Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper explores the impact of stochastic mortality and disease on animal-based commodities, with a specific emphasis on aquaculture, particularly in the context of salmon farming. The investigat...

We study the effect of stochastic feeding costs on animal-based commodities with particular focus on aquaculture. More specifically, we use soybean futures to infer on the stochastic behaviour of sa...

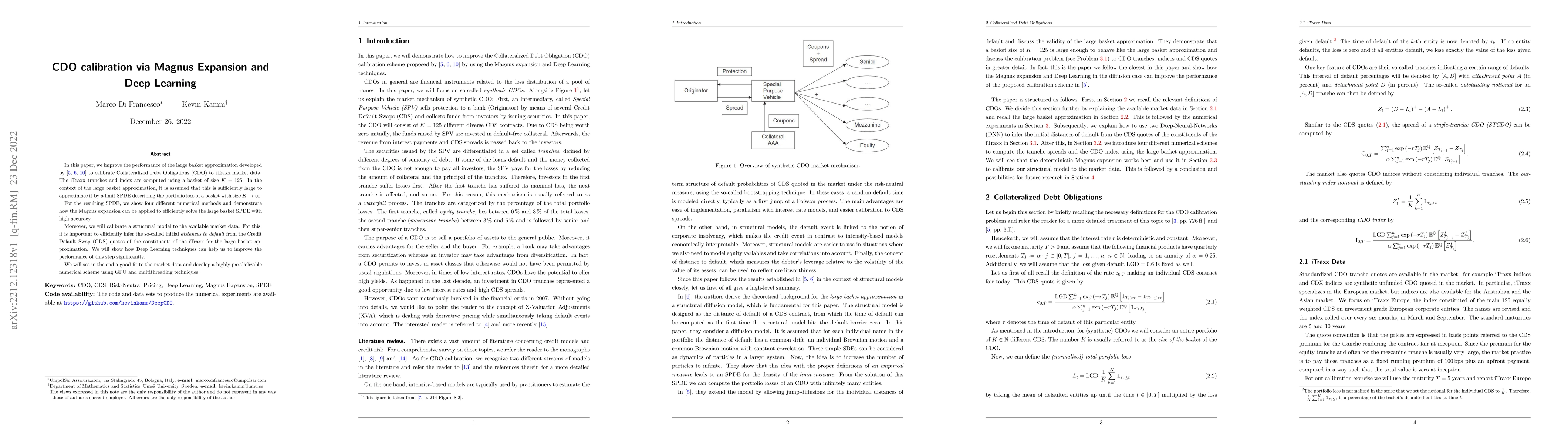

In this paper, we improve the performance of the large basket approximation developed by Reisinger et al. to calibrate Collateralized Debt Obligations (CDO) to iTraxx market data. The iTraxx tranche...

In this paper, we model the rating process of an entity by using a geometrical approach. We model rating transitions as an SDE on a Lie group. Specifically, we focus on calibrating the model to both...

In this paper, we show how the It\^o-stochastic Magnus expansion can be used to efficiently solve stochastic partial differential equations (SPDE) with two space variables numerically. To this end, ...

