Academic Profile

Statistics

Similar Authors

Papers on arXiv

We numerically study the distribution of the lowest eigenvalue of finite many-boson systems with $k$-body interactions modeled by Bosonic Embedded Gaussian Orthogonal [BEGOE($k$)] and Unitary [BEGUE...

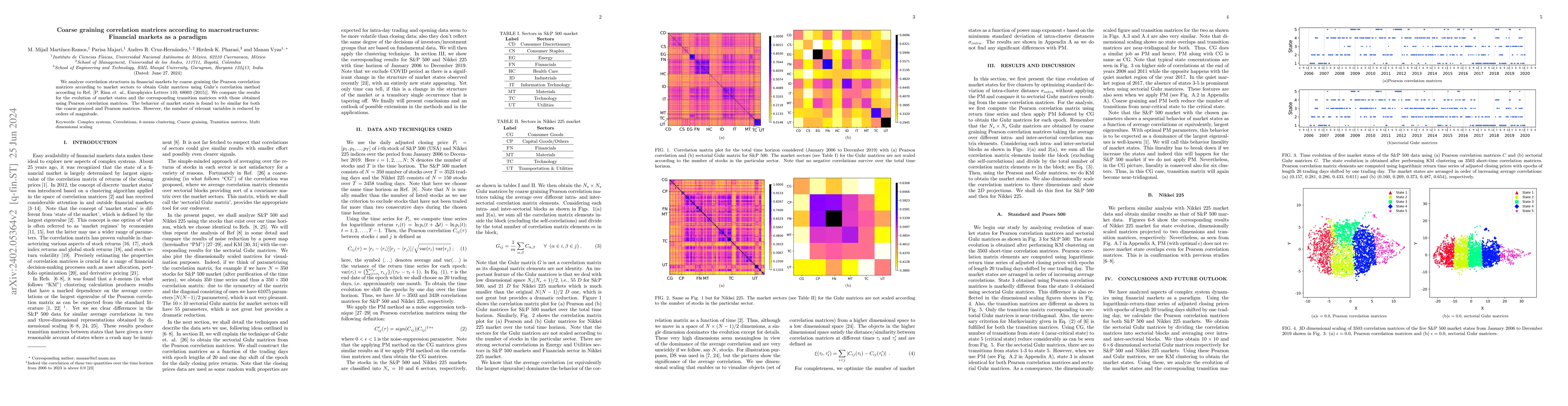

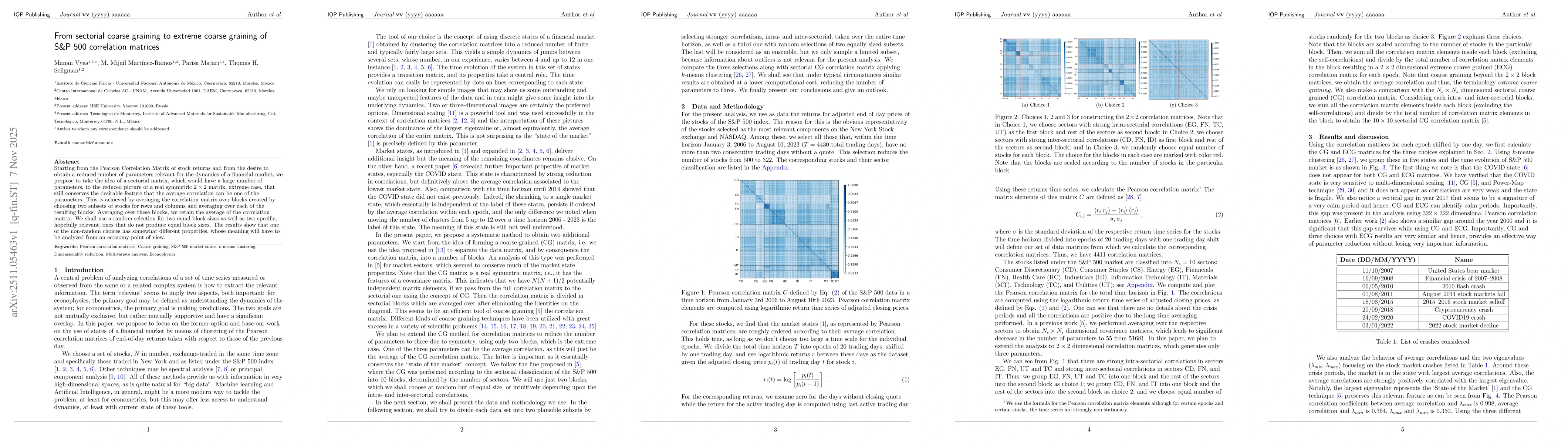

We analyze correlation structures in financial markets by coarse graining the Pearson correlation matrices according to market sectors to obtain Guhr matrices using Guhr's correlation method accordi...

