Academic Profile

Statistics

Similar Authors

Papers on arXiv

Quantile-Quantile (Q-Q) plots are widely used for assessing the distributional similarity between two datasets. Traditionally, Q-Q plots are constructed for univariate distributions, making them les...

We consider the empirical versions of geometric quantile and halfspace depth, and study their extremal behaviour as a function of the sample size. The objective of this study is to establish connect...

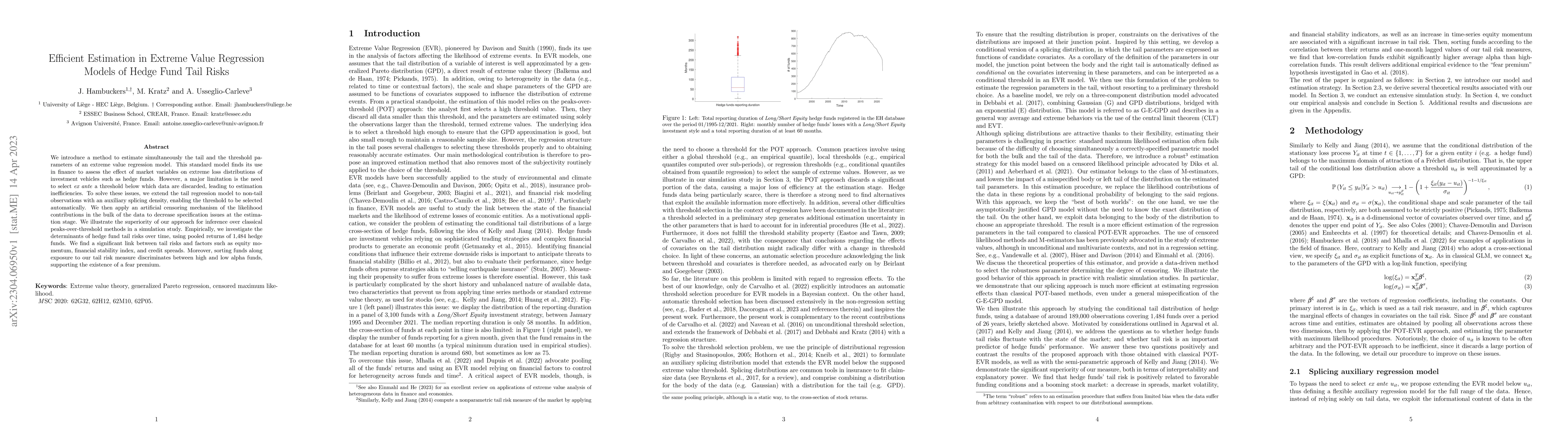

We introduce a method to estimate simultaneously the tail and the threshold parameters of an extreme value regression model. This standard model finds its use in finance to assess the effect of mark...

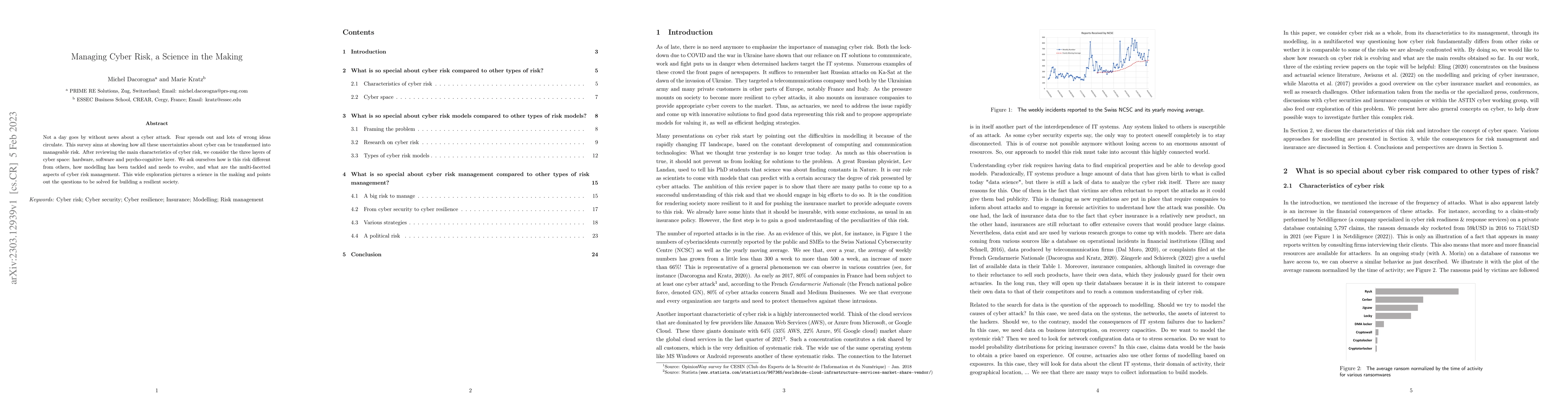

Not a day goes by without news about a cyber attack. Fear spreads out and lots of wrong ideas circulate. This survey aims at showing how all these uncertainties about cyber can be transformed into m...

