Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the fixed-confidence best arm identification (FC-BAI) problem in the Bayesian setting. This problem aims to find the arm of the largest mean with a fixed confidence level when the bandit m...

We revisit the dividend payment problem in the dual model of Avanzi et al. ([2], [1], and [3]). Using the fluctuation theory of spectrally positive L\'{e}vy processes, we give a short exposition in ...

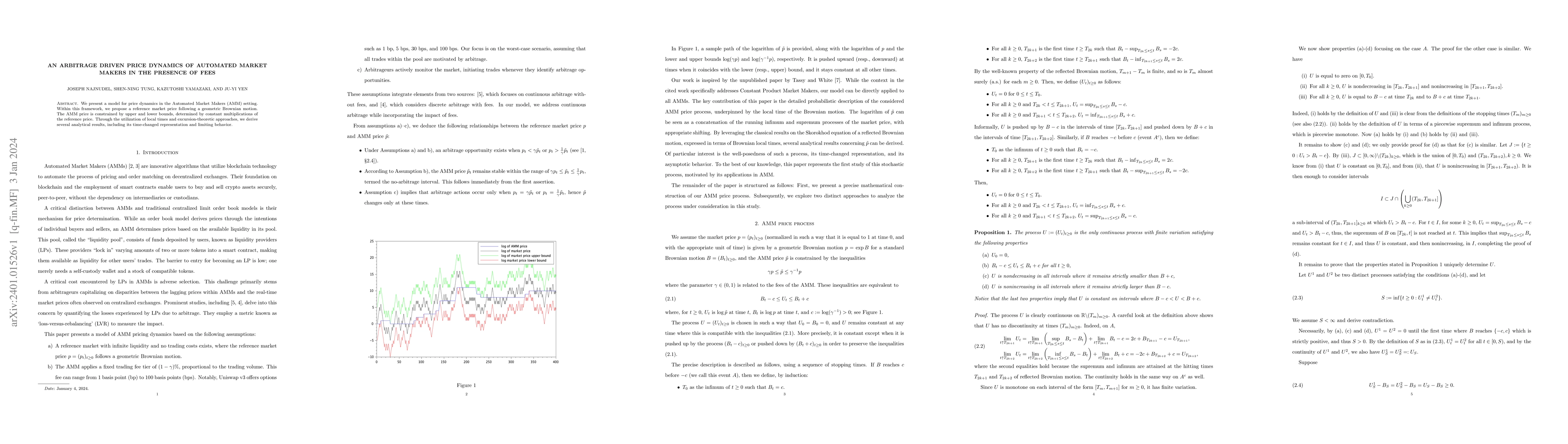

We present a model for price dynamics in the Automated Market Makers (AMM) setting. Within this framework, we propose a reference market price following a geometric Brownian motion. The AMM price is...

We revisit an absolutely-continuous version of the stochastic control problem driven by a L\'evy process. A strategy must be absolutely continuous with respect to the Lebesgue measure and the runnin...

