Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop a framework for composite likelihood inference of parametric continuous-time stationary Gaussian processes. We derive the asymptotic theory of the associated maximum composite likelihood ...

The ability to accurately infer cardiac electrophysiological (EP) properties is key to improving arrhythmia diagnosis and treatment. In this work, we developed a physics-informed neural networks (PI...

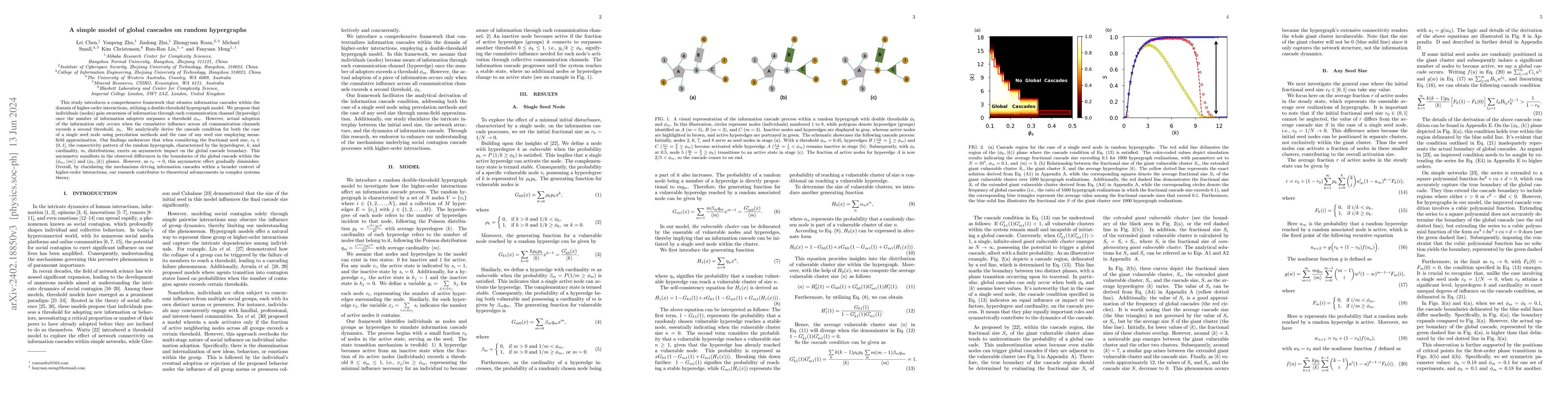

This study introduces a comprehensive framework that situates information cascades within the domain of higher-order interactions, utilizing a double-threshold hypergraph model. We propose that indi...

The Chinese venture capital (VC) market is a young and rapidly expanding financial subsector. Gaining a deeper understanding of the investment behaviours of VC firms is crucial for the development o...

The frequency and magnitude of weather extreme events have increased significantly during the past few years in response to anthropogenic climate change. However, global statistical characteristics ...

Community structures have been identified in various complex real-world networks, for example, communication, information, internet and shareholder networks. The scaling of community size distributi...

In this paper, we develop a penalized realized variance (PRV) estimator of the quadratic variation (QV) of a high-dimensional continuous It\^{o} semimartingale. We adapt the principle idea of regula...

