Academic Profile

Statistics

Similar Authors

Papers on arXiv

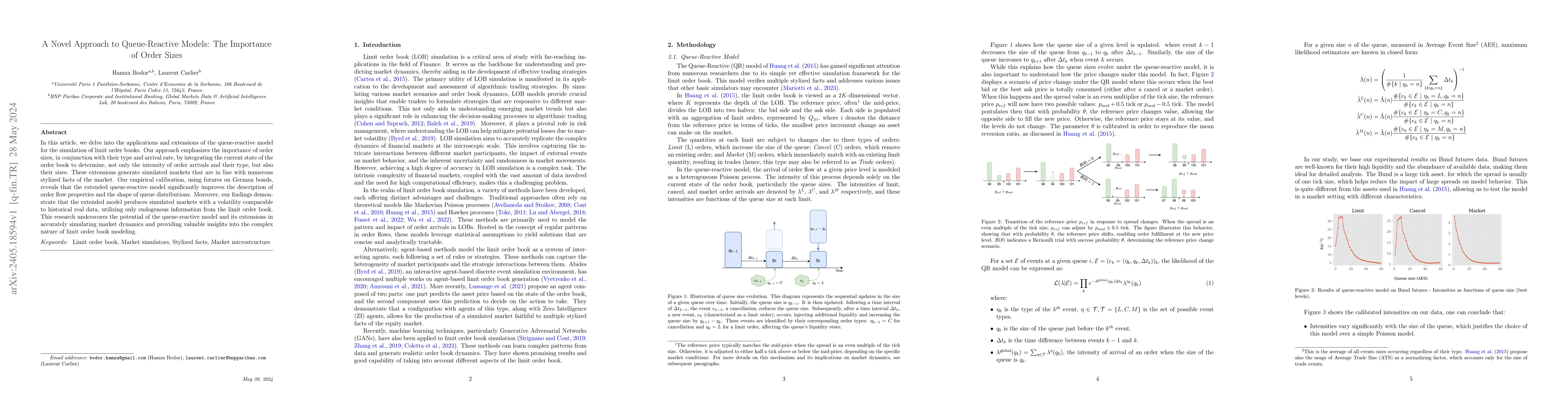

In this article, we delve into the applications and extensions of the queue-reactive model for the simulation of limit order books. Our approach emphasizes the importance of order sizes, in conjunct...

This paper presents an in-depth analysis of stylized facts in the context of futures on German bonds. The study examines four futures contracts on German bonds: Schatz, Bobl, Bund and Buxl, using ti...

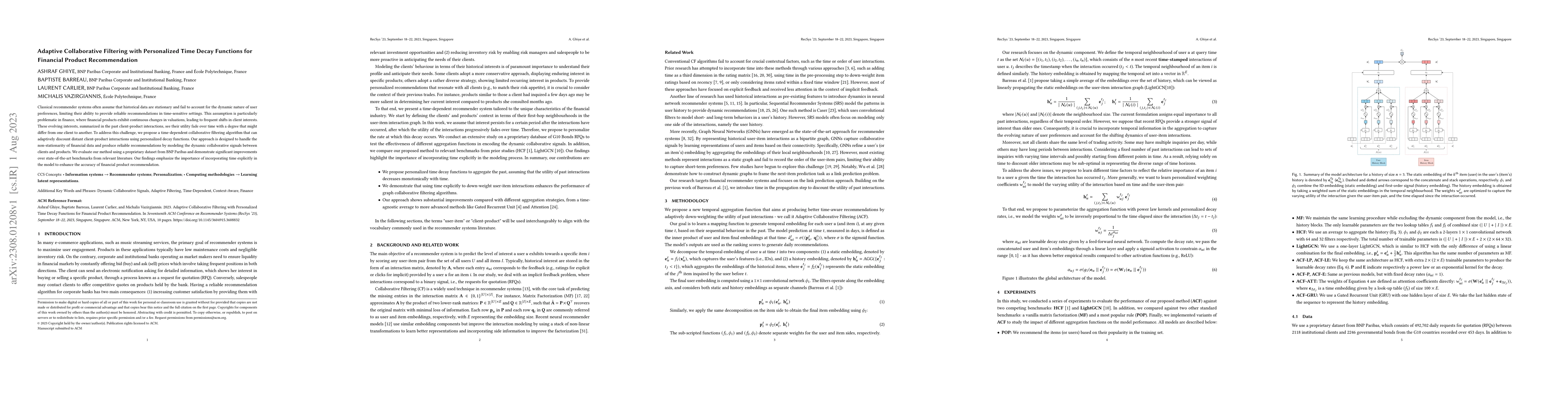

Classical recommender systems often assume that historical data are stationary and fail to account for the dynamic nature of user preferences, limiting their ability to provide reliable recommendati...