The study of concomitants has recently met a renewed interest due to its applications in selection procedures. For instance, concomitants are used in ranked-set sampling, to achieve efficiency and r...

Cyber security and resilience are major challenges in our modern economies; this is why they are top priorities on the agenda of governments, security and defense forces, management of companies and...

In this paper, we establish a joint (bivariate) functional central limit theorem of the sample quantile and the $r$-th absolute centred sample moment for functionals of mixing processes. More precis...

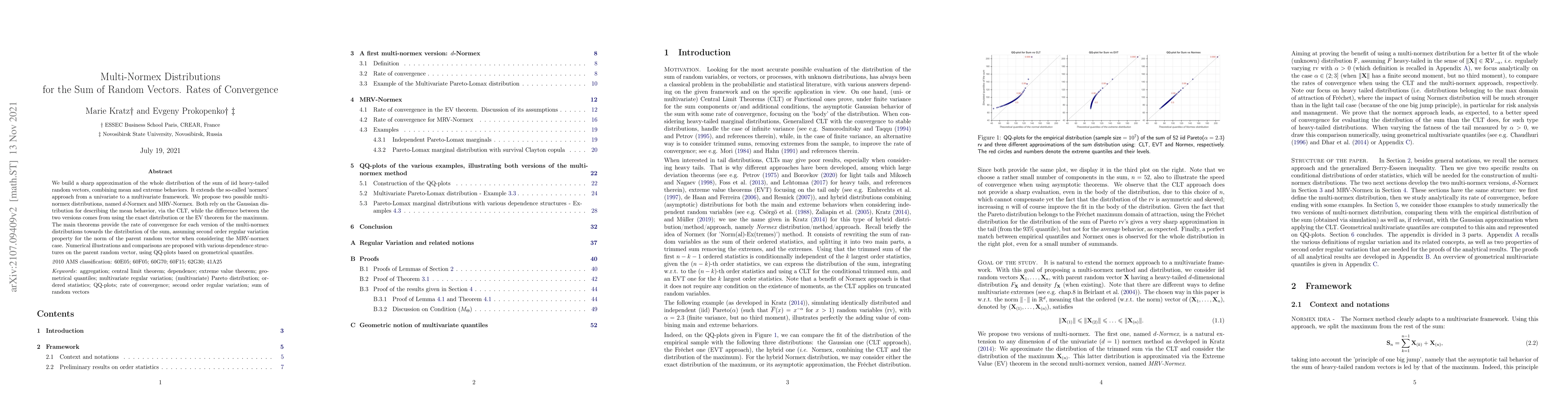

We build a sharp approximation of the whole distribution of the sum of iid heavy-tailed random vectors, combining mean and extreme behaviors. It extends the so-called 'normex' approach from a univar...

Procyclicality of historical risk measure estimation means that one tends to over-estimate future risk when present realized volatility is high and vice versa under-estimate future risk when the rea...

Measures of risk concentration and their asymptotic behavior for portfolios with heavy-tailed risk factors is of interest in risk management. Second order regular variation is a structural assumptio...

We study the empirical version of halfspace depths with the objective of establishing a connection between the rates of convergence and the tail behaviour of the corresponding underlying distributions...

