Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the problem of choosing the copula when the marginal distributions of a random vector are not all continuous. Inspired by three motivating examples including simulation from copulas, stress...

We analyze the problem of optimally sharing risk using allocations that exhibit counter-monotonicity, the most extreme form of negative dependence. Counter-monotonic allocations take the form of eit...

A useful property of independent samples is that their correlation remains the same after applying marginal transforms. This invariance property plays a fundamental role in statistical inference, bu...

We study optimal reinsurance in the framework of stochastic game theory, in which there is an insurer and two reinsurers. A Stackelberg model is established to analyze the non-cooperative relationsh...

We systematically study pairwise counter-monotonicity, an extremal notion of negative dependence. A stochastic representation and an invariance property are established for this dependence structure...

We address the problem of sharing risk among agents with preferences modelled by a general class of comonotonic additive and law-based functionals that need not be either monotone or convex. Such fu...

The diversification quotient (DQ) is recently introduced for quantifying the degree of diversification of a stochastic portfolio model. It has an axiomatic foundation and can be defined through a pa...

We establish the first axiomatic theory for diversification indices using six intuitive axioms: non-negativity, location invariance, scale invariance, rationality, normalization, and continuity. The...

A joint mix is a random vector with a constant component-wise sum. The dependence structure of a joint mix minimizes some common objectives such as the variance of the component-wise sum, and it is ...

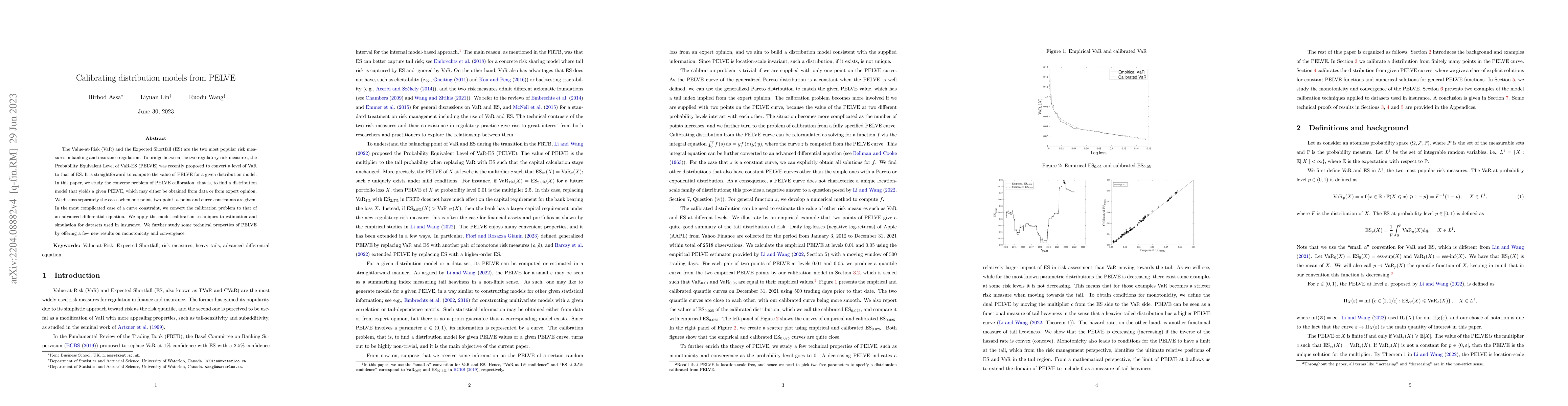

The Value-at-Risk (VaR) and the Expected Shortfall (ES) are the two most popular risk measures in banking and insurance regulation. To bridge between the two regulatory risk measures, the Probabilit...

We study the aggregation of two risks when the marginal distributions are known and the dependence structure is unknown, under the additional constraint that one risk is smaller than or equal to the...

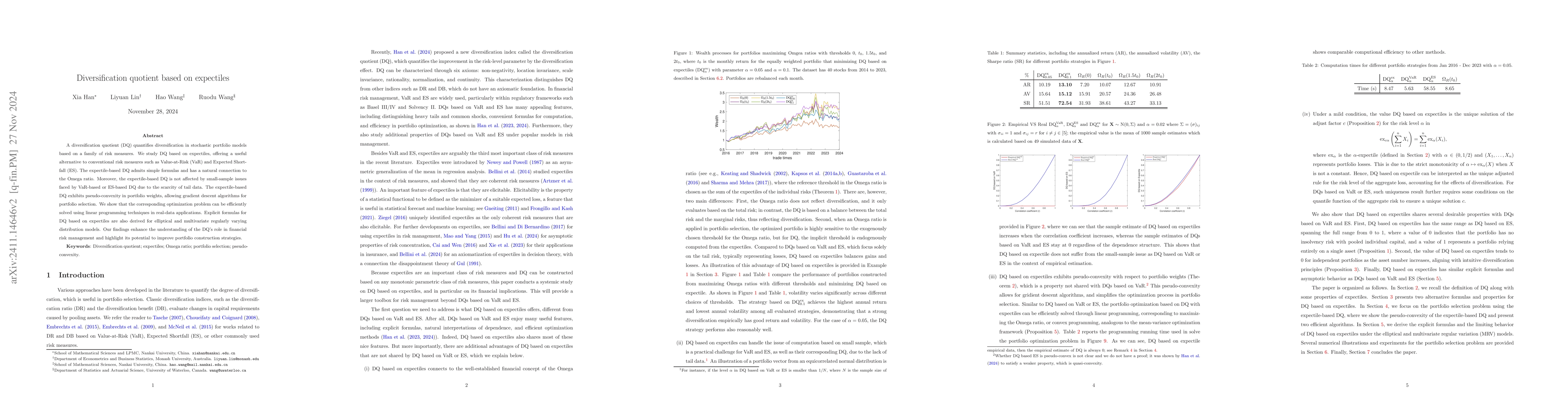

A diversification quotient (DQ) quantifies diversification in stochastic portfolio models based on a family of risk measures. We study DQ based on expectiles, offering a useful alternative to conventi...

The Diversification Quotient (DQ), introduced by Han et al. (2025), is a recently proposed measure of portfolio diversification that quantifies the reduction in a portfolio's risk-level parameter attr...

Value-at-Risk (VaR) is a standard regulatory risk measure, and its failure of subadditivity is well known. Much less appreciated is that for sufficiently heavy-tailed losses, VaR can be superadditive ...