Academic Profile

Statistics

Similar Authors

Papers on arXiv

We use house prices (HP) and house price indices (HPI) as a proxy to income distribution. Specifically, we analyze sale prices in the 1970-2010 window of over 116,000 single-family homes in Hamilton...

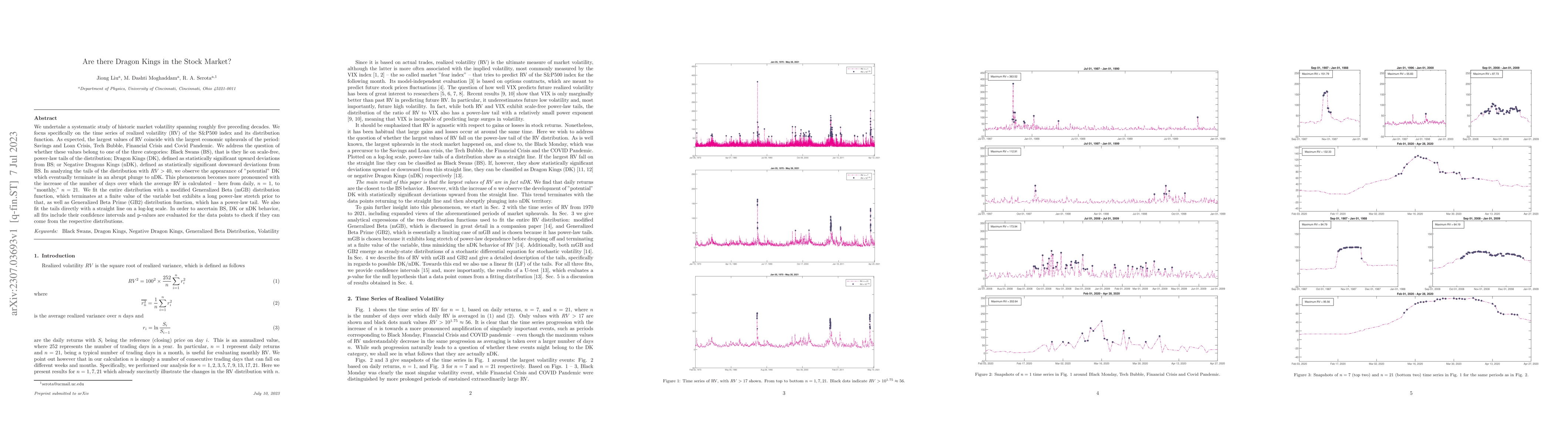

We undertake a systematic study of historic market volatility spanning roughly five preceding decades. We focus specifically on the time series of realized volatility (RV) of the S&P500 index and it...

Data scarcity and heterogeneity pose significant performance challenges for personalized federated learning, and these challenges are mainly reflected in overfitting and low precision in existing me...

We approach the Generalized Beta (GB) family of distributions using a mean-reverting stochastic differential equation (SDE) for a power of the variable, whose steady-state (stationary) probability d...

