Academic Profile

Statistics

Papers on arXiv

In a dual risk model, the premiums are considered as the costs and the claims are regarded as the profits. The surplus can be interpreted as the wealth of a venture capital, whose profits depend on ...

Dual risk models are popular for modeling a venture capital or high tech company, for which the running cost is deterministic and the profits arrive stochastically over time. Most of the existing li...

The dual risk model is a popular model in finance and insurance, which is often used to model the wealth process of a venture capital or high tech company. Optimal dividends have been extensively st...

We develop approximate estimation methods for exponential random graph models (ERGMs), whose likelihood is proportional to an intractable normalizing constant. The usual approach approximates this c...

Hawkes process is a class of simple point processes with self-exciting and clustering properties. Hawkes process has been widely applied in finance, neuroscience, social networks, criminology, seism...

Injecting heavy-tailed noise to the iterates of stochastic gradient descent (SGD) has received increasing attention over the past few years. While various theoretical properties of the resulting alg...

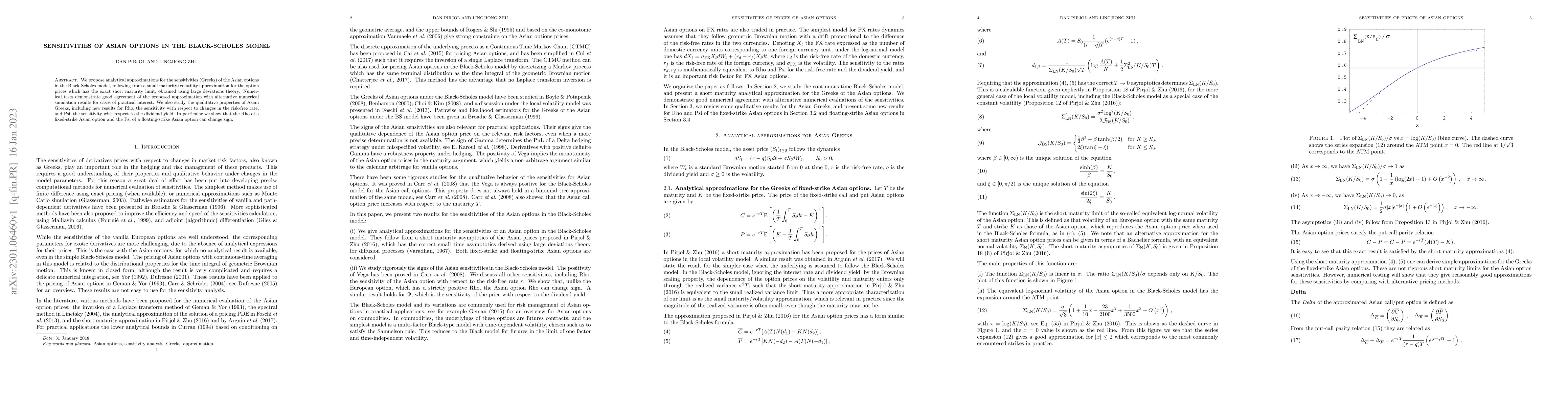

We derive the short-maturity asymptotics for option prices in the local volatility model in a new short-maturity limit $T\to 0$ at fixed $\rho = (r-q) T$, where $r$ is the interest rate and $q$ is t...

We study Euler-Maruyama numerical schemes of stochastic differential equations driven by stable L\'{e}vy processes with i.i.d. stable components. We obtain a uniform-in-time approximation error in W...