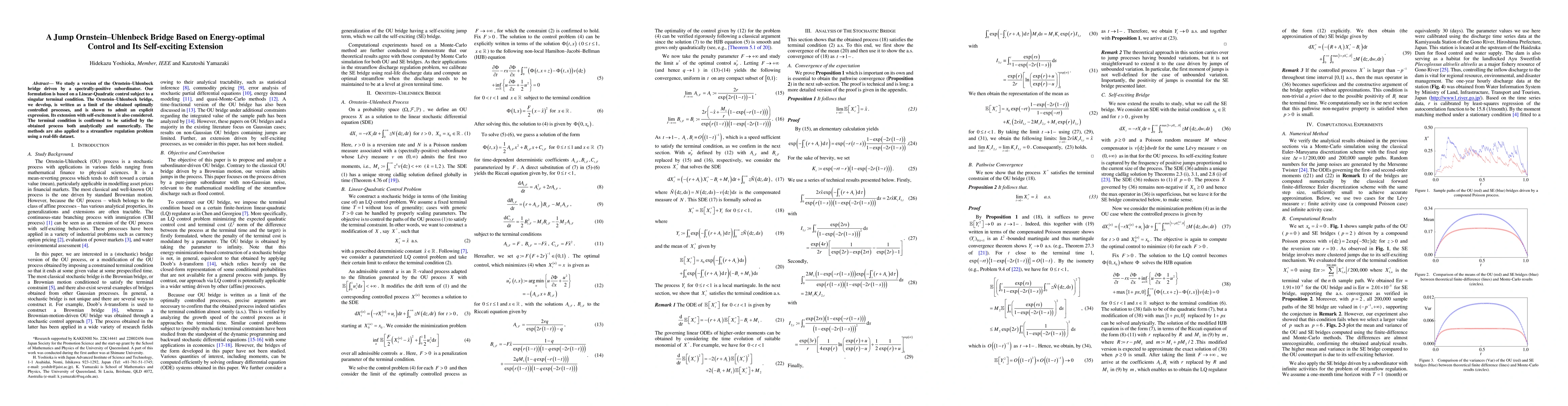

We study a version of the Ornstein-Uhlenbeck bridge driven by a spectrally-positive subordinator. Our formulation is based on a Linear-Quadratic control subject to a singular terminal condition. The...

We consider a version of the continuous-time multi-armed bandit problem where decision opportunities arrive at Poisson arrival times, and study its Gittins index policy. When driven by spectrally on...

The Gerber-Shiu function provides a unified framework for the evaluation of a variety of risk quantities. Ever since its establishment, it has attracted constantly increasing interests in actuarial ...

We introduce a new Levy fluctuation theoretic method to analyze the cumulative sum (CUSUM) procedure in sequential change-point detection. When observations are phase-type distributed and the post-c...

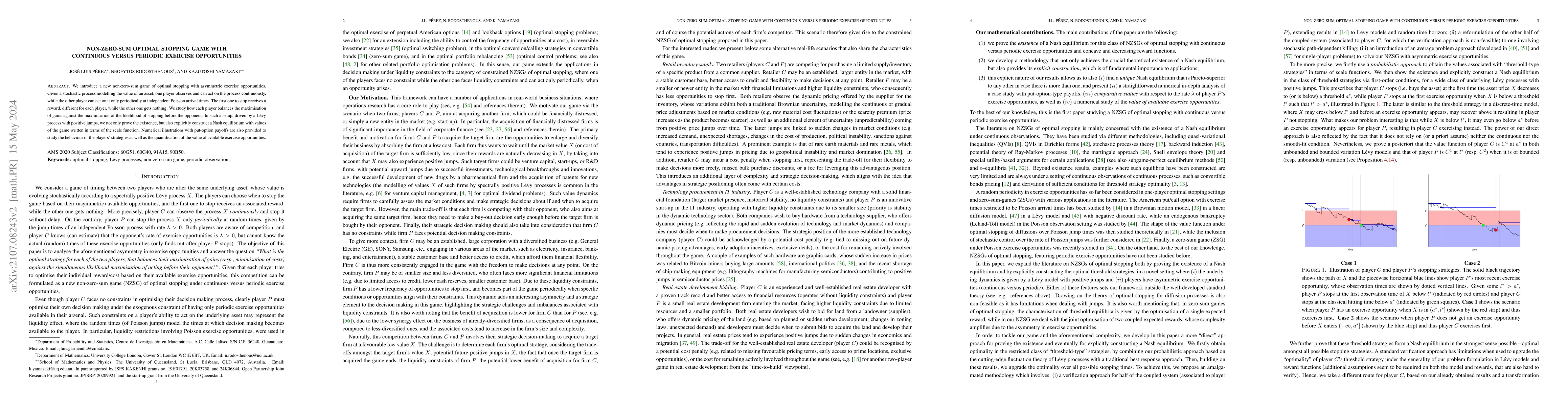

We introduce a new non-zero-sum game of optimal stopping with asymmetric exercise opportunities. Given a stochastic process modelling the value of an asset, one player observes and can act on the pr...

