Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this article we introduce a portfolio optimisation framework, in which the use of rough path signatures (Lyons, 1998) provides a novel method of incorporating path-dependencies in the joint signa...

We propose a novel generative model for multivariate discrete-time time series data. Drawing inspiration from the construction of neural spline flows, our algorithm incorporates linear transformatio...

We present a method for finding optimal hedging policies for arbitrary initial portfolios and market states. We develop a novel actor-critic algorithm for solving general risk-averse stochastic cont...

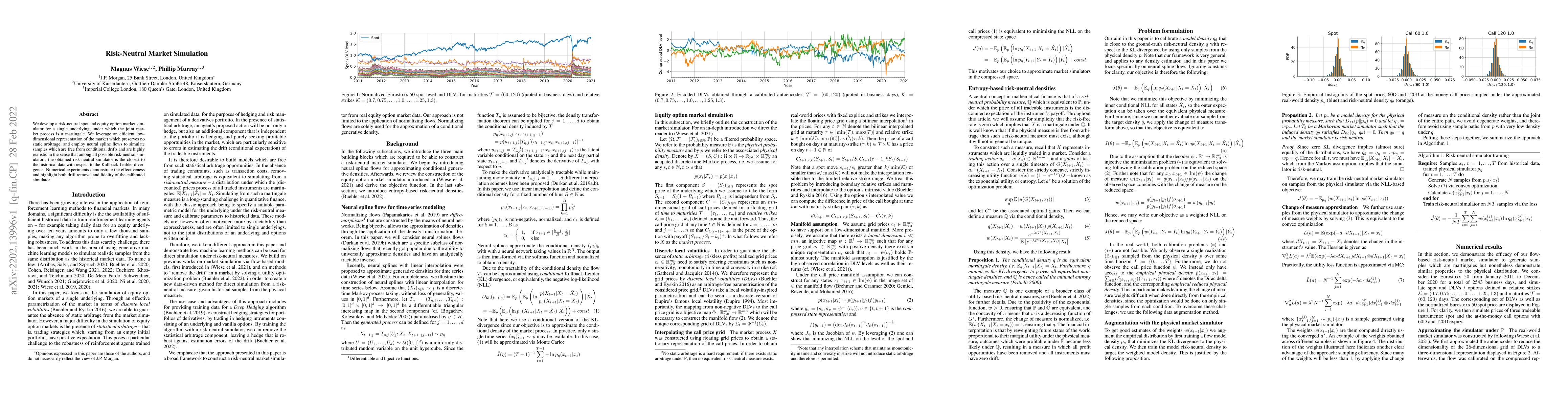

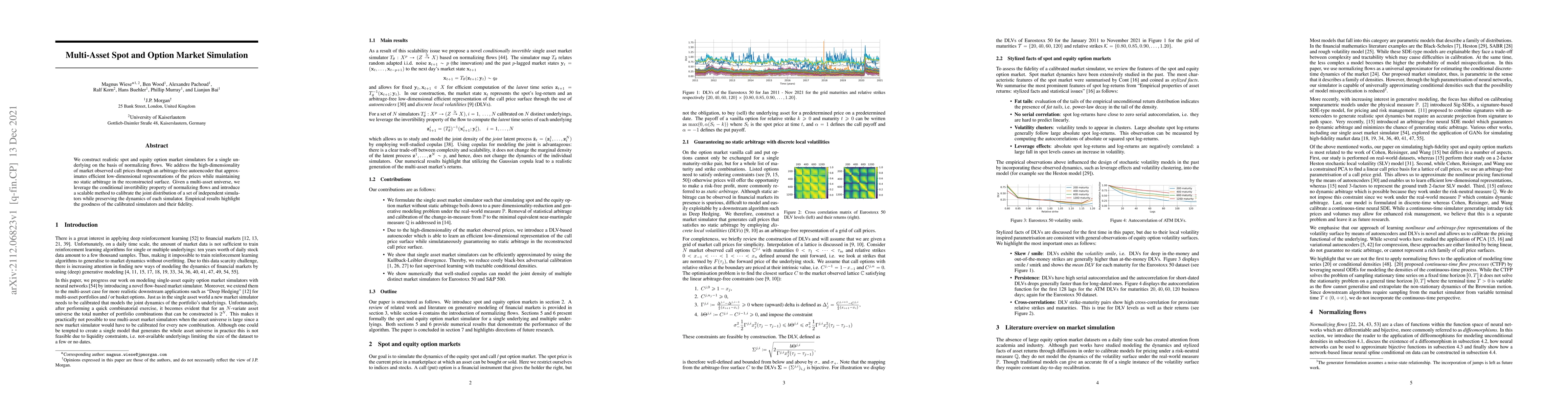

We develop a risk-neutral spot and equity option market simulator for a single underlying, under which the joint market process is a martingale. We leverage an efficient low-dimensional representati...

We construct realistic spot and equity option market simulators for a single underlying on the basis of normalizing flows. We address the high-dimensionality of market observed call prices through a...

