Academic Profile

Statistics

Similar Authors

Papers on arXiv

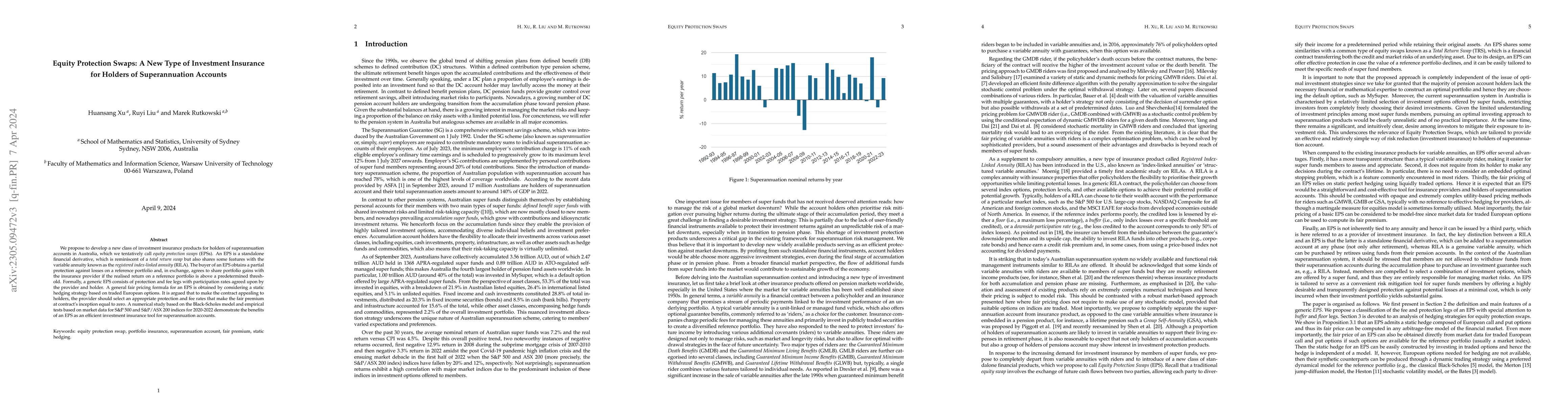

We propose to develop a new class of investment insurance products for holders of superannuation accounts in Australia, which we tentatively call equity protection swaps (EPSs). An EPS is a standalo...

We study the upper and lower bounds for prices of European and American style options with the possibility of an external termination, meaning that the contract may be terminated at some random time...

The paper is directly motivated by the pricing of vulnerable European and American options in a general hazard process setup and a related study of the corresponding pre-default backward stochastic ...

We study generalized backward stochastic differential equations (BSDEs) up to a random time horizon $\vartheta$, which is not a stopping time, under minimal assumptions regarding the properties of $...

We prove some new results on reflected BSDEs and doubly reflected BSDEs driven by a multi-dimensional RCLL martingale. The goal is to develop a general multi-asset framework encompassing a wide spec...

Results on the existence, uniqueness and strict comparison for solutions to a BSDE driven by a multi-dimensional RCLL martingale are established. The goal is to develop a general multi-asset framewo...

The financial industry has undergone a significant transition from the London Interbank Offered Rate (LIBOR) to Risk Free Rates (RFR) such as, e.g., the Secured Overnight Financing Rate (SOFR) in the ...

In this paper, we explore the pricing and hedging strategies for an innovative insurance product called the equity protection swap(EPS). Notably, we focus on the application of EPSs involving cross-cu...

The role of collateral in derivative pricing has evolved beyond credit risk mitigation, particularly following the global financial crisis, when funding costs and basis spreads became central to valua...

This paper examines the valuation and hedging of standard equity protection swap (EPS) products proposed by Xu et al.. To account for financial crises and counterparty default risk, we develop pricing...