Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper deals with tail diversification in financial time series through the concept of statistical independence by way of differential entropy and mutual information. By using moments as contras...

We look at optimal liability-driven portfolios in a family of fat-tailed and extremal risk measures, especially in the context of pension fund and insurance fixed cashflow liability profiles, but al...

A fundamental bottleneck in utilising complex machine learning systems for critical applications has been not knowing why they do and what they do, thus preventing the development of any crucial saf...

Portfolio optimization methods suffer from a catalogue of known problems, mainly due to the facts that pair correlations of asset returns are unstable, and that extremal risk measures such as maximu...

Standard, PCA-based factor analysis suffers from a number of well known problems due to the random nature of pairwise correlations of asset returns. We analyse an alternative based on ICA, where fac...

We introduce the new "Goldilocks" class of activation functions, which non-linearly deform the input signal only locally when the input signal is in the appropriate range. The small local deformatio...

We present a class of macroscopic models of the Limit Order Book to simulate the aggregate behaviour of market makers in response to trading flows. The resulting models are solved numerically and as...

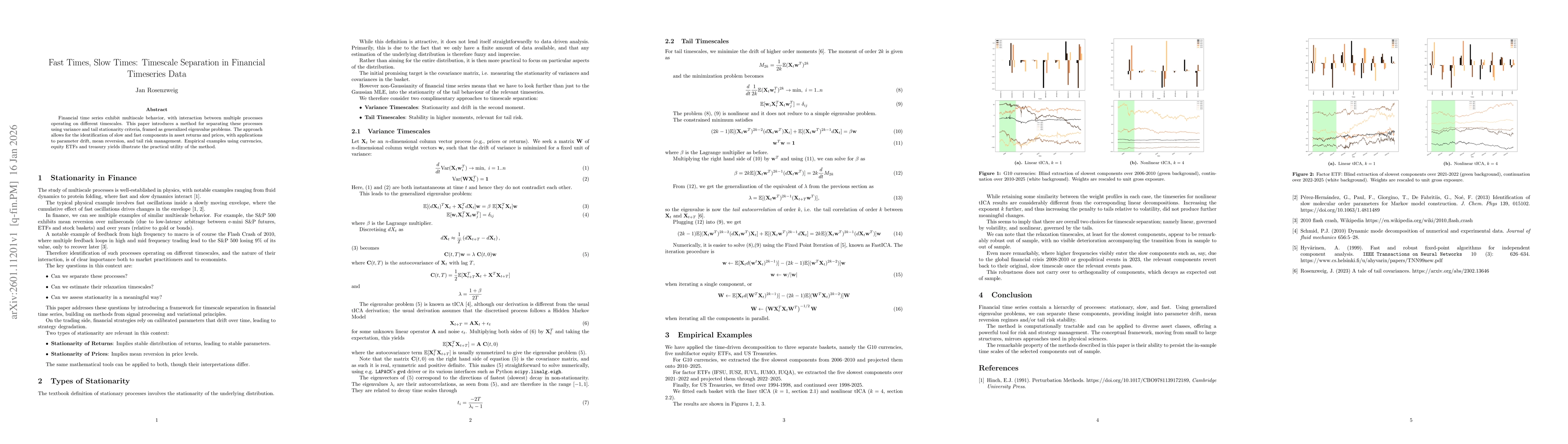

Financial time series exhibit multiscale behavior, with interaction between multiple processes operating on different timescales. This paper introduces a method for separating these processes using va...