Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we develop a hybrid approach to forecasting the volatility and risk of financial instruments by combining common econometric GARCH time series models with deep learning neural network...

This paper proposes a novel approach to hedging portfolios of risky assets when financial markets are affected by financial turmoils. We introduce a completely novel approach to diversification acti...

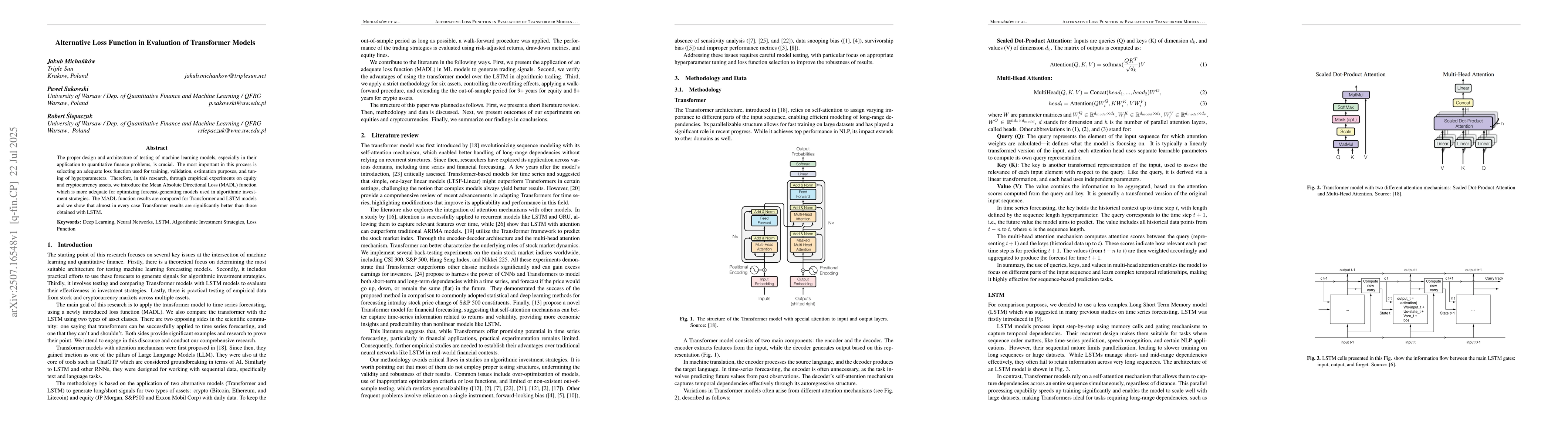

This paper investigates the issue of an adequate loss function in the optimization of machine learning models used in the forecasting of financial time series for the purpose of algorithmic investme...

Regardless of the selected asset class and the level of model complexity (Transformer versus LSTM versus Perceptron/RNN), the GMADL loss function produces superior results than standard MSE-type loss ...

The proper design and architecture of testing of machine learning models, especially in their application to quantitative finance problems, is crucial. The most important in this process is selecting ...

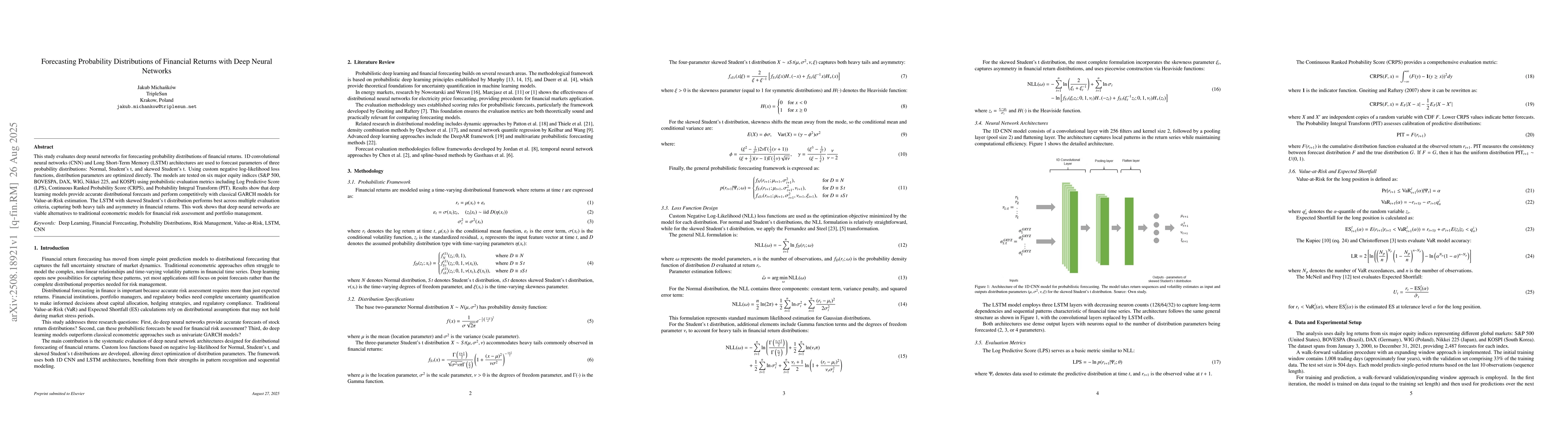

This study evaluates deep neural networks for forecasting probability distributions of financial returns. 1D convolutional neural networks (CNN) and Long Short-Term Memory (LSTM) architectures are use...

This paper explores the application of deep Q-learning to hedging at-the-money options on the S\&P~500 index. We develop an agent based on the Twin Delayed Deep Deterministic Policy Gradient (TD3) alg...

This thesis studies the use of randomized neural networks for the estimation of exposure profiles and unilateral CVA of American options within a Monte Carlo framework. The analysis is carried out sep...