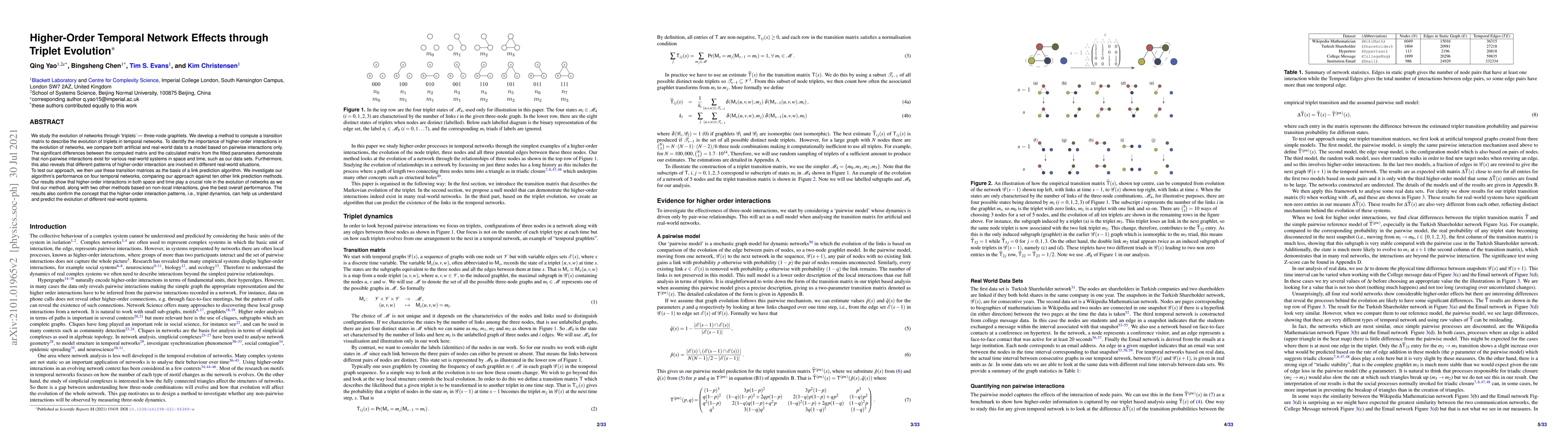

We study the evolution of networks through `triplets' - three-node graphlets. We develop a method to compute a transition matrix to describe the evolution of triplets in temporal networks. To identi...

We develop a GMM approach for estimation of log-normal stochastic volatility models driven by a fractional Brownian motion with unrestricted Hurst exponent. We show that a parameter estimator based ...

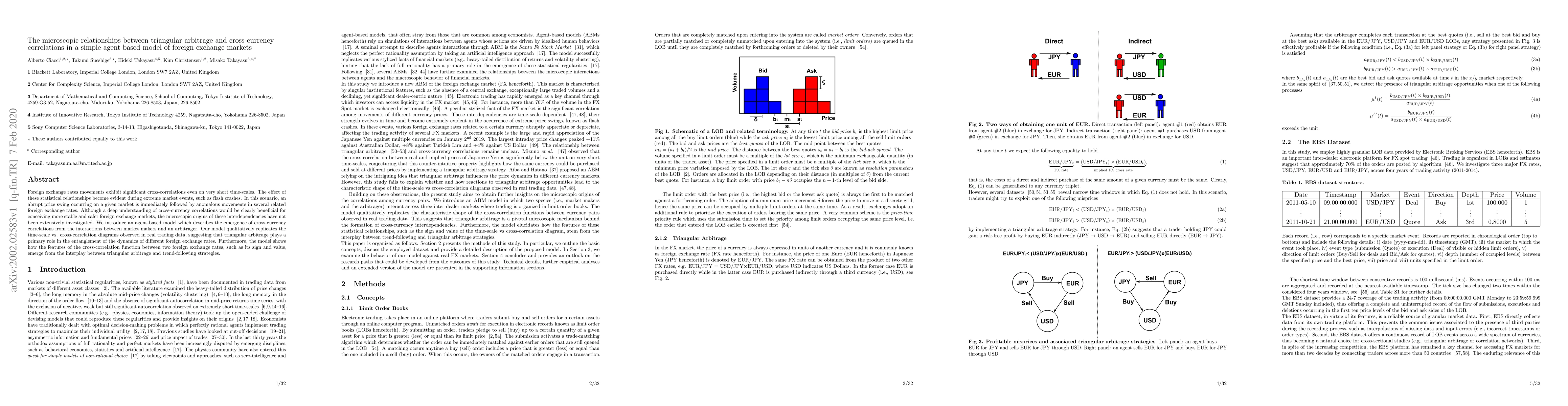

Foreign exchange rates movements exhibit significant cross-correlations even on very short time-scales. The effect of these statistical relationships become evident during extreme market events, suc...

