model exhibiting a blue-sky catastrophe. By introducing a magnetic flux variable that couples no...