Academic Profile

Statistics

Similar Authors

Papers on arXiv

One challenge in the estimation of financial market agent-based models (FABMs) is to infer reliable insights using numerical simulations validated by only a single observed time series. Ergodicity (...

An important but understudied question in economics is how people choose when facing uncertainty in the timing of events. Here we study preferences over time lotteries, in which the payment amount i...

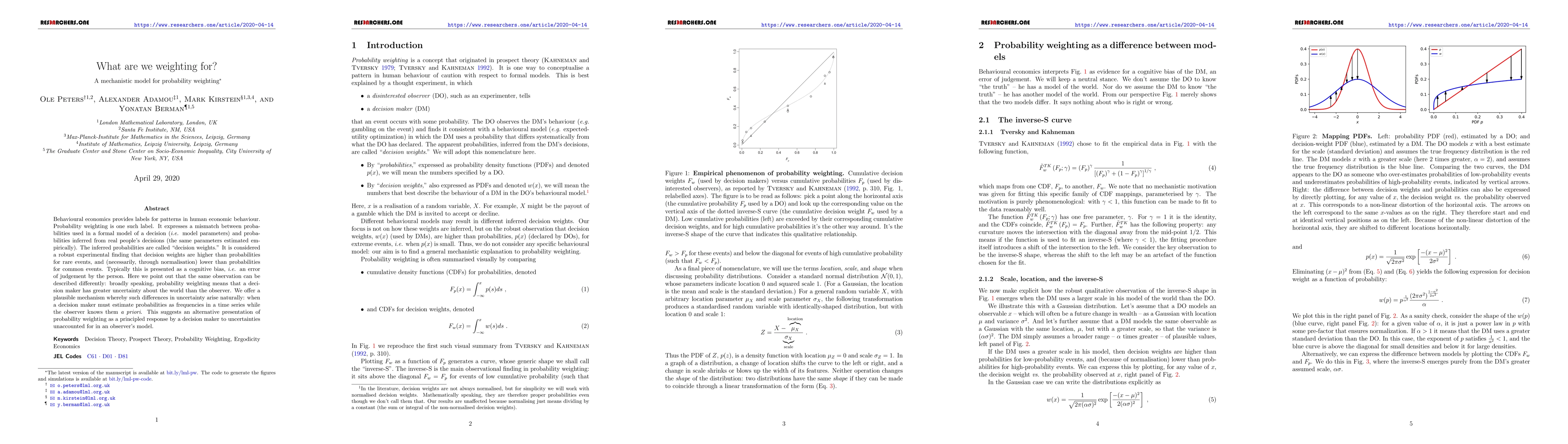

Behavioural economics provides labels for patterns in human economic behaviour. Probability weighting is one such label. It expresses a mismatch between probabilities used in a formal model of a dec...