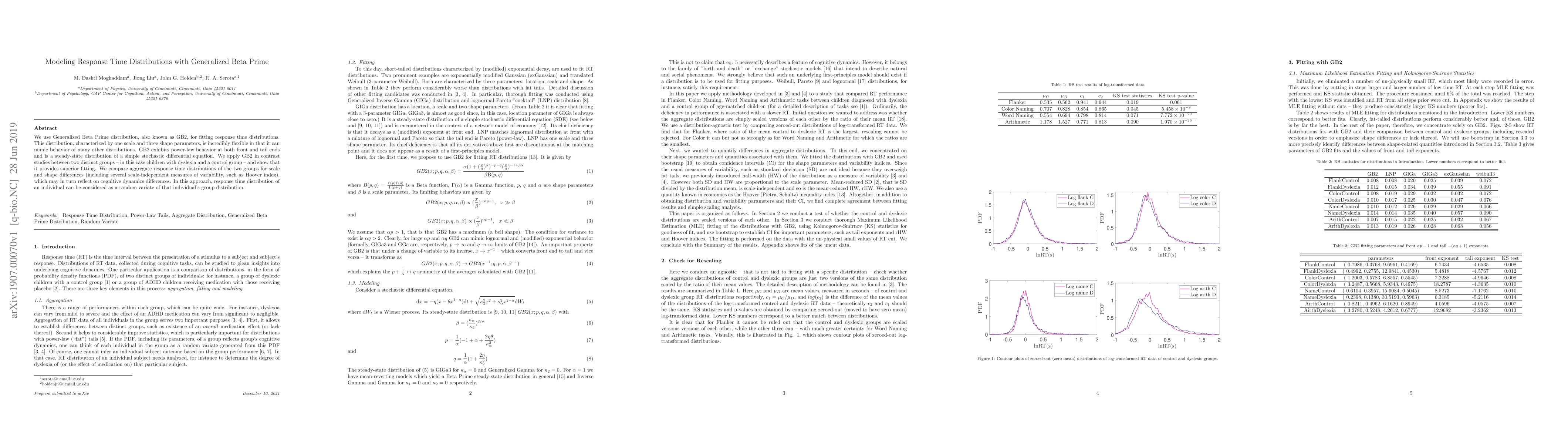

We use Generalized Beta Prime distribution, also known as GB2, for fitting response time distributions. This distribution, characterized by one scale and three shape parameters, is incredibly flexib...

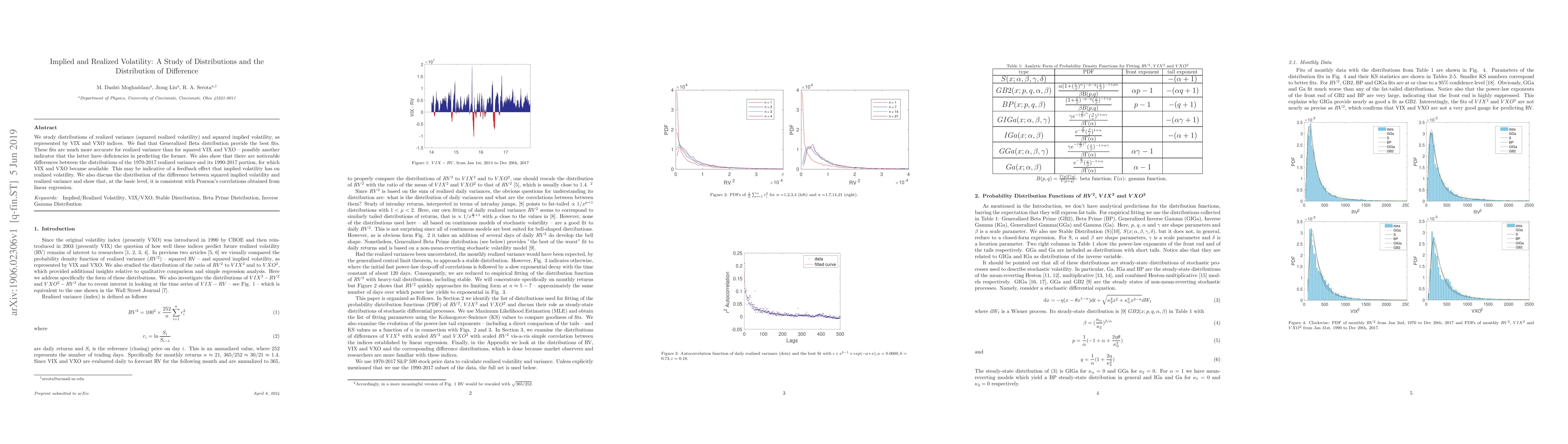

We study distributions of realized variance (squared realized volatility) and squared implied volatility, as represented by VIX and VXO indices. We find that Generalized Beta distribution provide th...