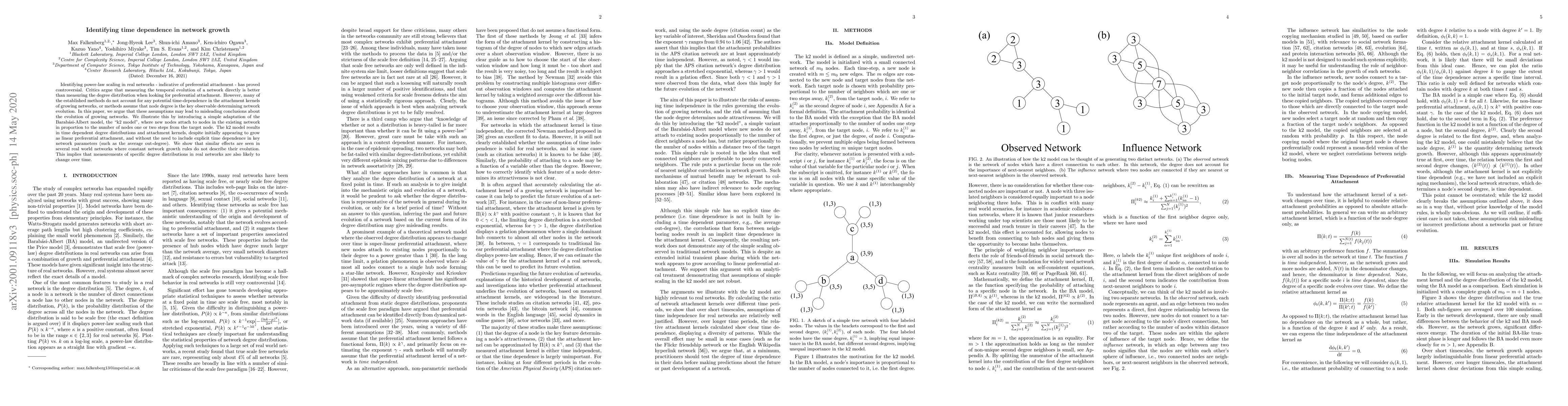

Identifying power-law scaling in real networks - indicative of preferential attachment - has proved controversial. Critics argue that measuring the temporal evolution of a network directly is better...

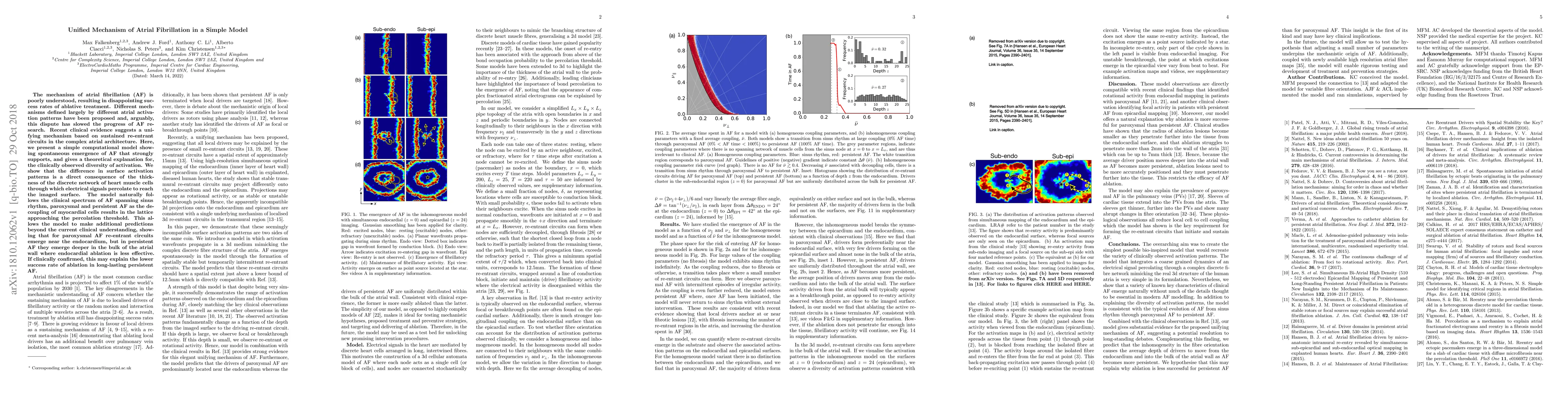

The mechanism of atrial fibrillation (AF) is poorly understood, resulting in disappointing success rates of ablative treatment. Different mechanisms defined largely by different atrial activation pa...

