Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this study, we introduce a physical model inspired by statistical physics for predicting price volatility and expected returns by leveraging Level 3 order book data. By drawing parallels between ...

Spatial models of preference, in the form of vector embeddings, are learned by many deep learning and multiagent systems, including recommender systems. Often these models are assumed to approximate...

The introduction of electronic trading platforms effectively changed the organisation of traditional systemic trading from quote-driven markets into order-driven markets. Its convenience led to an e...

We study strategic candidate positioning in multidimensional spatial-voting elections. Voters and candidates are represented as points in $\mathbb{R}^d$, and each voter supports the candidate that is ...

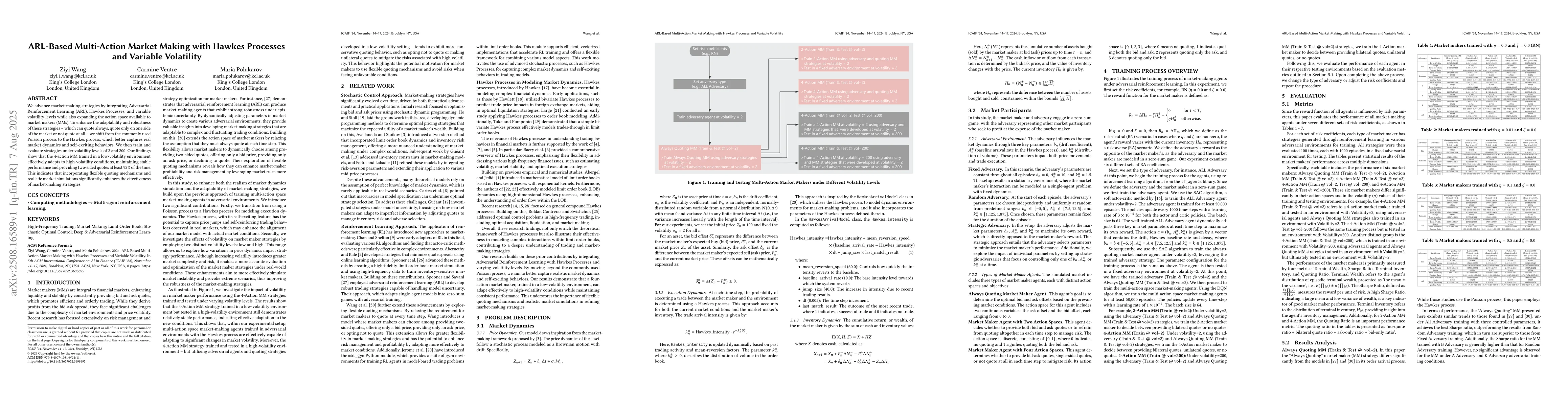

We advance market-making strategies by integrating Adversarial Reinforcement Learning (ARL), Hawkes Processes, and variable volatility levels while also expanding the action space available to market ...