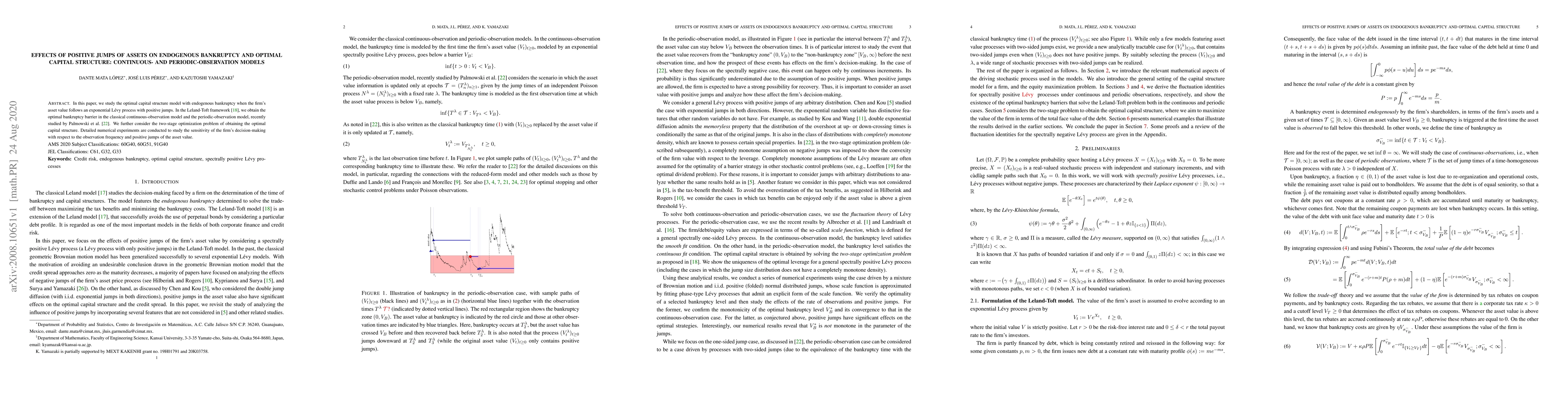

In this paper, we study the optimal capital structure model with endogenous bankruptcy when the firm's asset value follows an exponential L\'evy process with positive jumps. In the Leland-Toft frame...

