Algorithmic collusion has emerged as a central question in AI: Will the

interaction between different AI agents deployed in markets lead to collusion?

More generally, understanding how emergent behavior, be it a cartel or market

dominance from more advanced bots, affects the market overall is an important

research question.

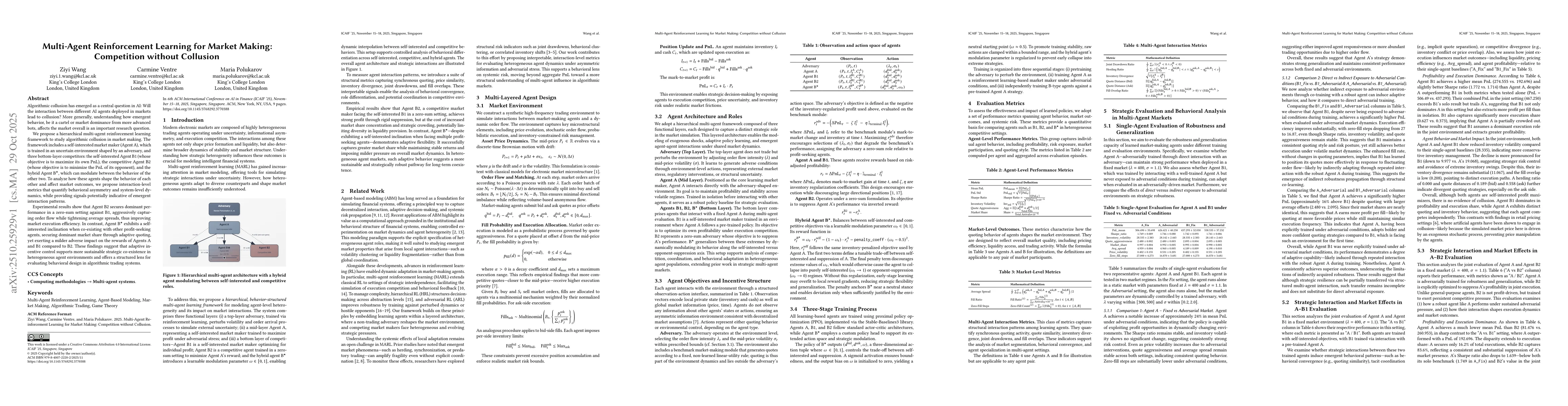

We propose a hierarchical multi-agent reinforcement learning framework to

study algorithmic collusion in market making. The framework includes a

self-interested market maker (Agent~A), which is trained in an uncertain

environment shaped by an adversary, and three bottom-layer competitors: the

self-interested Agent~B1 (whose objective is to maximize its own PnL), the

competitive Agent~B2 (whose objective is to minimize the PnL of its opponent),

and the hybrid Agent~B$^\star$, which can modulate between the behavior of the

other two. To analyze how these agents shape the behavior of each other and

affect market outcomes, we propose interaction-level metrics that quantify

behavioral asymmetry and system-level dynamics, while providing signals

potentially indicative of emergent interaction patterns.

Experimental results show that Agent~B2 secures dominant performance in a

zero-sum setting against B1, aggressively capturing order flow while tightening

average spreads, thus improving market execution efficiency. In contrast,

Agent~B$^\star$ exhibits a self-interested inclination when co-existing with

other profit-seeking agents, securing dominant market share through adaptive

quoting, yet exerting a milder adverse impact on the rewards of Agents~A and B1

compared to B2. These findings suggest that adaptive incentive control supports

more sustainable strategic co-existence in heterogeneous agent environments and

offers a structured lens for evaluating behavioral design in algorithmic

trading systems.

Discussion 0