Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a new method for finding statistical arbitrages that can contain more assets than just the traditional pair. We formulate the problem as seeking a portfolio with the highest volatility, s...

More than seventy years ago Harry Markowitz formulated portfolio construction as an optimization problem that trades off expected return and risk, defined as the standard deviation of the portfolio ...

We consider the well-studied problem of predicting the time-varying covariance matrix of a vector of financial returns. Popular methods range from simple predictors like rolling window or exponentia...

The multi-armed bandit(MAB) problem is a simple yet powerful framework that has been extensively studied in the context of decision-making under uncertainty. In many real-world applications, such as...

This paper considers centralized mission-planning for a heterogeneous multi-agent system with the aim of locating a hidden target. We propose a mixed observable setting, consisting of a fully observ...

We consider the problem of managing a portfolio of moving-band statistical arbitrages (MBSAs), inspired by the Markowitz optimization framework. We show how to manage a dynamic basket of MBSAs, and il...

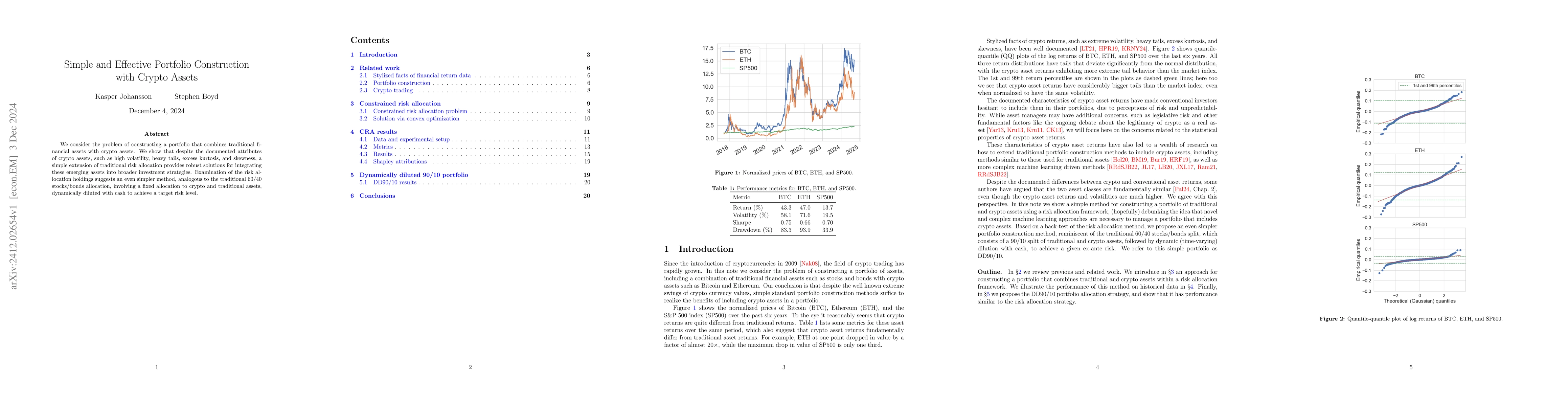

We consider the problem of constructing a portfolio that combines traditional financial assets with crypto assets. We show that despite the documented attributes of crypto assets, such as high volatil...

The retirement funding problem addresses the question of how to manage a retiree's savings to provide her with a constant post-tax inflation adjusted consumption throughout her lifetime. This consists...