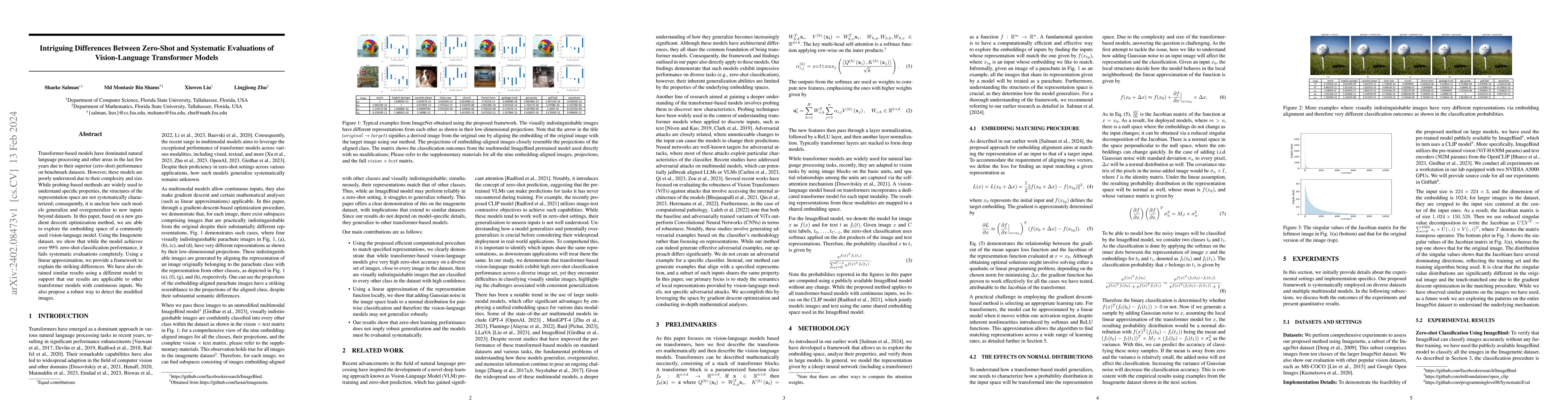

Transformer-based models have dominated natural language processing and other areas in the last few years due to their superior (zero-shot) performance on benchmark datasets. However, these models a...

Score-based generative modeling with probability flow ordinary differential equations (ODEs) has achieved remarkable success in a variety of applications. While various fast ODE-based samplers have ...

Score-based generative models (SGMs) is a recent class of deep generative models with state-of-the-art performance in many applications. In this paper, we establish convergence guarantees for a gene...

We present a study of the short maturity asymptotics for Asian options in a jump-diffusion model with a local volatility component, where the jumps are modeled as a compound Poisson process. The ana...

The Hawkes process is a counting process that has self- and mutually-exciting features with many applications in various fields. In recent years, there have been many interests in the mean-field res...

We present an asymptotic result for the Laplace transform of the time integral of the geometric Brownian motion $F(\theta,T) = \mathbb{E}[e^{-\theta X_T}]$ with $X_T = \int_0^T e^{\sigma W_s + ( a -...

Algorithmic stability is an important notion that has proven powerful for deriving generalization bounds for practical algorithms. The last decade has witnessed an increasing number of stability bou...

Cyclic and randomized stepsizes are widely used in the deep learning practice and can often outperform standard stepsize choices such as constant stepsize in SGD. Despite their empirical success, no...

Heavy-tail phenomena in stochastic gradient descent (SGD) have been reported in several empirical studies. Experimental evidence in previous works suggests a strong interplay between the heaviness o...

Hawkes processes are a class of simple point processes whose intensity depends on the past history, and is in general non-Markovian. Limit theorems for Hawkes processes in various asymptotic regimes...

We propose analytical approximations for the sensitivities (Greeks) of the Asian options in the Black-Scholes model, following from a small maturity/volatility approximation for the option prices wh...

In this paper, we study a dual risk model with delays in the spirit of Dassios-Zhao. When a new innovation occurs, there is a delay before the innovation turns into a profit. We obtain large initial...

We consider the constrained sampling problem where the goal is to sample from a target distribution $\pi(x)\propto e^{-f(x)}$ when $x$ is constrained to lie on a convex body $\mathcal{C}$. Motivated...

Recent studies have shown that heavy tails can emerge in stochastic optimization and that the heaviness of the tails have links to the generalization error. While these studies have shed light on in...