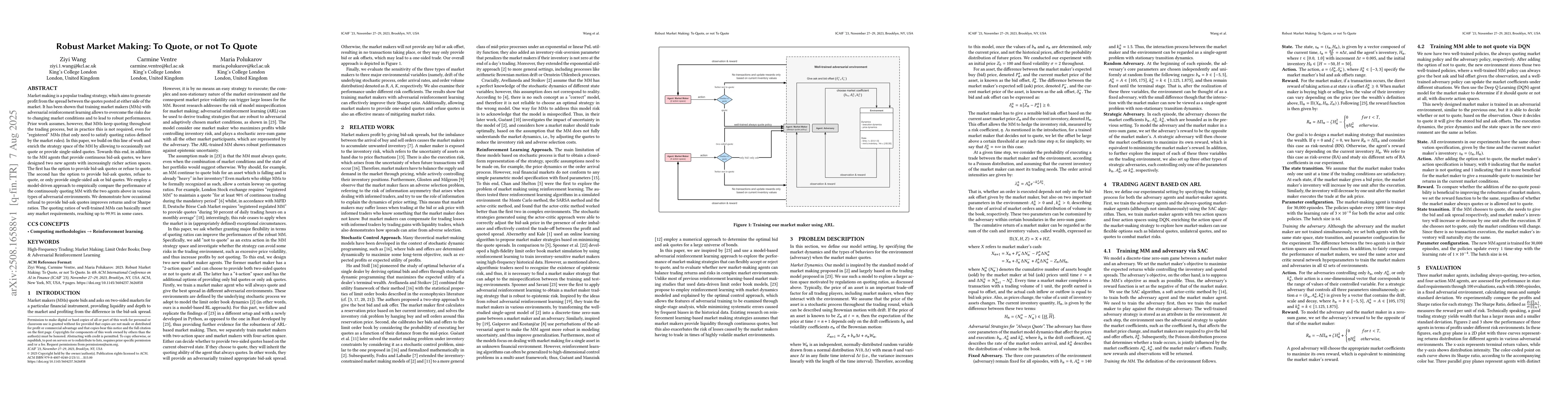

Market making is a popular trading strategy, which aims to generate profit from the spread between the quotes posted at either side of the market. It has been shown that training market makers (MMs) w...

In multiwinner approval elections with many candidates, voters may struggle to determine their preferences over the entire slate of candidates. It is therefore of interest to explore which (if any) fa...

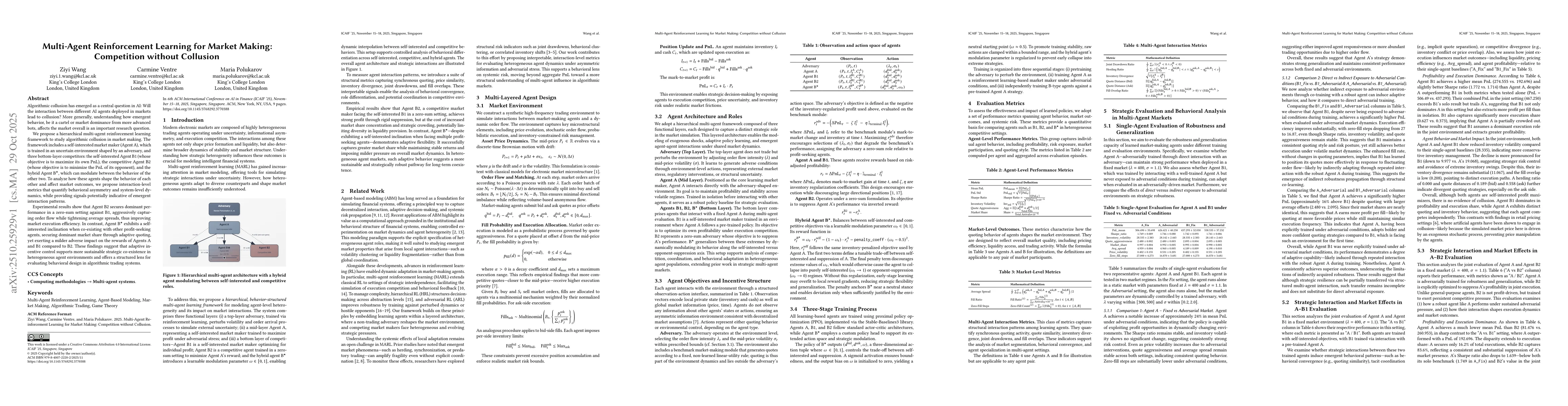

Algorithmic collusion has emerged as a central question in AI: Will the interaction between different AI agents deployed in markets lead to collusion? More generally, understanding how emergent behavi...

We study the computational complexity of strategic behaviour in primary elections. Unlike direct voting systems, primaries introduce a multi-stage process in which voters first influence intra-party n...

Large language models (LLMs) are increasingly deployed as interactive agents, yet their capacity for social and strategic reasoning over extended interaction remains poorly understood. Existing evalua...

In multiwinner elections with many candidates, as in participatory budgeting or large-scale recommendation, voters cannot plausibly evaluate every candidate, yet standard proportional-fairness guarant...