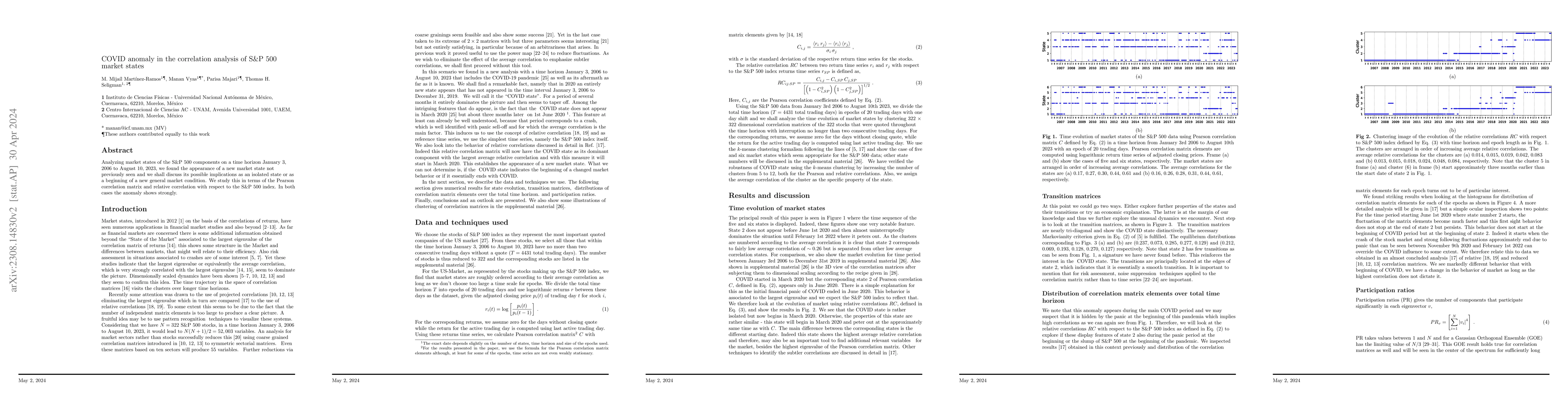

Analyzing market states of the S&P 500 components on a time horizon January 3, 2006 to August 10, 2023, we found the appearance of a new market state not previously seen and we shall discuss its pos...

Eigenvalue density generated by embedded Gaussian unitary ensemble with $k$-body interactions for two species (say $\mathbf{\pi}$ and $\mathbf{\nu}$) fermion systems is investigated by deriving form...