Recent theoretical studies have shown that heavy-tails can emerge in stochastic optimization due to `multiplicative noise', even under surprisingly simple settings, such as linear regression with Ga...

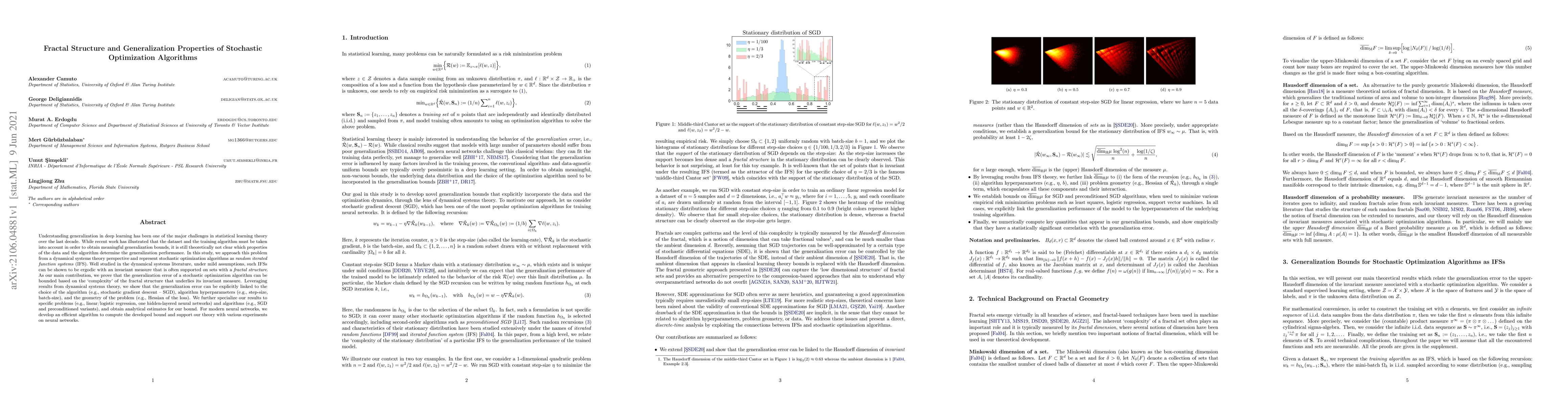

Understanding generalization in deep learning has been one of the major challenges in statistical learning theory over the last decade. While recent work has illustrated that the dataset and the tra...