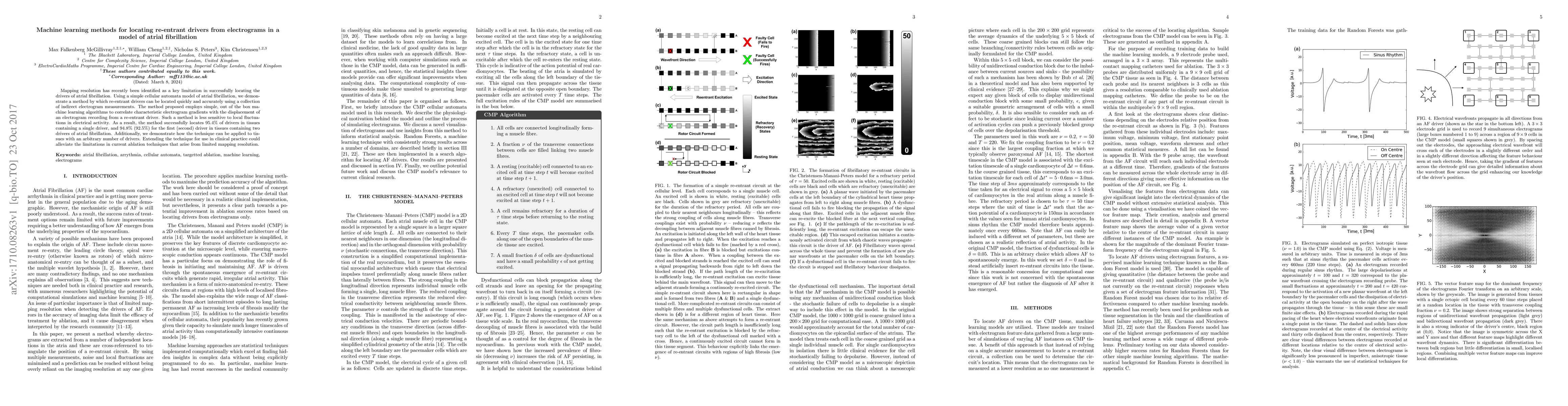

Mapping resolution has recently been identified as a key limitation in successfully locating the drivers of atrial fibrillation. Using a simple cellular automata model of atrial fibrillation, we dem...