As of 2022, greenhouse gases (GHG) emissions reporting and auditing are not yet compulsory for all companies and methodologies of measurement and estimation are not unified. We propose a machine lea...

We systematically investigate the links between price returns and Environment, Social and Governance (ESG) scores in the European equity market. Using interpretable machine learning, we examine whet...

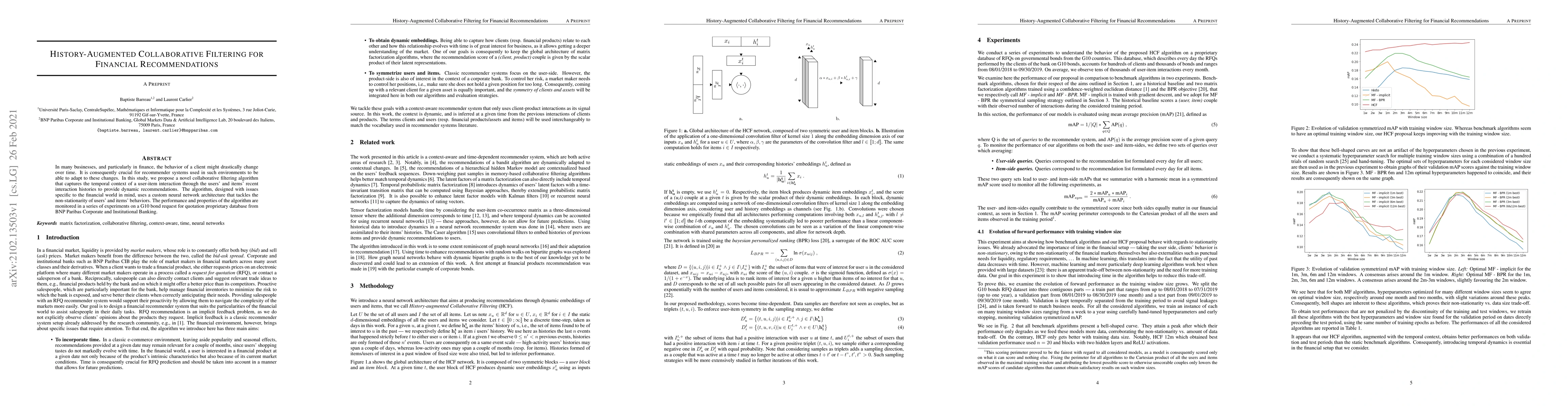

In many businesses, and particularly in finance, the behavior of a client might drastically change over time. It is consequently crucial for recommender systems used in such environments to be able ...

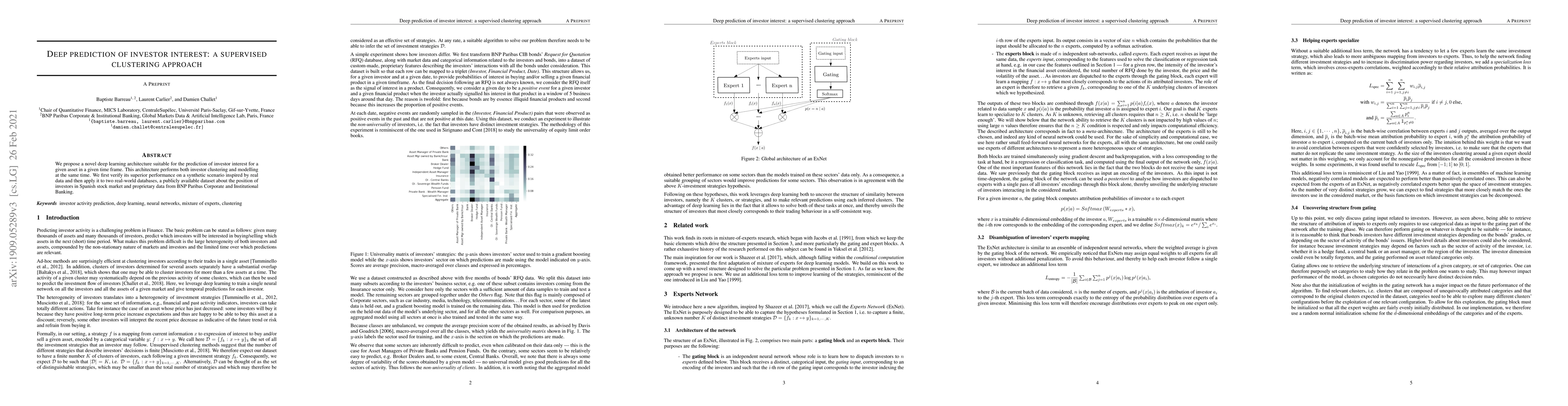

We propose a novel deep learning architecture suitable for the prediction of investor interest for a given asset in a given time frame. This architecture performs both investor clustering and modell...