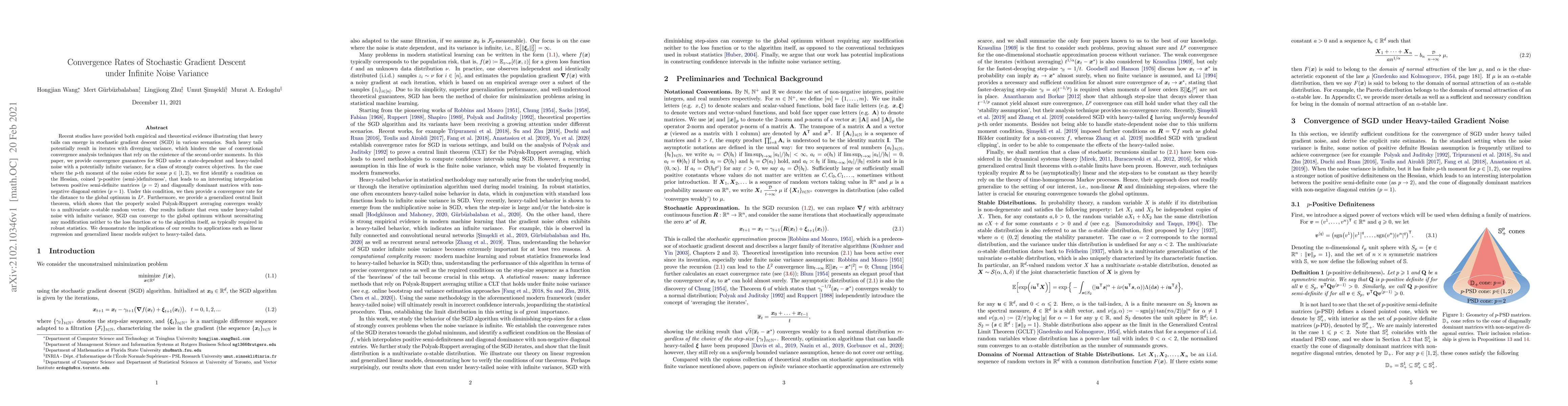

Recent studies have provided both empirical and theoretical evidence illustrating that heavy tails can emerge in stochastic gradient descent (SGD) in various scenarios. Such heavy tails potentially ...

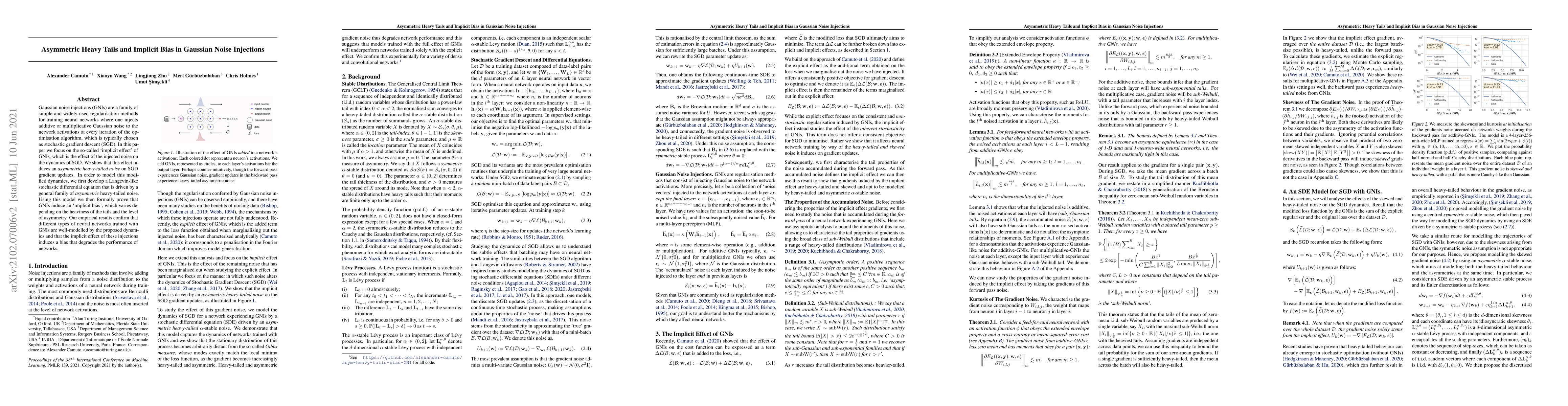

Gaussian noise injections (GNIs) are a family of simple and widely-used regularisation methods for training neural networks, where one injects additive or multiplicative Gaussian noise to the networ...

In recent years, various notions of capacity and complexity have been proposed for characterizing the generalization properties of stochastic gradient descent (SGD) in deep learning. Some of the pop...

We study the explosion of the solutions of the SDE in the quasi-Gaussian HJM model with a CEV-type volatility. The quasi-Gaussian HJM models are a popular approach for modeling the dynamics of the y...

Quasi-Gaussian HJM models are a popular approach for modeling the dynamics of the yield curve. This is due to their low dimensional Markovian representation, which greatly simplifies their numerical...

Affine point processes are a class of simple point processes with self- and mutually-exciting properties, and they have found useful applications in several areas. In this paper, we obtain large-tim...

We consider estimating an expected infinite-horizon cumulative discounted cost/reward contingent on an underlying stochastic process by Monte Carlo simulation. An unbiased estimator based on truncat...

We study the short maturity asymptotics for prices of forward start Asian options under the assumption that the underlying asset follows a local volatility model. We obtain asymptotics for the cases...

