Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a new model which can be considered as a extended version of the Hawkes process in a discrete sense. This model enables the integration of various residual distributions while preservin...

This study examines the use of a recurrent neural network for estimating the parameters of a Hawkes model based on high-frequency financial data, and subsequently, for computing volatility. Neural n...

This study investigates and uses multi-kernel Hawkes models to describe a high-frequency mid-price process. Each kernel represents a different responsive speed of market participants. Using the cond...

The Hawkes model is suitable for describing self and mutually exciting random events. In addition, the exponential decay in the Hawkes process allows us to calculate the moment properties in the mod...

This study proposes a versatile model for the dynamics of the best bid and ask prices using an extended Hawkes process. The model incorporates the zero intensities of the spread-narrowing processes ...

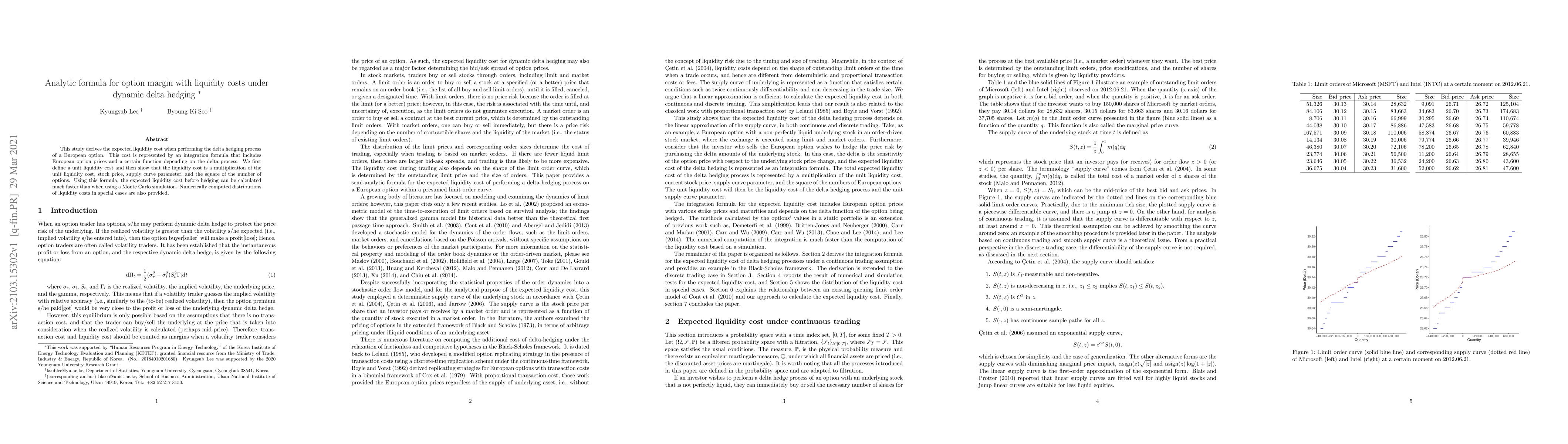

This study derives the expected liquidity cost when performing the delta hedging process of a European option. This cost is represented by an integration formula that includes European option prices...

We propose the Hawkes flocking model that assesses systemic risk in high-frequency processes at the two perspectives -- endogeneity and interactivity. We examine the futures markets of WTI crude oil...

The risk-neutral option pricing method under GARCH intensity model is examined. The GARCH intensity model incorporates the characteristics of financial return series such as volatility clustering, l...

The third moment variation of a financial asset return process is defined by the quadratic covariation between the return and square return processes. The skew and fat tail risk of an underlying ass...

This study examine the theoretical and empirical perspectives of the symmetric Hawkes model of the price tick structure. Combined with the maximum likelihood estimation, the model provides a proper ...

In quantitative finance, it is often necessary to analyze the distribution of the sum of specific functions of observed values at discrete points of an underlying process. Examples include the proba...

A simple Hawkes model have been developed for the price tick structure dynamics incorporating market microstructure noise and trade clustering. In this paper, the model is extended with random mark ...

This study explores the prediction of high-frequency price changes using deep learning models. Although state-of-the-art methods perform well, their complexity impedes the understanding of successful ...

This paper presents a method for forecasting limit order book durations using a self-exciting flexible residual point process. High-frequency events in modern exchanges exhibit heavy-tailed interarriv...