Non-zero-sum optimal stopping game with continuous versus periodic exercise opportunities

Publication

Metrics

AI Quick Summary

This paper explores a non-zero-sum optimal stopping game where one player has continuous exercise opportunities and the other only periodic ones. It proves the existence of a Nash equilibrium and constructs explicit solutions using scale functions, with numerical examples illustrating player strategies and the value of exercise opportunities.

Paper Preview

Abstract

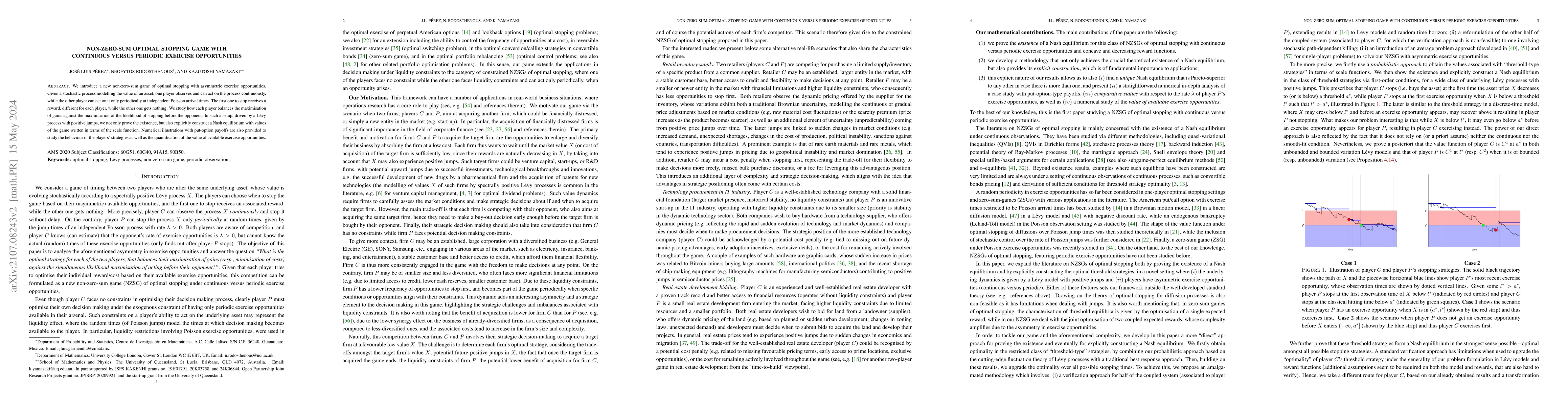

We introduce a new non-zero-sum game of optimal stopping with asymmetric exercise opportunities. Given a stochastic process modelling the value of an asset, one player observes and can act on the process continuously, while the other player can act on it only periodically at independent Poisson arrival times. The first one to stop receives a reward, different for each player, while the other one gets nothing. We study how each player balances the maximisation of gains against the maximisation of the likelihood of stopping before the opponent. In such a setup, driven by a L\'evy process with positive jumps, we not only prove the existence, but also explicitly construct a Nash equilibrium with values of the game written in terms of the scale function. Numerical illustrations with put-option payoffs are also provided to study the behaviour of the players' strategies as well as the quantification of the value of available exercise opportunities.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Paper Details

Authors

PDF Preview

Key Terms

Related Papers

No references found for this paper.

Discussion 0