Academic Profile

Statistics

Similar Authors

Papers on arXiv

Risk and utility functionals are fundamental building blocks in economics and finance. In this paper we investigate under which conditions a risk or utility functional is sensitive to the accumulati...

The Merton investment-consumption problem is fundamental, both in the field of finance, and in stochastic control. An important extension of the problem adds transaction costs, which is highly relev...

We provide an elementary proof of the dual representation of Expected Shortfall on the space of integrable random variables over a general probability space. Unlike the results in the extant literat...

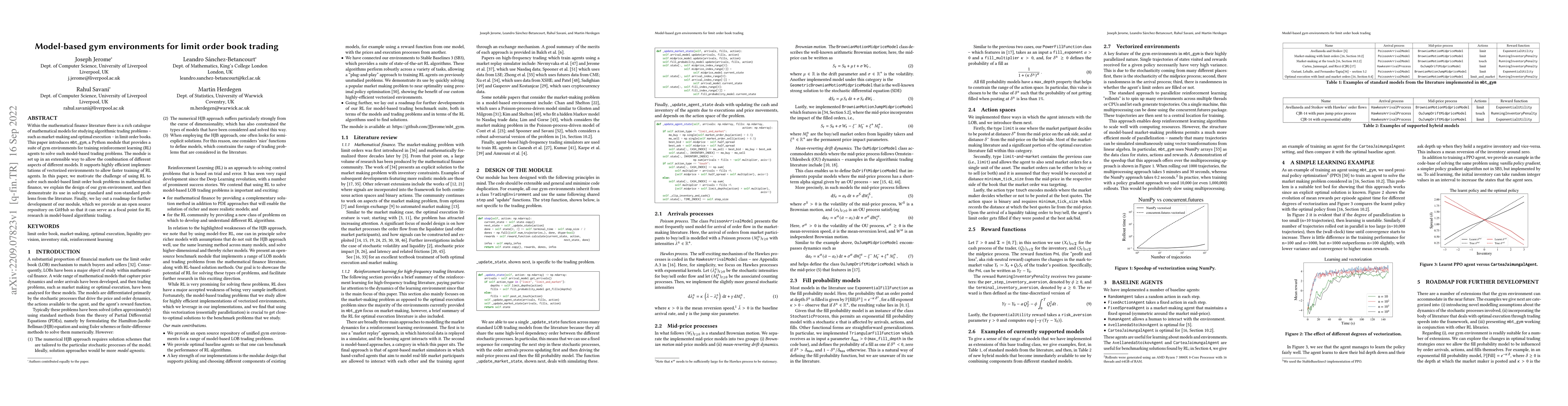

Within the mathematical finance literature there is a rich catalogue of mathematical models for studying algorithmic trading problems -- such as market-making and optimal execution -- in limit order...

Necessary and sufficient conditions for weak and vague convergence of measures are important for a diverse host of applications. This paper aims to give a comprehensive description of the relationsh...

The Laplace transforms of positive measures on $\mathbb{R}_{+}$ converge if and only if their distribution functions converge at continuity points of the limiting measure. We extend this classical c...

In this article, we consider the optimal investment-consumption problem for an agent with preferences governed by Epstein--Zin stochastic differential utility (EZ-SDU) who invests in a constant-para...

We study one-shot Nash competition between an arbitrary number of identical dealers that compete for the order flow of a client. The client trades either because of proprietary information, exposure...

In this article we consider the optimal investment-consumption problem for an agent with preferences governed by Epstein-Zin stochastic differential utility who invests in a constant-parameter Black...

We introduce a new definition of speculative bubbles in discrete-time models based on the discounted stock price losing mass at some finite drop-down under an equivalent martingale measure. We provi...

In this article we consider the infinite-horizon Merton investment-consumption problem in a constant-parameter Black - Scholes - Merton market for an agent with constant relative risk aversion R. Th...

We study risk-sharing economies where heterogenous agents trade subject to quadratic transaction costs. The corresponding equilibrium asset prices and trading strategies are characterised by a syste...

We derive scaling limits for integral functionals of It\^o processes with fast nonlinear mean-reversion speed. We show that in these limits, the fast mean-reverting process is "averaged out" by inte...

We revisit the classical topic of quadratic and linear mean-variance equilibria with both financial and real assets. The novelty of our results is that they are the first allowing for equilibrium pric...

We study liquidity provision in the presence of exogenous competition. We consider a `reference market maker' who monitors her inventory and the aggregated inventory of the competing market makers. We...

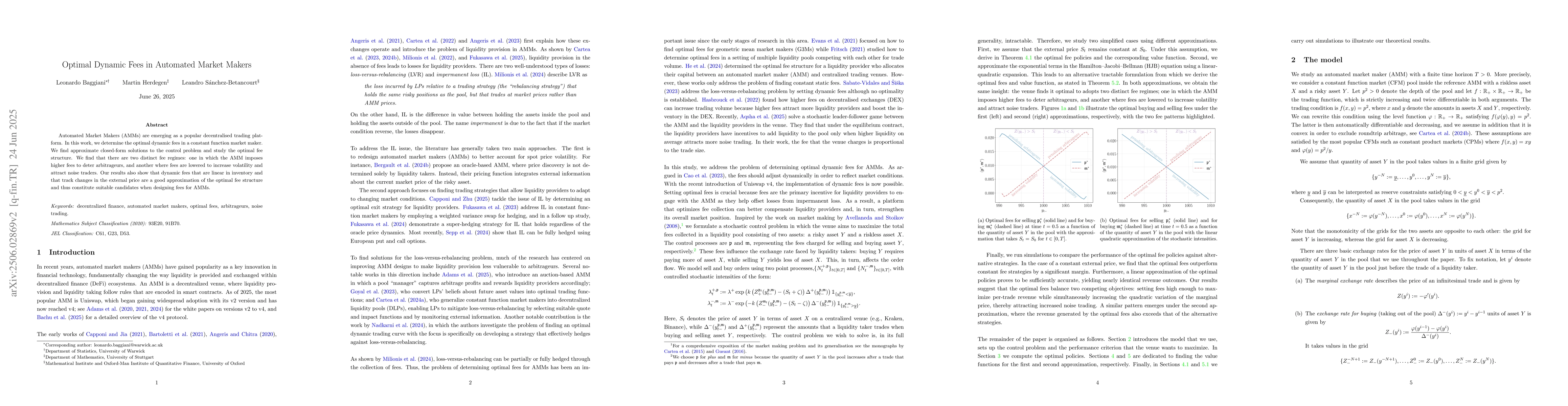

Automated Market Makers (AMMs) are emerging as a popular decentralised trading platform. In this work, we determine the optimal dynamic fees in a constant function market maker. We find approximate cl...

In this article, we study optimal investment and consumption in an incomplete stochastic factor model for a power utility investor on the infinite horizon. When the state space of the stochastic facto...

We revisit the problem of portfolio selection, where an investor maximizes utility subject to a risk constraint. Our framework is very general and accommodates a wide range of utility and risk functio...

We find an approximate Nash equilibrium in a game between decentralized exchanges (DEXs) that compete for order flow by setting dynamic trading fees. We characterize the equilibrium via a coupled syst...