Langevin algorithms are popular Markov Chain Monte Carlo methods for Bayesian learning, particularly when the aim is to sample from the posterior distribution of a parametric model, given the input da...

We derive the short-maturity asymptotics for prices of options on realized variance in local-stochastic volatility models. We consider separately the short-maturity asymptotics for out-of-the-money an...

We derive the short-maturity asymptotics for Asian option prices in local-stochastic volatility (LSV) models. Both out-of-the-money (OTM) and at-the-money (ATM) asymptotics are considered. Using large...

We derive the short-maturity asymptotics for European and VIX option prices in local-stochastic volatility models where the volatility follows a continuous-path Markov process. Both out-of-the-money (...

We study the pricing of VIX options in the SABR model $dS_t = \sigma_t S_t^\beta dB_t, d\sigma_t = \omega \sigma_t dZ_t$ where $B_t,Z_t$ are standard Brownian motions correlated with correlation $\rho...

We consider the constrained sampling problem where the goal is to sample from a target distribution on a constrained domain. We propose skew-reflected non-reversible Langevin dynamics (SRNLD), a conti...

Understanding the generalization properties of optimization algorithms under heavy-tailed noise has gained growing attention. However, the existing theoretical results mainly focus on stochastic gradi...

Self-supervised learning has been a powerful approach for learning meaningful representations from unlabeled data across various domains, reducing the reliance on large labeled datasets. Inspired by B...

Langevin algorithms are popular Markov chain Monte Carlo methods that are often used to solve high-dimensional large-scale sampling problems in machine learning. The most classical Langevin Monte Carl...

The problem of sampling a target probability distribution on a constrained domain arises in many applications including machine learning. For constrained sampling, various Langevin algorithms such as ...

We study the optimal sequencing of a batch of tasks on a machine subject to random disruptions driven by a non-homogeneous Poisson process (NHPP), such that every disruption requires the interrupted t...

Langevin Monte Carlo (LMC) algorithms are popular Markov Chain Monte Carlo (MCMC) methods to sample a target probability distribution, which arises in many applications in machine learning. Inspired b...

Langevin algorithms are popular Markov chain Monte Carlo (MCMC) methods for large-scale sampling problems that often arise in data science. We propose Monte Carlo algorithms based on the discretizatio...

Standard first-order Langevin algorithms such as the unadjusted Langevin algorithm (ULA) are obtained by discretizing the Langevin diffusion and are widely used for sampling in machine learning becaus...

Sampling from a target distribution induced by training data is central to Bayesian learning, with Stochastic Gradient Langevin Dynamics (SGLD) serving as a key tool for scalable posterior sampling an...

Characterizing the differential privacy (DP) of learning algorithms has become a major challenge in recent years. In parallel, many studies suggested investigating the behavior of stochastic gradient ...

Hawkes processes are point processes with self-exciting and clustering properties that are popular in applications. In recent years, renewal Hawkes processes have gained attention, due to their versat...

We study the problem of sampling from a target distribution $π(q)\propto e^{-U(q)}$ on $\mathbb{R}^d$, where $U$ can be non-convex, via the Hessian-free high-resolution (HFHR) dynamics, which is a sec...

We present a study of the short-maturity asymptotics for VIX and European option prices in local-stochastic volatility models with compound Poisson jumps. Both out-of-the-money (OTM) and at-the-money ...

We propose Decentralized Proximal Stochastic Gradient Langevin Dynamics (DE-PSGLD), a decentralized Markov chain Monte Carlo (MCMC) algorithm for sampling from a log-concave probability distribution c...

Diffusion models achieve strong generation quality, diversity, and distribution coverage, but their performance often comes with expensive inference. In this work, we propose Stochastic Transition-Map...

We present a study of the leading-order asymptotics for VIX option prices in Bergomi models in the short-maturity and small volatility-of-volatility regimes. Both out-of-the-money (OTM) and at-the-mon...