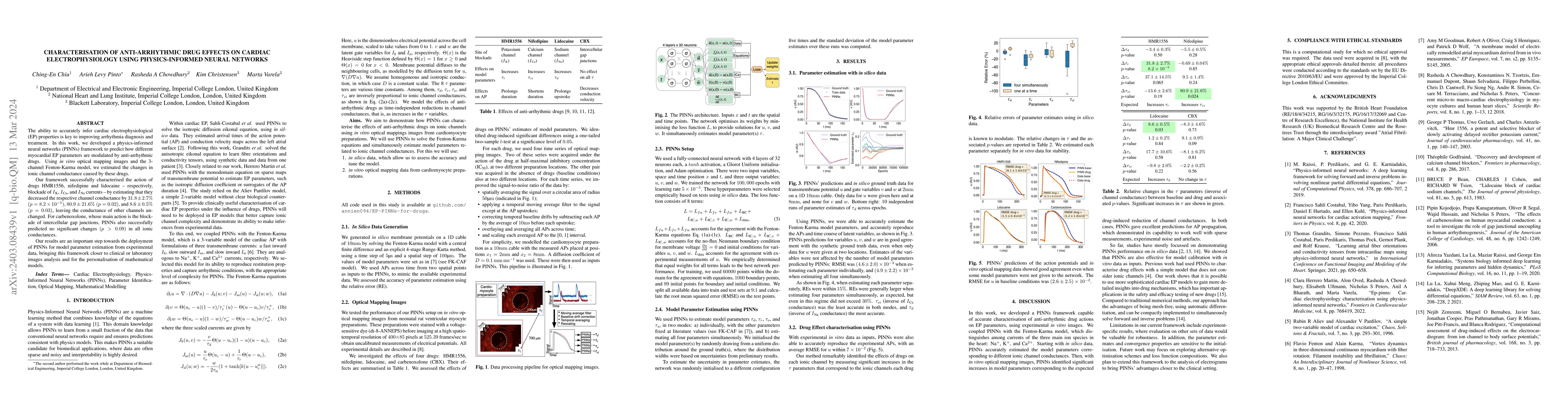

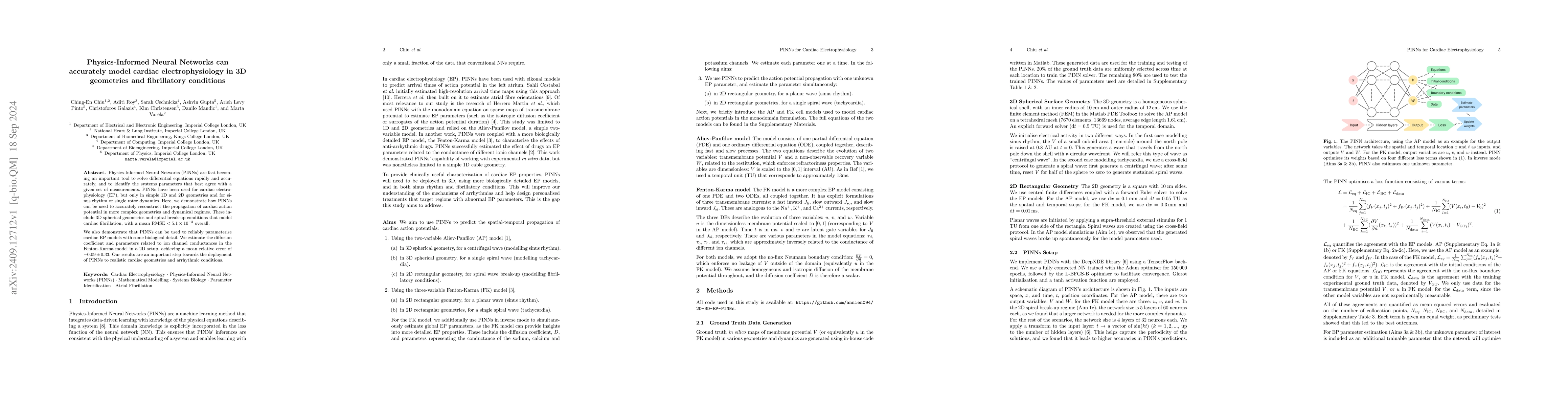

Physics-Informed Neural Networks (PINNs) are fast becoming an important tool to solve differential equations rapidly and accurately, and to identify the systems parameters that best agree with a given...

We develop a model for point processes on the real line, where the intensity can be locally unbounded without inducing an explosion. In contrast to an orderly point process, for which the probability ...

The association between log-price increments of exchange-traded equities, as measured by their spot correlation estimated from high-frequency data, exhibits a pronounced upward-sloping and almost piec...

We introduce a minimalistic model based on dynamic node deletion and node duplication with heterodimerisation. The model is intended to capture the essential features of the evolution of protein inter...

Atmospheric rivers (ARs) are essential components of the global hydrological cycle, with profound implications for water resources, extreme weather events, and climate dynamics. Yet, the statistical o...

We introduce a minimalistic model based on dynamic node deletion and node duplication with heterodimerisation. The model is intended to capture the essential features of the evolution of protein inter...

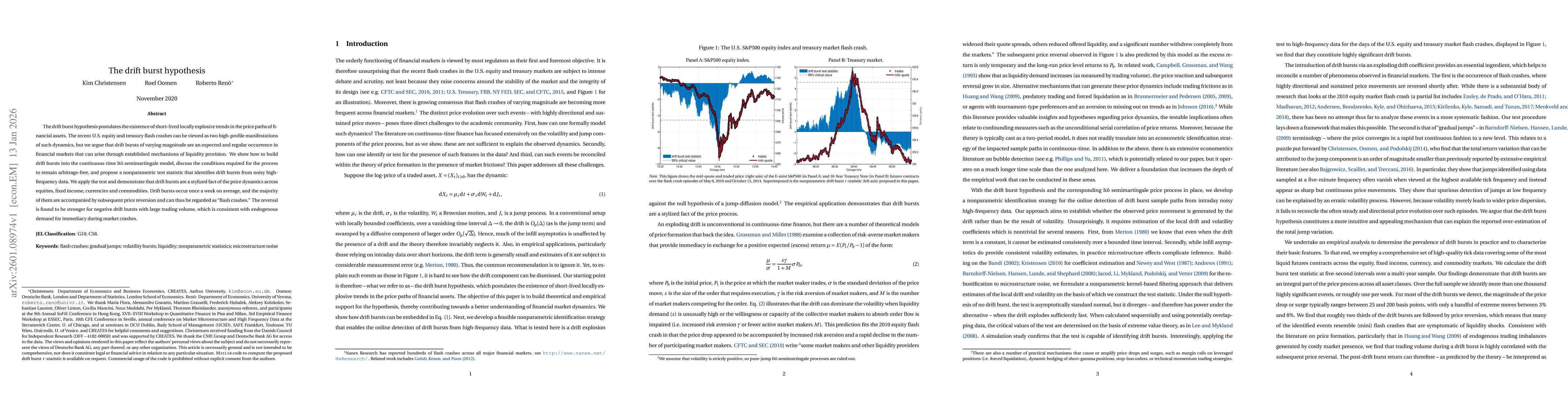

The drift burst hypothesis postulates the existence of short-lived locally explosive trends in the price paths of financial assets. The recent U.S. equity and treasury flash crashes can be viewed as t...

