Academic Profile

Statistics

Similar Authors

Papers on arXiv

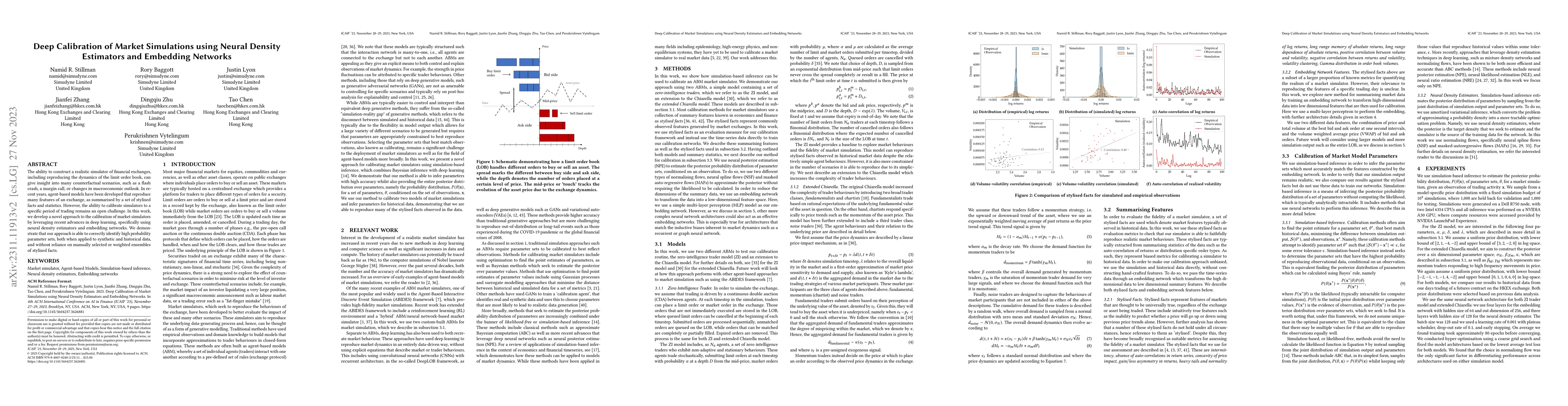

The ability to construct a realistic simulator of financial exchanges, including reproducing the dynamics of the limit order book, can give insight into many counterfactual scenarios, such as a flas...

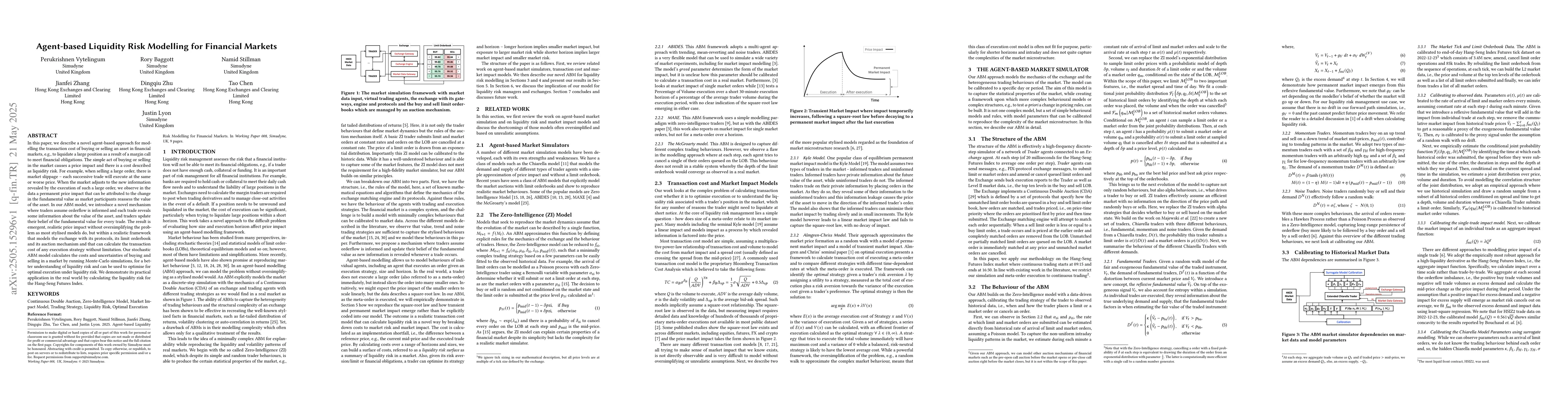

In this paper, we describe a novel agent-based approach for modelling the transaction cost of buying or selling an asset in financial markets, e.g., to liquidate a large position as a result of a marg...

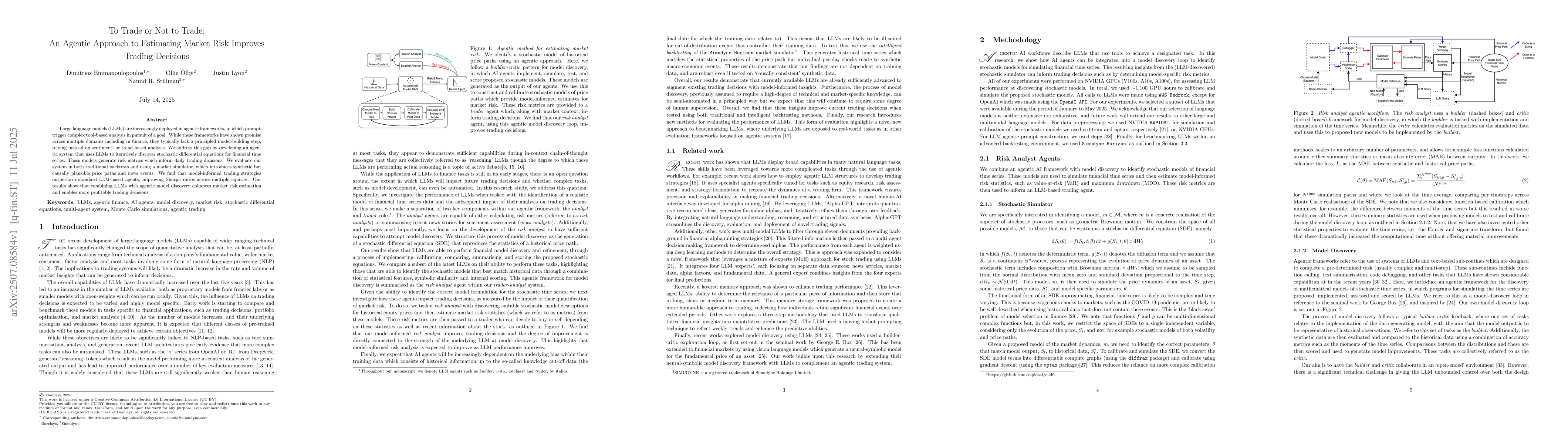

Large language models (LLMs) are increasingly deployed in agentic frameworks, in which prompts trigger complex tool-based analysis in pursuit of a goal. While these frameworks have shown promise acros...