Academic Profile

Statistics

Similar Authors

Papers on arXiv

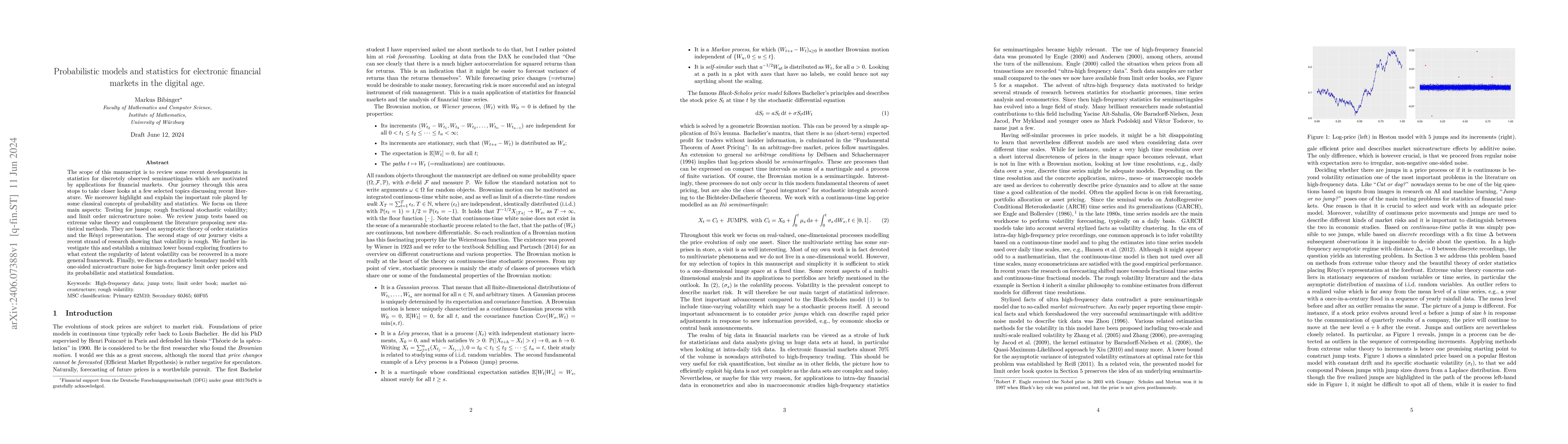

The scope of this manuscript is to review some recent developments in statistics for discretely observed semimartingales which are motivated by applications for financial markets. Our journey throug...

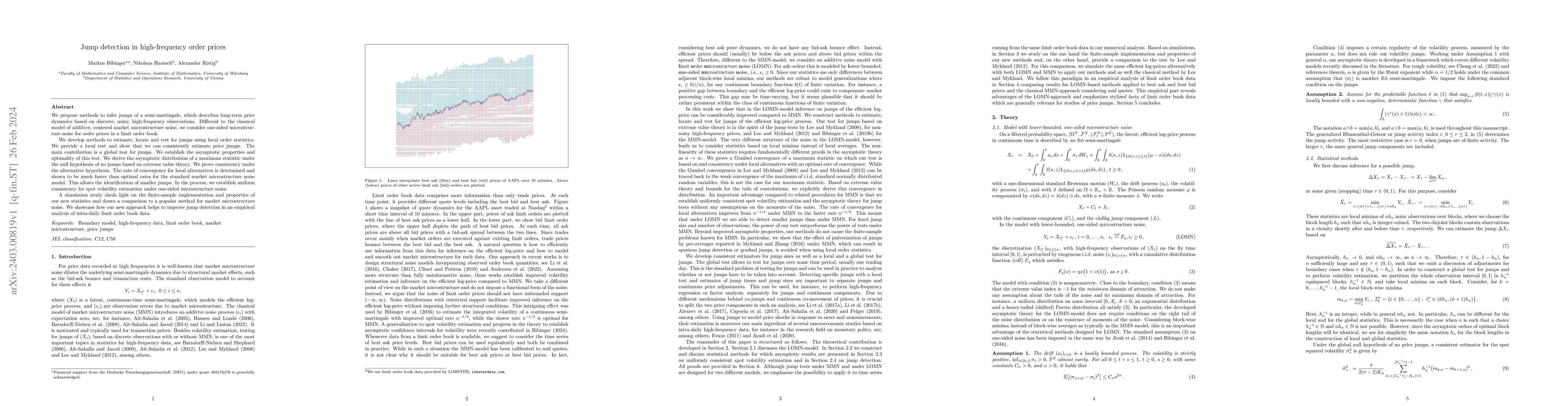

We propose methods to infer jumps of a semi-martingale, which describes long-term price dynamics based on discrete, noisy, high-frequency observations. Different to the classical model of additive, ...

We develop and investigate a test for jumps based on high-frequency observations of a fractional process with an additive jump component. The Hurst exponent of the fractional process is unknown. The...

We consider estimation of the spot volatility in a stochastic boundary model with one-sided microstructure noise for high-frequency limit order prices. Based on discrete, noisy observations of an It...

We construct estimators for the parameters of a parabolic SPDE with one spatial dimension based on discrete observations of a solution in time and space on a bounded domain. We establish central lim...

In this note, we establish the convergence in distribution of the maxima of i.i.d. random variables to the Gumbel distribution with the associated normalizing sequences for several examples that are...

A multivariate fractional Brownian motion (mfBm) with component-wise Hurst exponents is used to model and forecast realized volatility. We investigate the interplay between correlation coefficients an...

The one-sided microstructure noise model for high-frequency quotes from a limit order book is generalized to capture asset-specific noise tail behaviour. Estimation of a noise tail parameter becomes t...