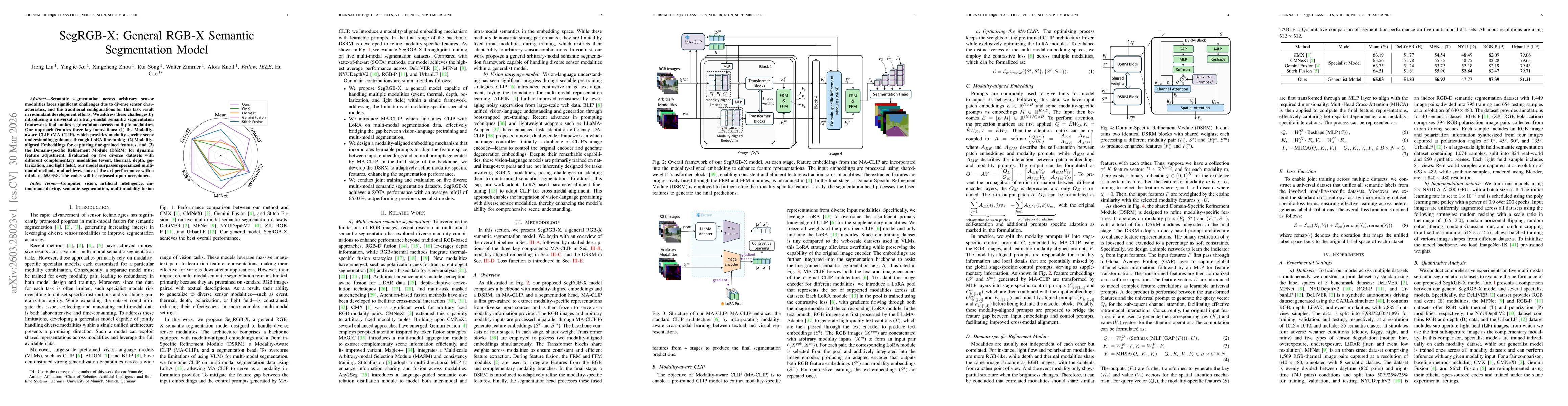

Semantic segmentation across arbitrary sensor modalities faces significant challenges due to diverse sensor characteristics, and the traditional configurations for this task result in redundant develo...

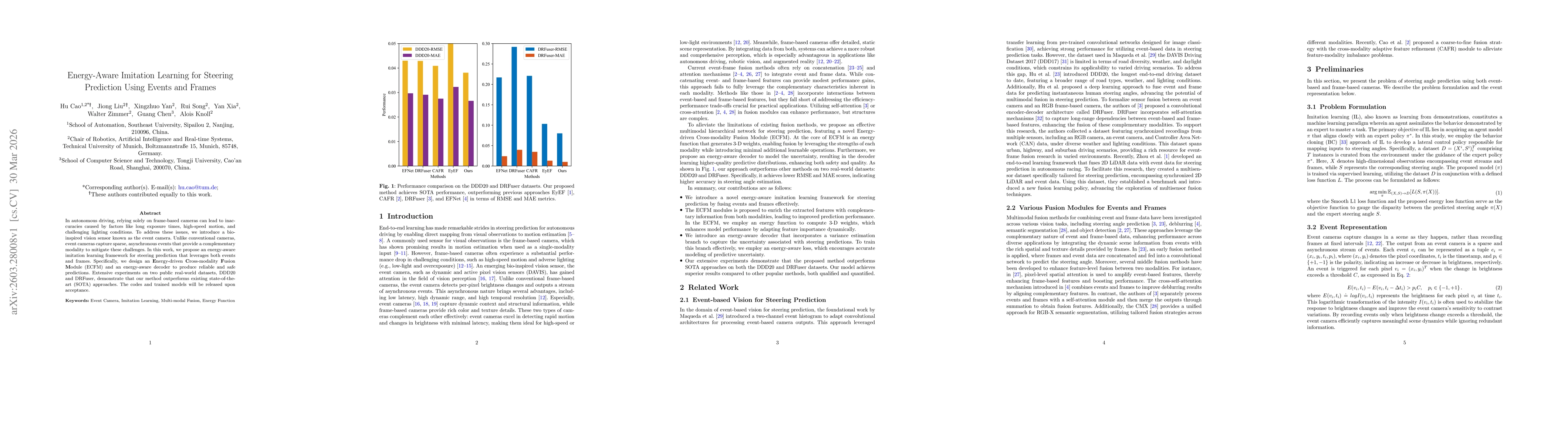

In autonomous driving, relying solely on frame-based cameras can lead to inaccuracies caused by factors like long exposure times, high-speed motion, and challenging lighting conditions. To address the...