Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a very efficient method for pricing various types of lookback options under Markov models. We utilize the model-free representations of lookback option prices as integrals of first passag...

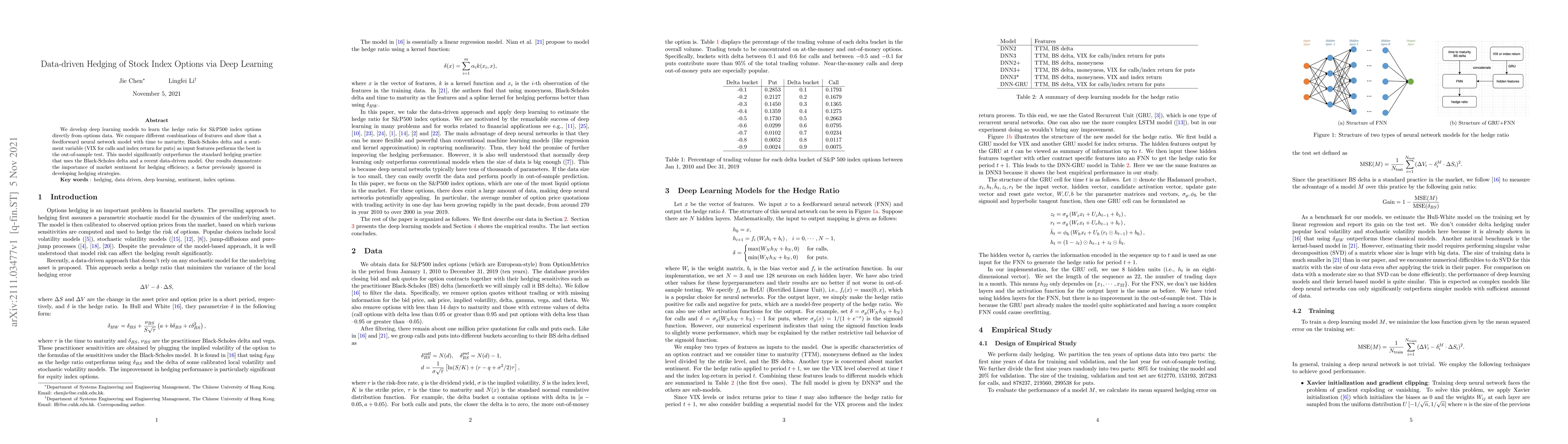

We develop deep learning models to learn the hedge ratio for S&P500 index options directly from options data. We compare different combinations of features and show that a feedforward neural network...

We propose a method based on continuous time Markov chain approximation to compute the distribution of Parisian stopping times and price Parisian options under general one-dimensional Markov process...

We develop a new simulation method for multidimensional diffusions with sticky boundaries. The challenge comes from simulating the sticky boundary behavior, for which standard methods like the Euler...

We propose a two-step framework for predicting the implied volatility surface over time without static arbitrage. In the first step, we select features to represent the surface and predict them over...

Semiconducting nanowires offer many opportunities for electronic and optoelectronic device applications due to their special geometries and unique physical properties. However, it has been challengi...

We develop continuous time Markov chain (CTMC) approximation of one-dimensional diffusions with a lower sticky boundary. Approximate solutions to the action of the Feynman-Kac operator associated wi...