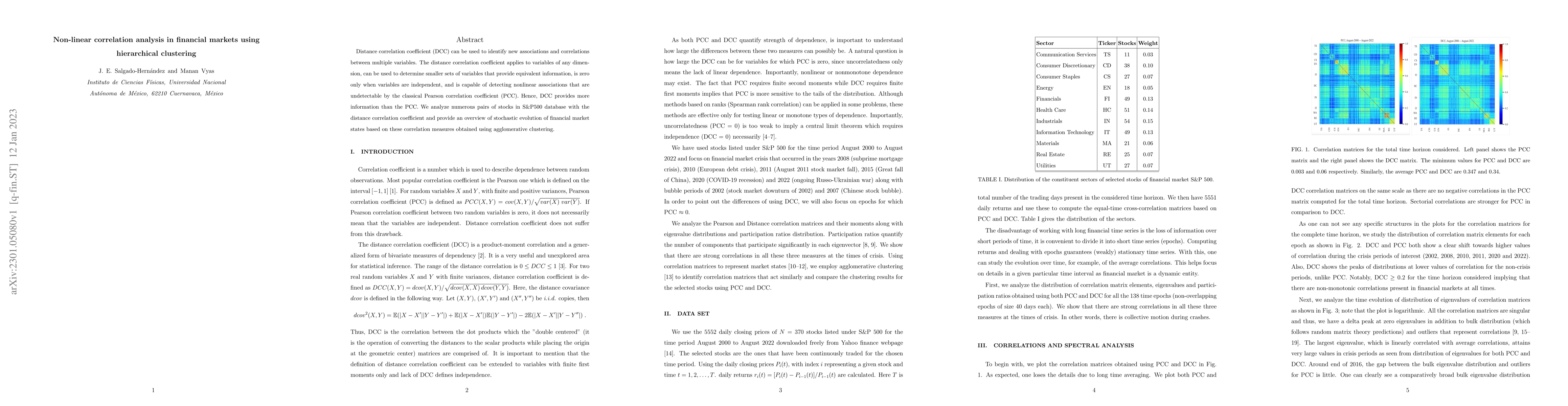

Distance correlation coefficient (DCC) can be used to identify new associations and correlations between multiple variables. The distance correlation coefficient applies to variables of any dimensio...

Statistical nuclear spectroscopy (also called spectral distribution method), introduced by J.B. French in late 60's and developed in detail in the later years by his group and many other groups, is ...

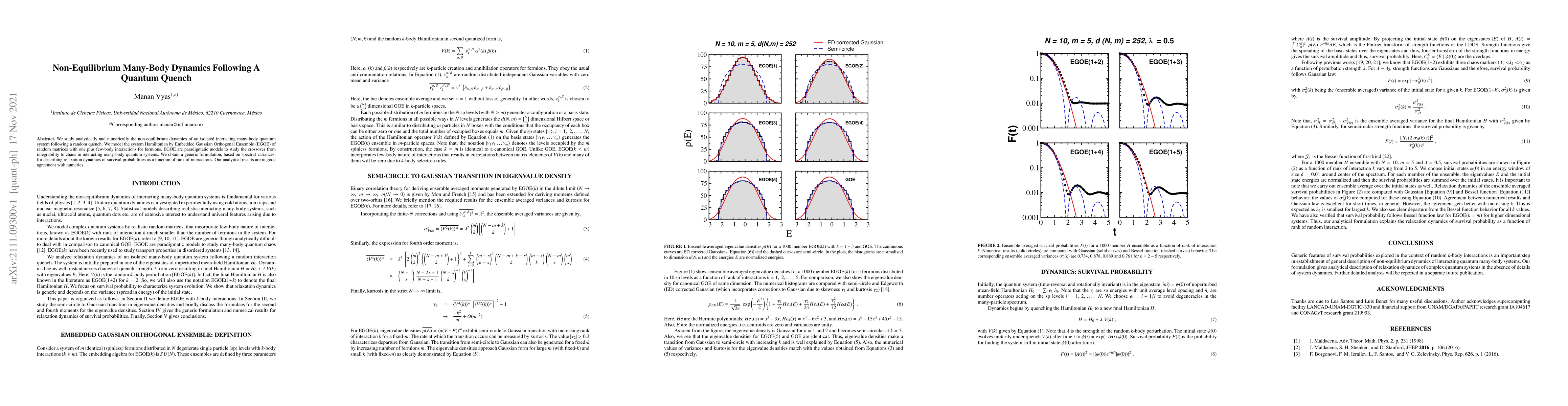

We study analytically and numerically the non-equilibrium dynamics of an isolated interacting many-body quantum system following a random quench. We model the system Hamiltonian by Embedded Gaussian...

We analyze the structure of eigenstates in many-body bosonic systems by modeling the Hamiltonian of these complex systems using Bosonic Embedded Gaussian Orthogonal Ensembles (BEGOE) defined by a me...

For finite quantum many-particle systems modeled with say $m$ fermions in $N$ single particle states and interacting with $k$-body interactions ($k \leq m$), the wavefunction structure is studied us...

Recently it is established, via lower order moments, that the univariate q-normal distribution, which is the weight function for $q$-Hermite polynomials, describes the ensemble averaged eigenvalue d...

