Statistics

Similar Authors

Papers on arXiv

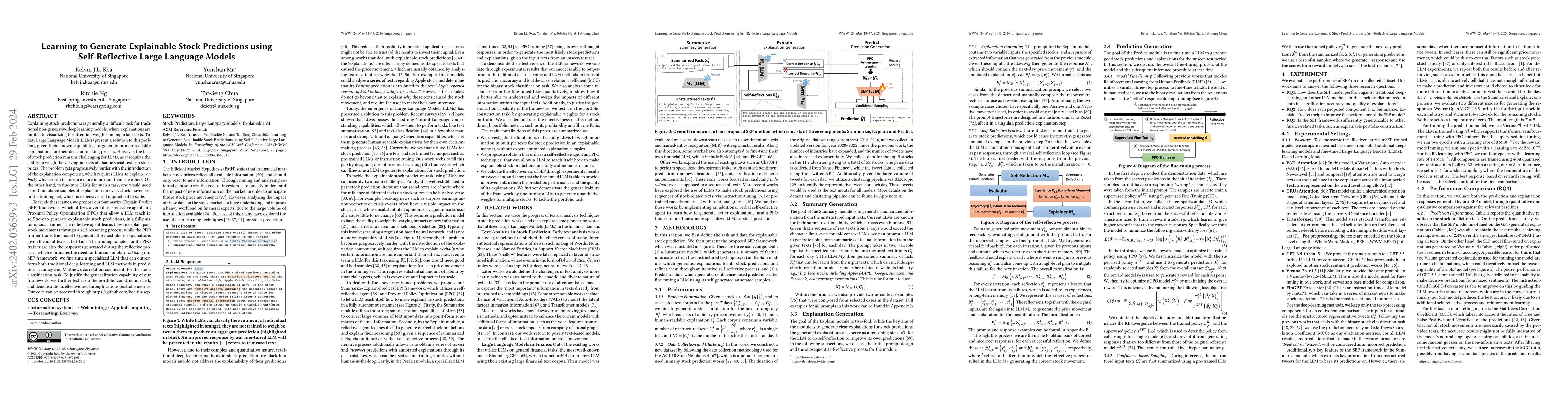

Explaining stock predictions is generally a difficult task for traditional non-generative deep learning models, where explanations are limited to visualizing the attention weights on important texts...

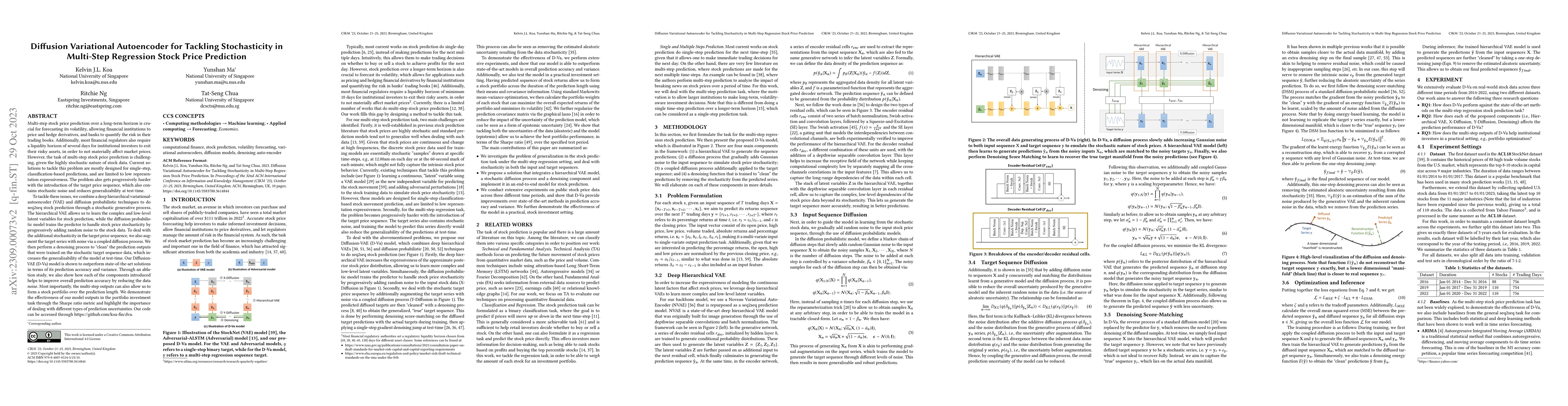

Multi-step stock price prediction over a long-term horizon is crucial for forecasting its volatility, allowing financial institutions to price and hedge derivatives, and banks to quantify the risk i...