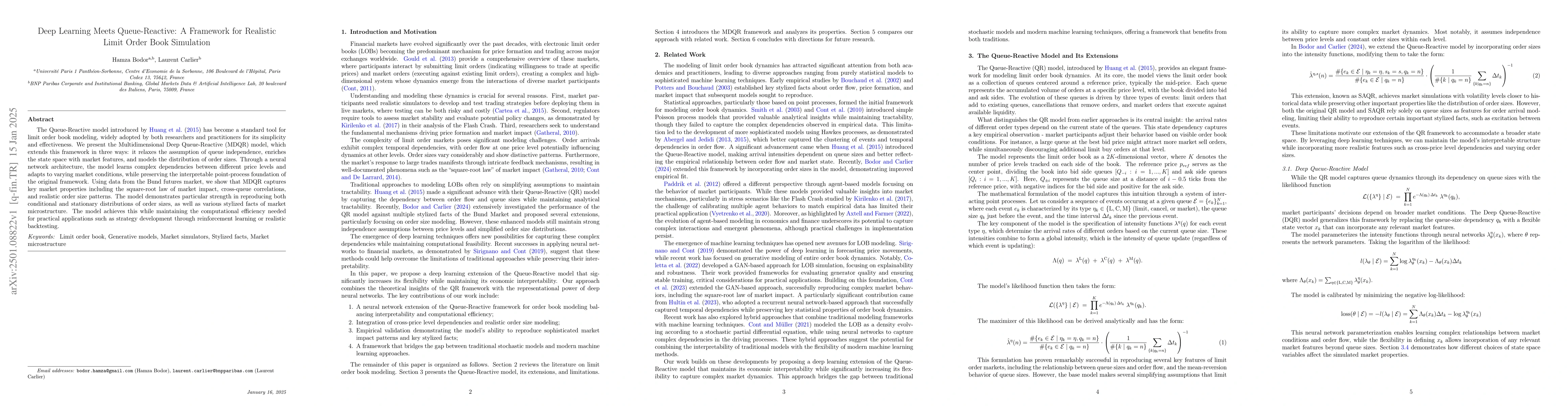

The Queue-Reactive model introduced by Huang et al. (2015) has become a standard tool for limit order book modeling, widely adopted by both researchers and practitioners for its simplicity and effecti...

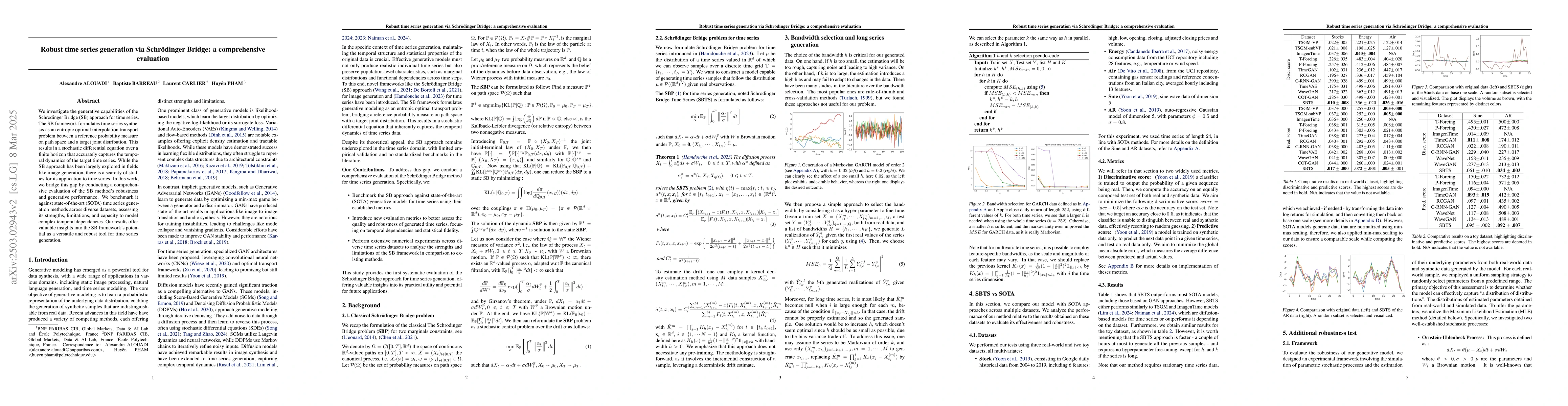

We investigate the generative capabilities of the Schr\"odinger Bridge (SB) approach for time series. The SB framework formulates time series synthesis as an entropic optimal interpolation transport p...

Graph Neural Networks have significantly advanced research in recommender systems over the past few years. These methods typically capture global interests using aggregated past interactions and rely ...