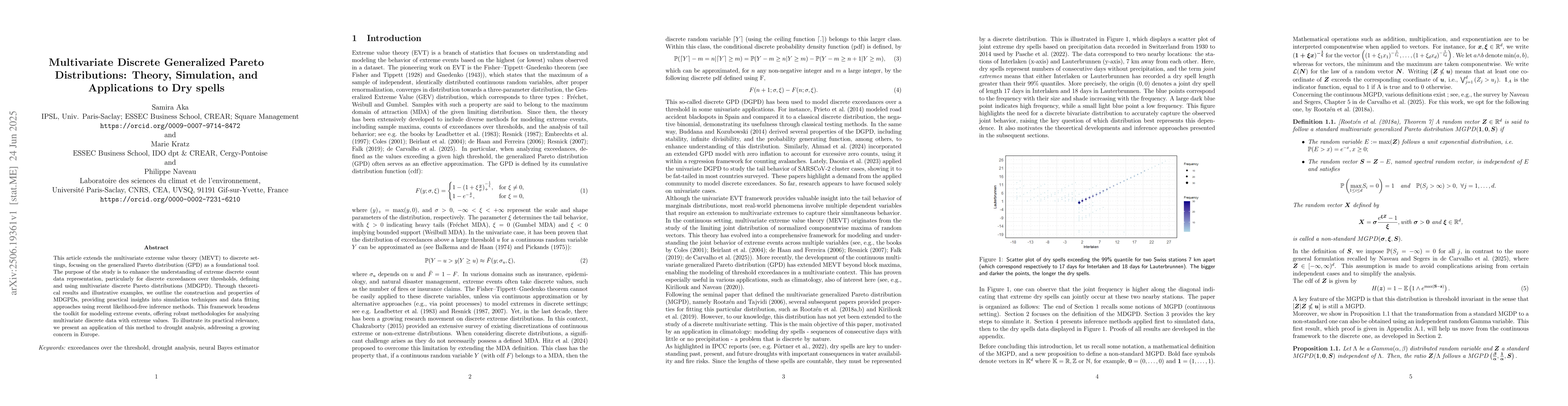

This article extends the multivariate extreme value theory (MEVT) to discrete settings, focusing on the generalized Pareto distribution (GPD) as a foundational tool. The purpose of the study is to enh...

In this paper, we investigate the regularization effects, in the sense of Malliavin calculus, on functionals of Gaussian processes induced by time integration, focusing on their covariance functions. ...

Geometric (also known as spatial) quantiles, introduced by Chaudhury and representing one of the three principal approaches to defining multivariate quantiles, have been well studied in the literature...

Likelihood-based inference for multivariate extreme-value models is often unreliable or infeasible when likelihoods are intractable or supports are discrete. This challenge is particularly acute for m...

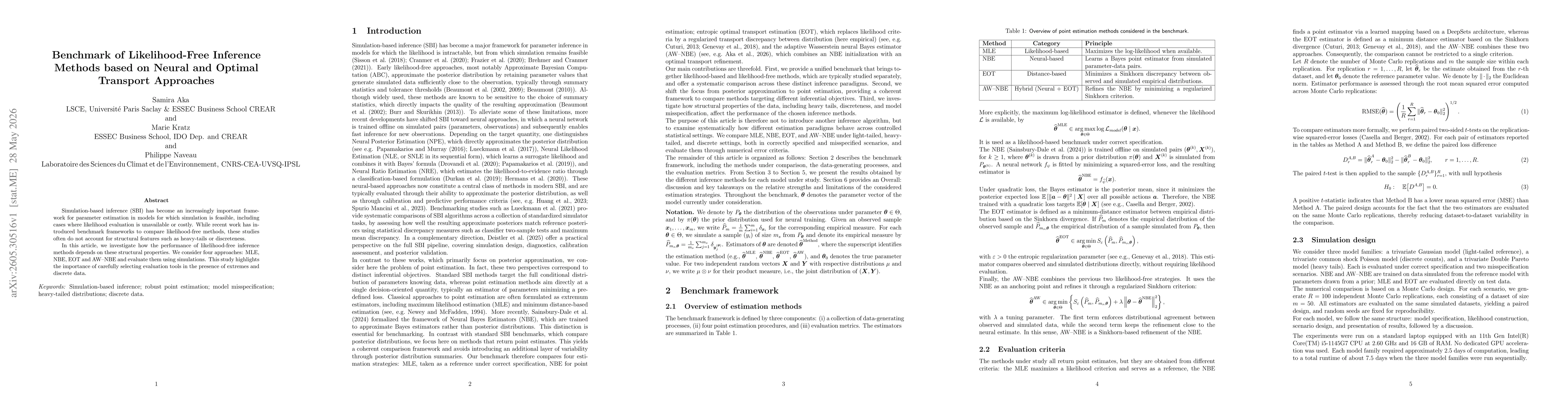

Simulation-based inference (SBI) has become an increasingly important framework for parameter estimation in models for which simulation is feasible, including cases where likelihood evaluation is unav...