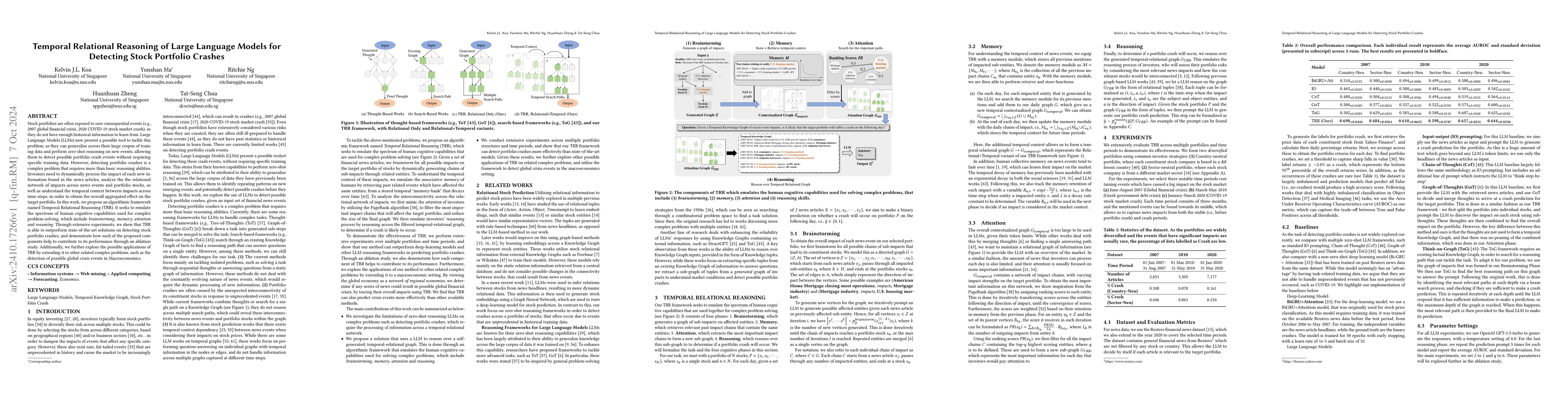

Stock portfolios are often exposed to rare consequential events (e.g., 2007 global financial crisis, 2020 COVID-19 stock market crash), as they do not have enough historical information to learn from....

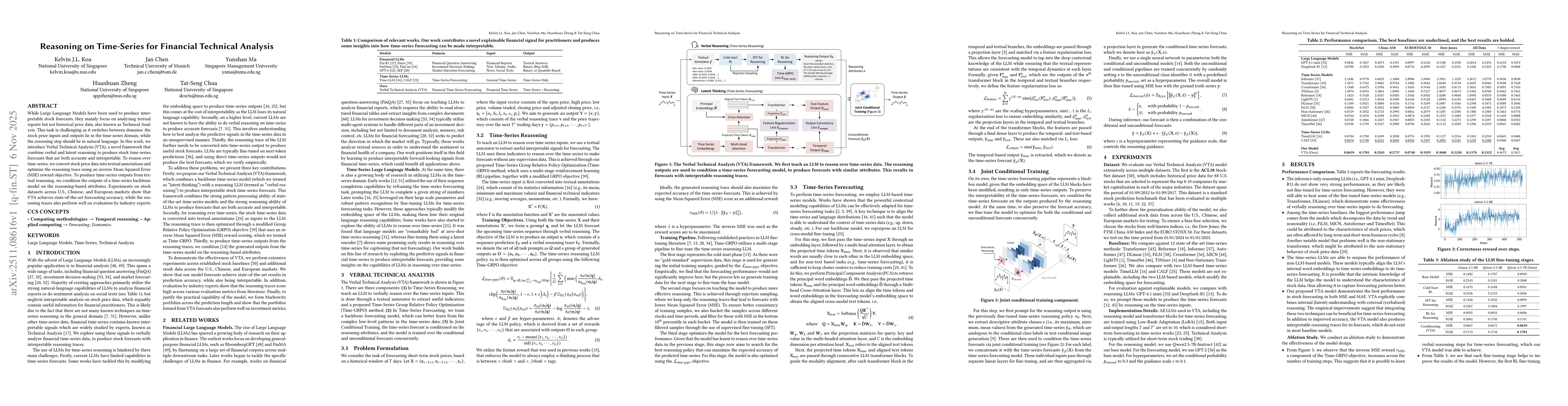

While Large Language Models have been used to produce interpretable stock forecasts, they mainly focus on analyzing textual reports but not historical price data, also known as Technical Analysis. Thi...

