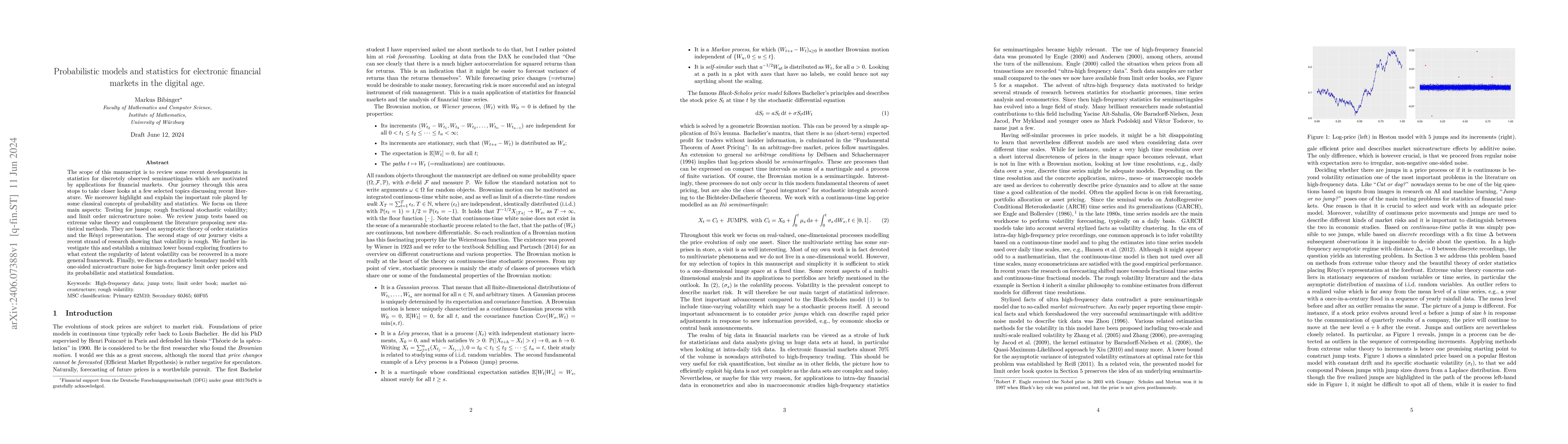

The scope of this manuscript is to review some recent developments in

statistics for discretely observed semimartingales which are motivated by

applications for financial markets. Our journey through this area stops to take

closer looks at a few selected topics discussing recent literature. We moreover

highlight and explain the important role played by some classical concepts of

probability and statistics. We focus on three main aspects: Testing for jumps;

rough fractional stochastic volatility; and limit order microstructure noise.

We review jump tests based on extreme value theory and complement the

literature proposing new statistical methods. They are based on asymptotic

theory of order statistics and the R\'{e}nyi representation. The second stage

of our journey visits a recent strand of research showing that volatility is

rough. We further investigate this and establish a minimax lower bound

exploring frontiers to what extent the regularity of latent volatility can be

recovered in a more general framework. Finally, we discuss a stochastic

boundary model with one-sided microstructure noise for high-frequency limit

order prices and its probabilistic and statistical foundation.

Discussion 0