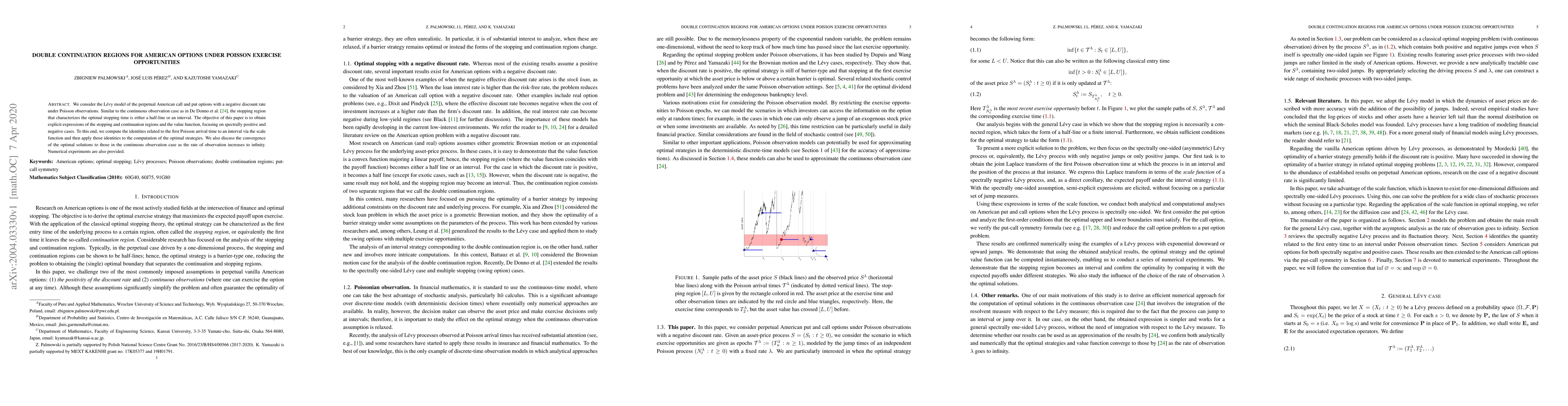

We consider the L\'evy model of the perpetual American call and put options with a negative discount rate under Poisson observations. Similar to the continuous observation case as in De Donno et al....

We consider de Finetti's problem for spectrally one-sided L\'evy risk models with control strategies that are absolutely continuous with respect to the Lebesgue measure. Furthermore, we consider the...

In this paper, we examine a modified version of de Finetti's optimal dividend problem, incorporating fixed transaction costs and altering the surplus process by introducing two-valued drift and two-va...

We study a stochastic control problem where the underlying process follows a spectrally negative L\'{e}vy process. A controller can continuously increase the process but only decrease it at independen...

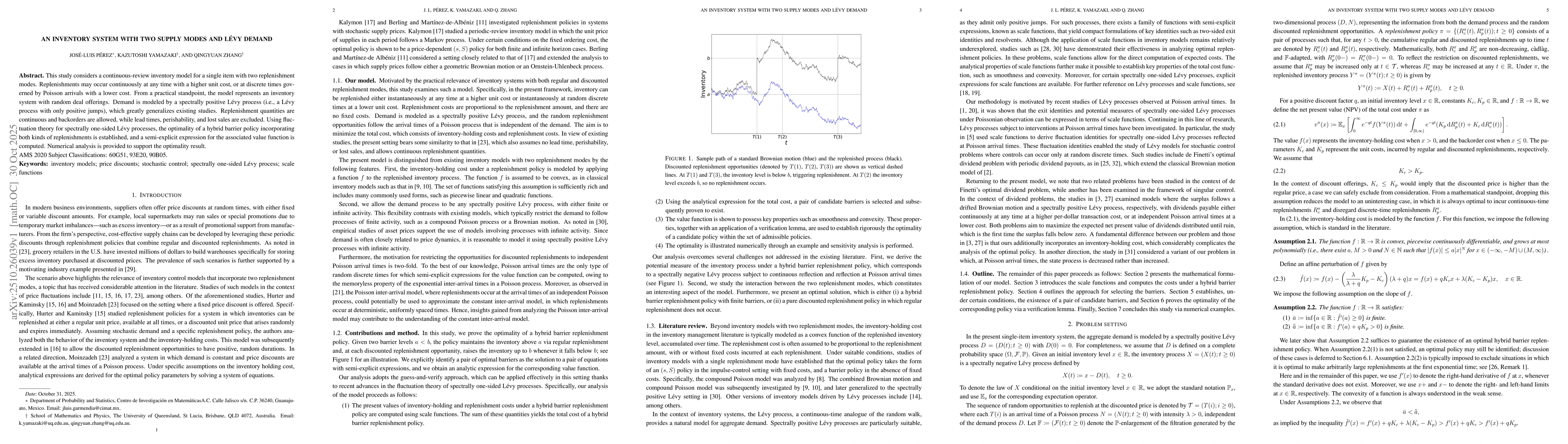

This study considers a continuous-review inventory model for a single item with two replenishment modes. Replenishments may occur continuously at any time with a higher unit cost, or at discrete times...

This paper examines multi-armed bandits in which actions are taken at random discrete times. The model consists of $J$ independent arms. When an arm is operated, it must remain active for a random dur...