Academic Profile

Statistics

Similar Authors

Papers on arXiv

Accurately estimating income Pareto exponents is challenging due to limitations in data availability and the applicability of statistical methods. Using tabulated summaries of incomes from tax autho...

Administrative data are often easier to access as tabulated summaries than in the original format due to confidentiality concerns. Motivated by this practical feature, we propose a novel nonparametr...

We develop a novel fixed-k tail regression method that accommodates the unique feature in the Forbes 400 data that observations are truncated from below at the 400th largest order statistic. Applyin...

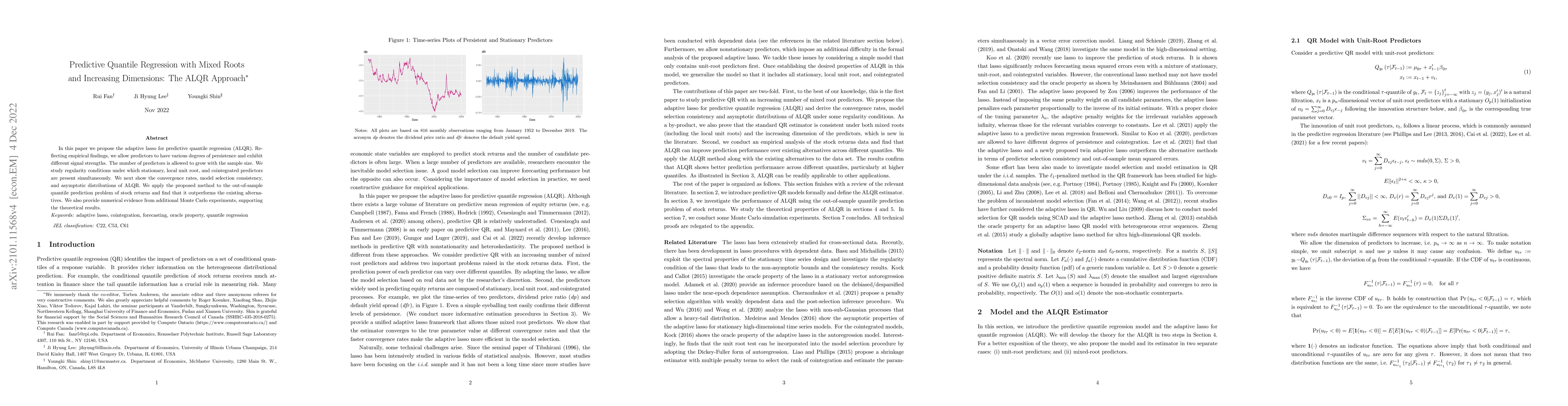

In this paper we propose the adaptive lasso for predictive quantile regression (ALQR). Reflecting empirical findings, we allow predictors to have various degrees of persistence and exhibit different...

We propose a novel conditional quantile prediction method based on complete subset averaging (CSA) for quantile regressions. All models under consideration are potentially misspecified and the dimen...

Explanatory variables in a predictive regression typically exhibit low signal strength and various degrees of persistence. Variable selection in such a context is of great importance. In this paper,...

This paper advances a variable screening approach to enhance conditional quantile forecasts using high-dimensional predictors. We have refined and augmented the quantile partial correlation (QPC)-base...

We analyse growth vulnerabilities in the US using quantile partial correlation regression, a selection-based machine-learning method that achieves model selection consistency under time series. We fin...