Corporate earnings announcements unpack large bundles of public information that should, in efficient markets, trigger jumps in stock prices. Testing this implication is difficult in practice, as it r...

We inspect how accurate machine learning (ML) is at forecasting realized variance of the Dow Jones Industrial Average index constituents. We compare several ML algorithms, including regularization, re...

In this paper, we propose a new jump robust quantile-based realised variance measure of ex-post return variation that can be computed using potentially noisy data. The estimator is consistent for the ...

In this paper, we show how to estimate the asymptotic (conditional) covariance matrix, which appears in central limit theorems in high-frequency estimation of asset return volatility. We provide a rec...

In this paper, we propose a nonparametric way to test the hypothesis that time-variation in intraday volatility is caused solely by a deterministic and recurrent diurnal pattern. We assume that noisy ...

We propose a nonparametric estimator of the empirical distribution function (EDF) of the latent spot variance of the log-price of a financial asset. We show that over a fixed time span our realized ED...

We provide a set of probabilistic laws for estimating the quadratic variation of continuous semimartingales with realized range-based variance -- a statistic that replaces every squared return of real...

We study the trading activity of designated market makers (DMMs) in electronic markets using a unique dataset with audit-trail information on trader classification. DMMs may either adhere to their mar...

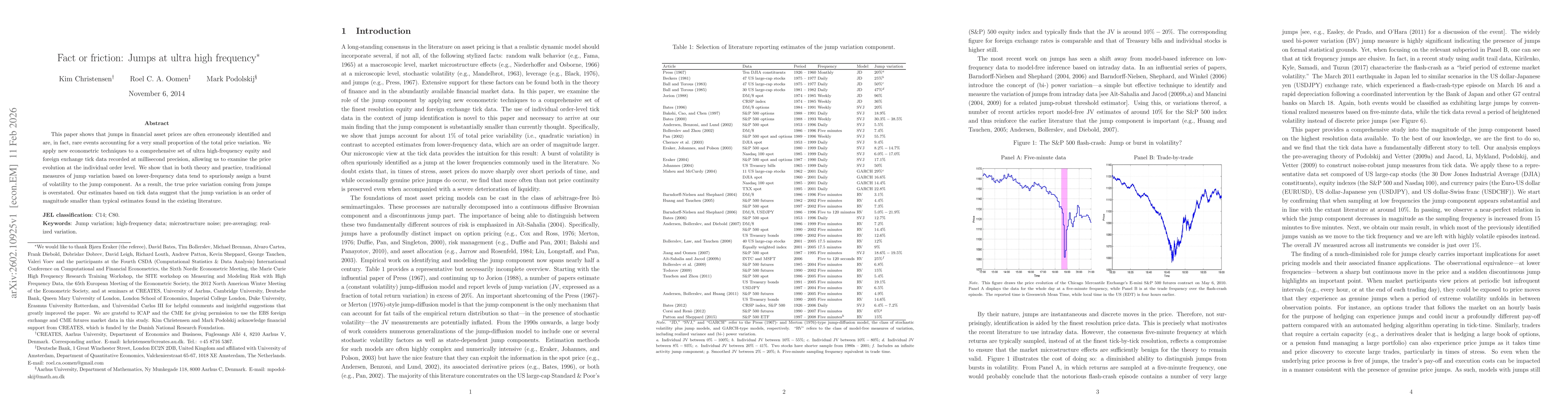

This paper shows that jumps in financial asset prices are often erroneously identified and are, in fact, rare events accounting for a very small proportion of the total price variation. We apply new e...

In this paper, we present a realized range-based multipower variation theory, which can be used to estimate return variation and draw jump-robust inference about the diffusive volatility component, wh...

This paper presents a Hayashi-Yoshida type estimator for the covariation matrix of continuous Itô semimartingales observed with noise. The coordinates of the multivariate process are assumed to be obs...

We show how pre-averaging can be applied to the problem of measuring the ex-post covariance of financial asset returns under microstructure noise and non-synchronous trading. A pre-averaged realised c...

We study a new measure of codependency in the second moment of a continuous-time multivariate asset price process, which we name the realized copula of volatility. The statistic is based on local vola...