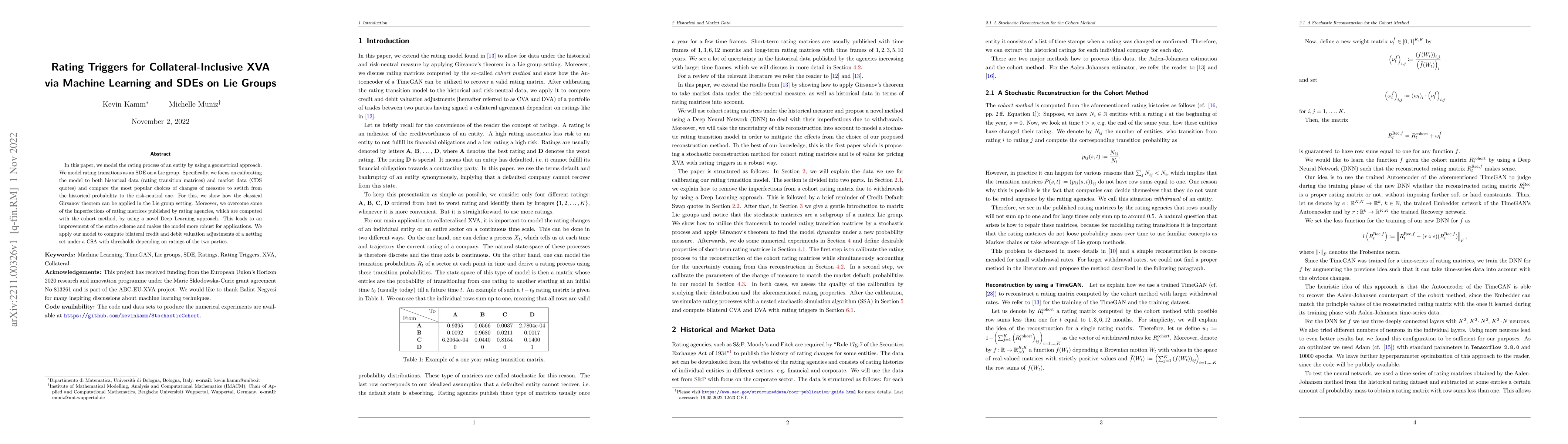

In this paper, we model the rating process of an entity as a piecewise homogeneous continuous time Markov chain. We focus specifically on calibrating the model to both historical data (rating transi...

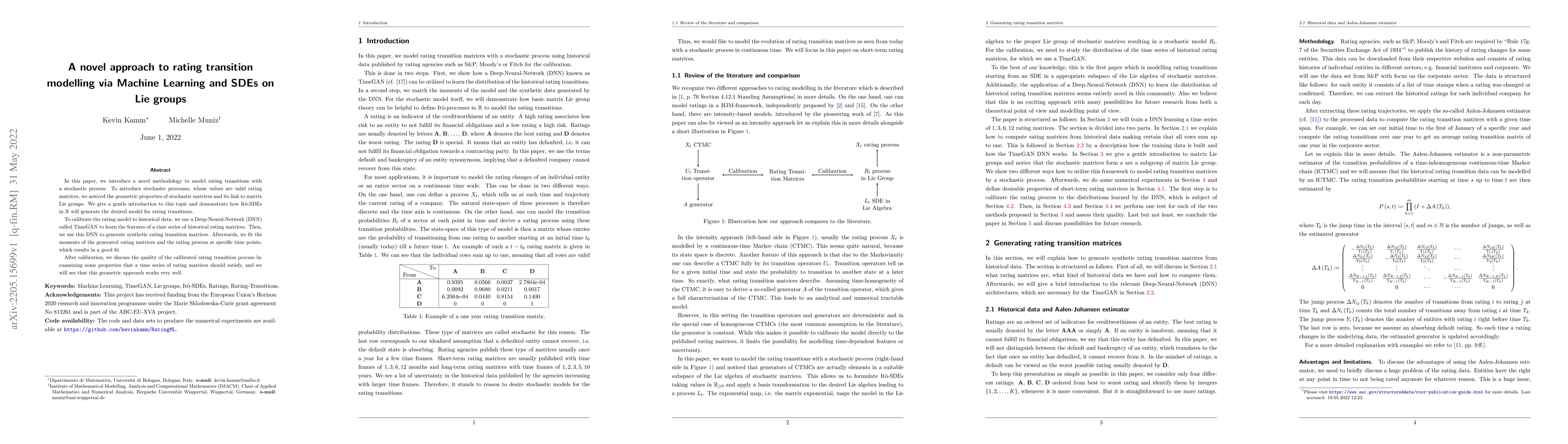

In this paper, we introduce a novel methodology to model rating transitions with a stochastic process. To introduce stochastic processes, whose values are valid rating matrices, we noticed the geome...

In this paper, we propose a new exogenous model to address the problem of negative interest rates that preserves the analytical tractability of the original Cox-Ingersoll-Ross (CIR) model with a per...

In this paper, we propose a new model to address the problem of negative interest rates that preserves the analytical tractability of the original Cox-Ingersoll-Ross (CIR) model without introducing ...

We derive the stochastic version of the Magnus expansion for linear systems of stochastic differential equations (SDEs). The main novelty with respect to the related literature is that we consider S...

This paper studies a joint stochastic optimal control and stopping (JCtrlOS) problem motivated by aquaculture operations, where the objective is to maximize farm profit through an optimal feeding stra...