Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a novel machine learning approach to probabilistic forecasting of hourly day-ahead electricity prices. In contrast to recent advances in data-rich probabilistic forecasting that approxima...

We identify a new type of risk, common firm-level investor fears, from commonalities within the cross-sectional distribution of individual stock options. We define firm-level fears that link with up...

This paper presents a model for smoothly varying heterogeneous persistence of economic data. We argue that such dynamics arise naturally from the dynamic nature of economic shocks with various degre...

We identify a new type of risk that is characterised by commonalities in the quantiles of the cross-sectional distribution of asset returns. Our newly proposed quantile risk factor is associated wit...

We propose a deep learning approach to probabilistic forecasting of macroeconomic and financial time series. Being able to learn complex patterns from a data rich environment, our approach is useful...

Using intraday data for the cross-section of individual stocks, we show that both transitory and persistent fluctuations in realized market and average idiosyncratic volatility, skewness and kurtosi...

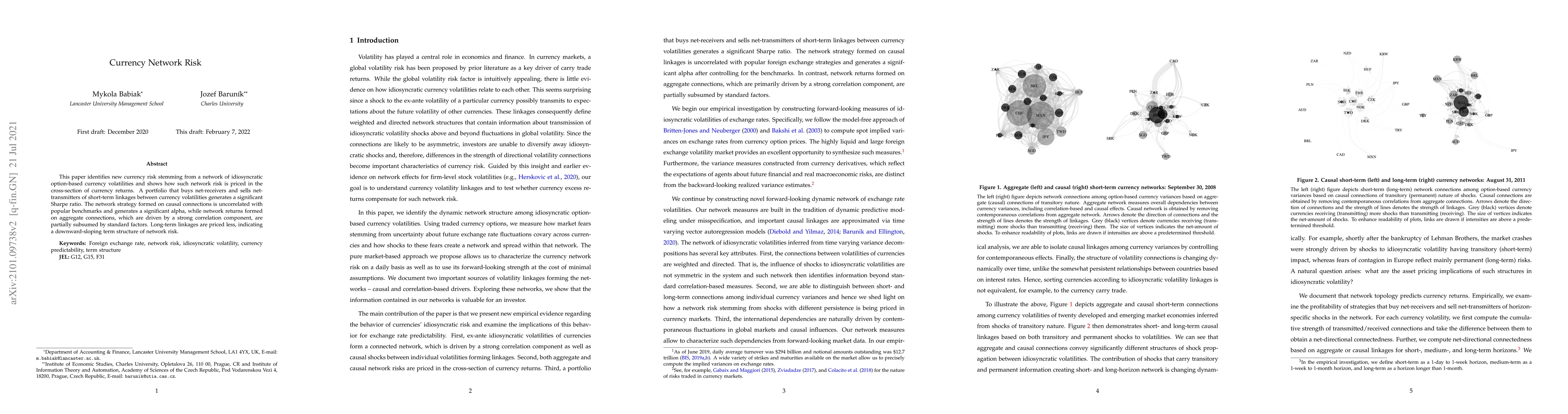

This paper identifies new currency risk stemming from a network of idiosyncratic option-based currency volatilities and shows how such network risk is priced in the cross-section of currency returns...

We argue that uncertainty network structures extracted from option prices contain valuable information for business cycles. Classifying U.S. industries according to their contribution to system-rela...

We study dynamic portfolio choice of a long-horizon investor who uses deep learning methods to predict equity returns when forming optimal portfolios. Our results show statistically and economically...

This paper characterises dynamic linkages arising from shocks with heterogeneous degrees of persistence. Using frequency domain techniques, we introduce measures that identify smoothly varying links...

Dramatic growth of investment disputes between foreign investors and host states rises serious questions about the impact of those disputes on investors. This paper is the first to explain increased...