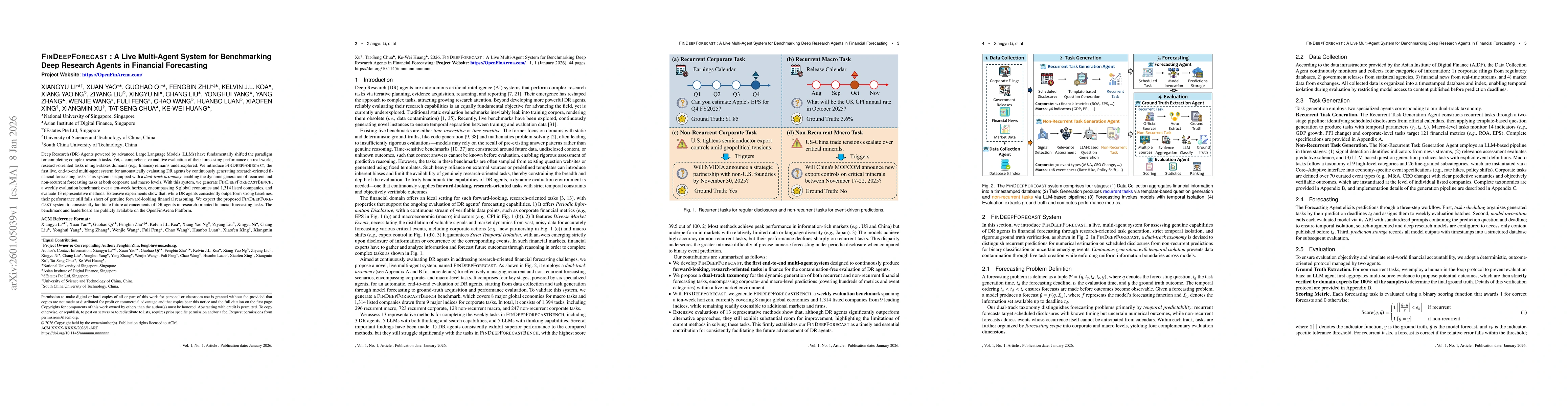

Deep Research (DR) Agents powered by advanced Large Language Models (LLMs) have fundamentally shifted the paradigm for completing complex research tasks. Yet, a comprehensive and live evaluation of th...

Natural Language Processing is rapidly evolving into a primary instrument for Computational Social Science, with researchers increasingly using embeddings to measure latent constructs such as novelty,...

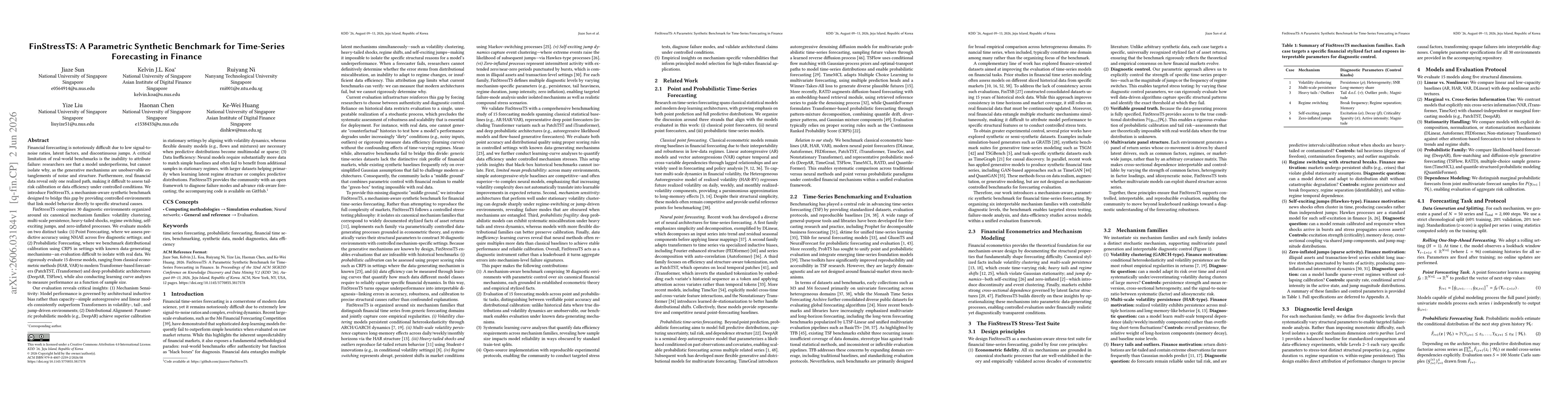

Financial forecasting is difficult due to low signal-to-noise ratios, latent factors, heavy tails, regime shifts, and jumps. Real-world benchmarks offer limited failure attribution: researchers can ob...