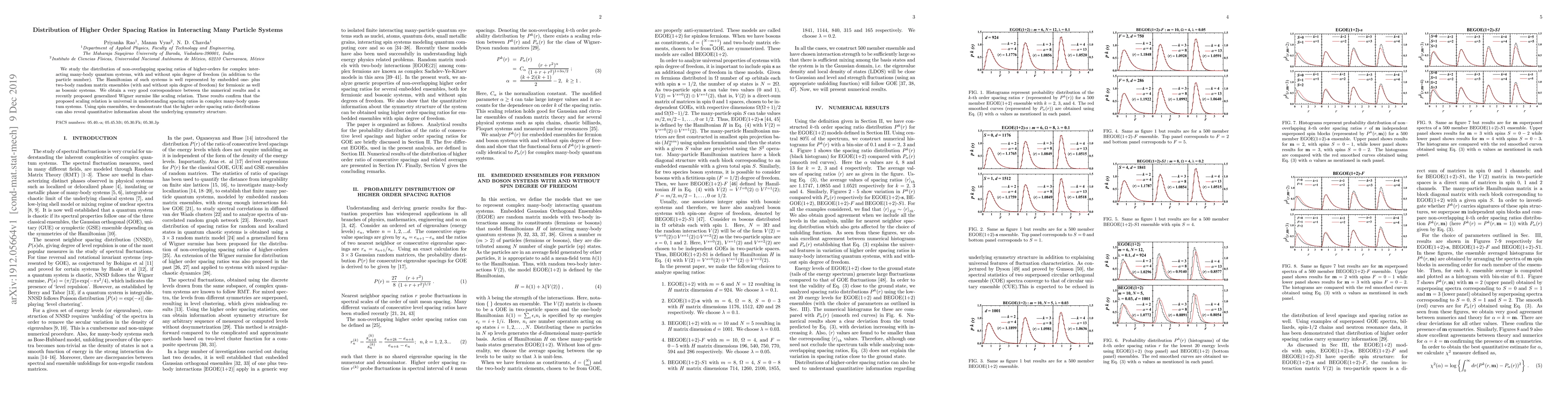

We study the distribution of non-overlapping spacing ratios of higher-orders for complex interacting many-body quantum systems, with and without spin degree of freedom (in addition to the particle n...

When dealing with non-stationary systems, for which many time series are available, it is common to divide time in epochs, i.e. smaller time intervals and deal with short time series in the hope to ...

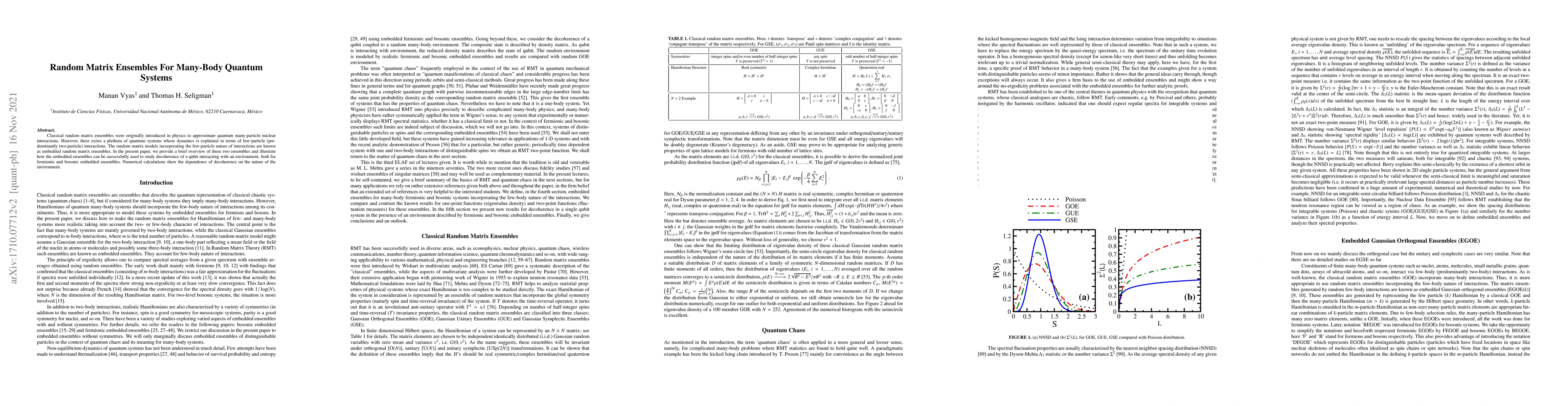

Classical random matrix ensembles were originally introduced in physics to approximate quantum many-particle nuclear interactions. However, there exists a plethora of quantum systems whose dynamics ...

Starting from the Pearson Correlation Matrix of stock returns and from the desire to obtain a reduced number of parameters relevant for the dynamics of a financial market, we propose to take the idea ...

Embedded random matrix ensembles operating in nuclear shell model spaces, with nucleons occupying a finite set of single particle orbits and interacting via a two-body interaction, form the basis for ...