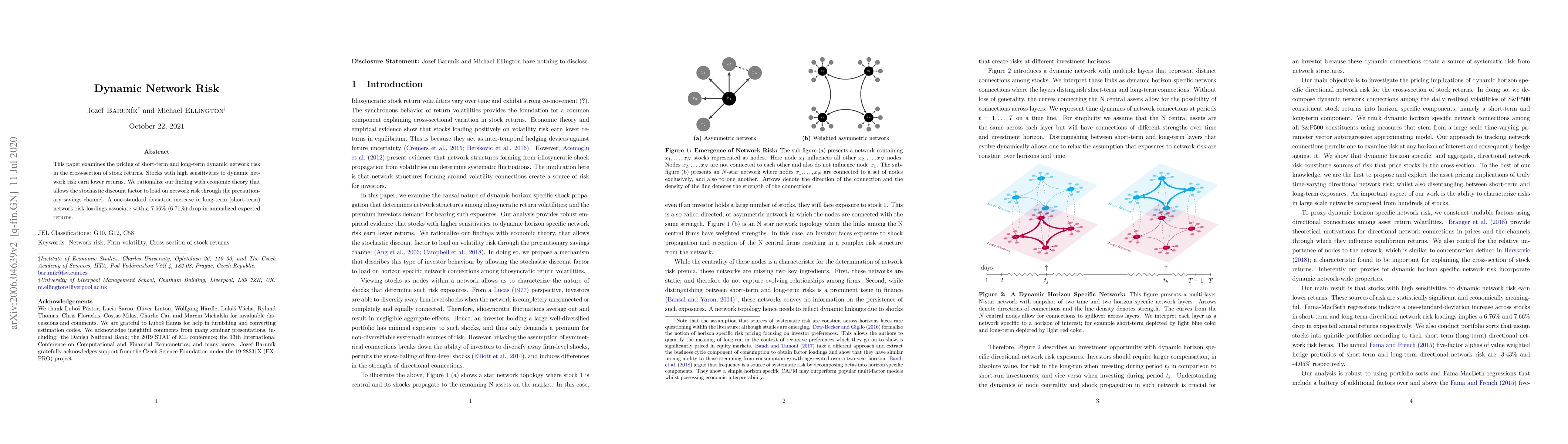

This paper examines the pricing of short-term and long-term dynamic network risk in the cross-section of stock returns. Stocks with high sensitivities to dynamic network risk earn lower returns. We ...

We propose how to quantify high-frequency market sentiment using high-frequency news from NASDAQ news platform and support vector machine classifiers. News arrive at markets randomly and the resulti...

This paper introduces forward-looking measures of the network connectedness of fears in the financial system, arising due to the good and bad beliefs of market participants about uncertainty that sp...

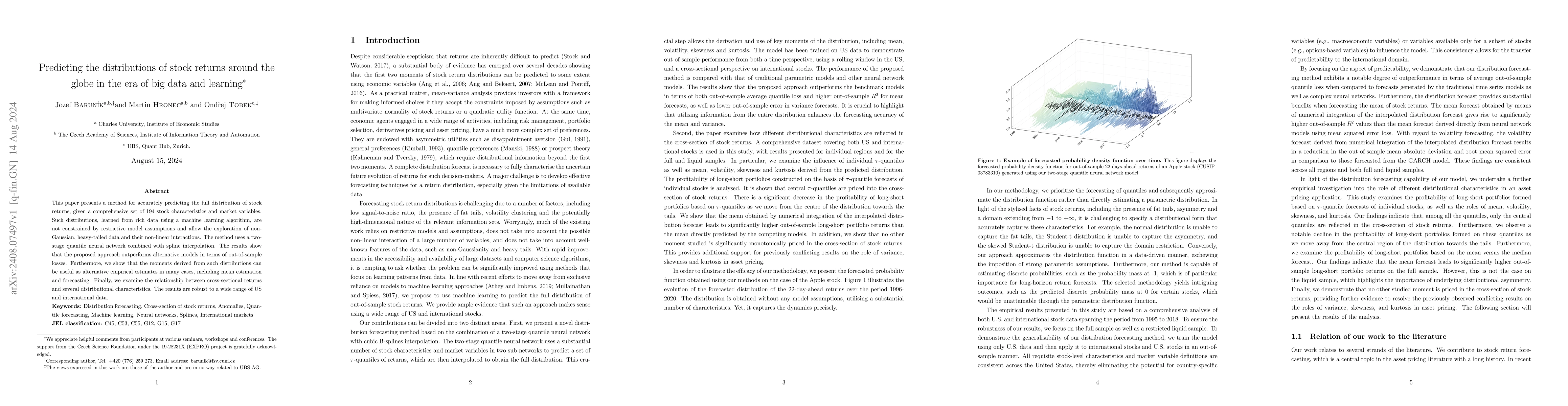

This paper presents a method for accurately predicting the full distribution of stock returns, given a comprehensive set of 194 stock characteristics and market variables. Such distributions, learned ...

We study the dynamic investment decisions of investors who prioritise specific quantiles of outcomes over their expected values. Downside-focused agents targeting low quantiles reduce risk in states w...

This paper studies the impact of funding market frictions on bond prices and market-wide liquidity. Using proprietary transaction-level data on all gilt-backed repo and reverse-repo trades, we demonst...

Cross-sectional dispersion in firm-level realized skewness is significantly and negatively related to future stock market returns. The predictive power of skewness dispersion is robust to in-sample an...