Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a non-zero-sum game between a government and a legislative body to study the optimal level of debt. Each player, with different time preferences, can intervene on the stochastic dynamic...

The socioeconomic impact of pollution naturally comes with uncertainty due to, e.g., current new technological developments in emissions' abatement or demographic changes. On top of that, the trend ...

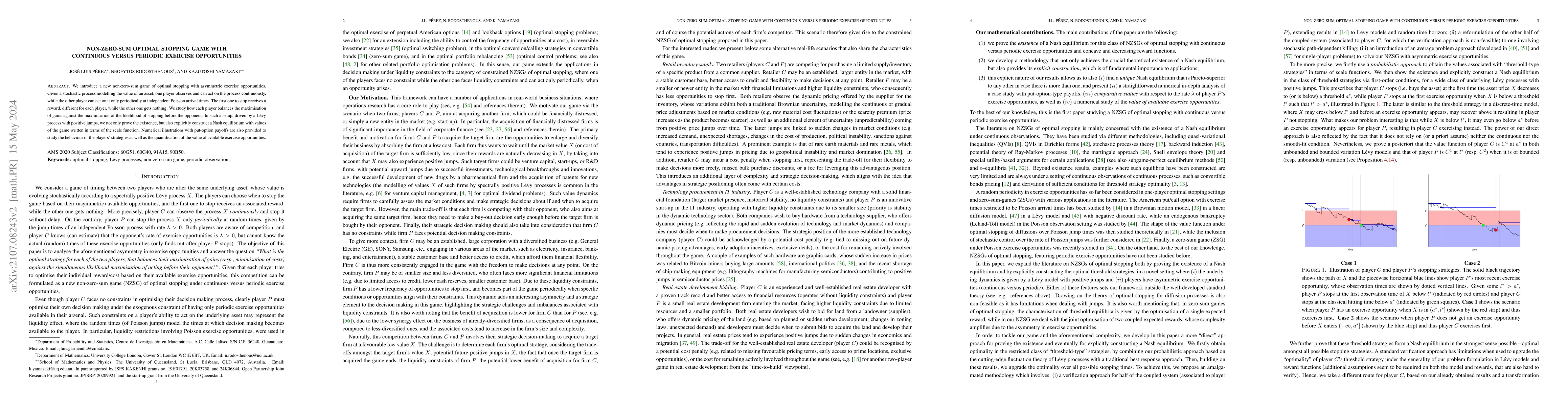

We introduce a new non-zero-sum game of optimal stopping with asymmetric exercise opportunities. Given a stochastic process modelling the value of an asset, one player observes and can act on the pr...

We study the problem of optimally managing an inventory with unknown demand trend. Our formulation leads to a stochastic control problem under partial observation, in which a Brownian motion with no...

We describe the bailout of banks by governments as a Markov Decision Process (MDP) where the actions are equity investments. The underlying dynamics is derived from the network of financial institut...

We consider risk averse investors with different levels of anxiety about asset price drawdowns. The latter is defined as the distance of the current price away from its best performance since incept...

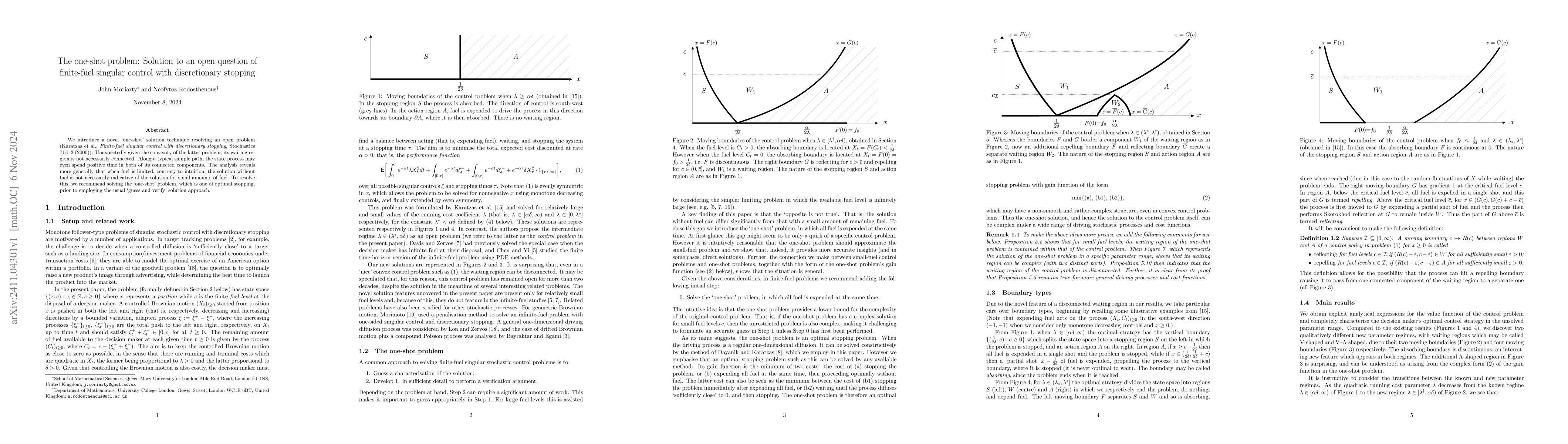

We introduce a novel 'one-shot' solution technique resolving an open problem (Karatzas et al., Finite-fuel singular control with discretionary stopping, Stochastics 71:1-2 (2000)). Unexpectedly given ...

We study a class of singular stochastic control problems for a one-dimensional diffusion $X$ in which the performance criterion to be optimised depends explicitly on the running infimum $I$ (or suprem...

The maximality principle has been a valuable tool in identifying the free-boundary functions that are associated with the solutions to several optimal stopping problems involving one-dimensional time-...

We study a time-inconsistent singular stochastic control problem for a general one-dimensional diffusion, where time-inconsistency arises from a non-exponential discount function. To address this, we ...

This paper extends the classical dividend problem by incorporating a novel, path-dependent mechanism of firm default. In the traditional framework, ruin occurs when the surplus process first reaches z...