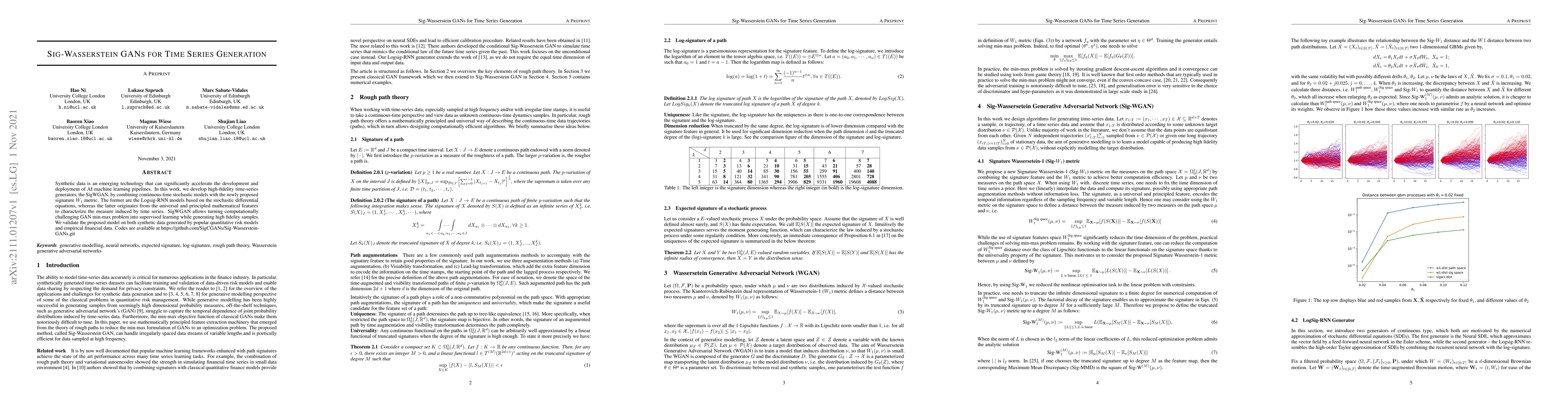

Synthetic data is an emerging technology that can significantly accelerate the development and deployment of AI machine learning pipelines. In this work, we develop high-fidelity time-series generat...

Generative adversarial networks (GANs) have been extremely successful in generating samples, from seemingly high dimensional probability measures. However, these methods struggle to capture the temp...

We construct realistic equity option market simulators based on generative adversarial networks (GANs). We consider recurrent and temporal convolutional architectures, and assess the impact of state...

Modeling financial time series by stochastic processes is a challenging task and a central area of research in financial mathematics. As an alternative, we introduce Quant GANs, a data-driven model ...

Deep generative networks such as GANs and normalizing flows flourish in the context of high-dimensional tasks such as image generation. However, so far exact modeling or extrapolation of distributio...