Academic Profile

Statistics

Similar Authors

Papers on arXiv

It has repeatedly been observed that loss minimization by stochastic gradient descent (SGD) leads to heavy-tailed distributions of neural network parameters. Here, we analyze a continuous diffusion ...

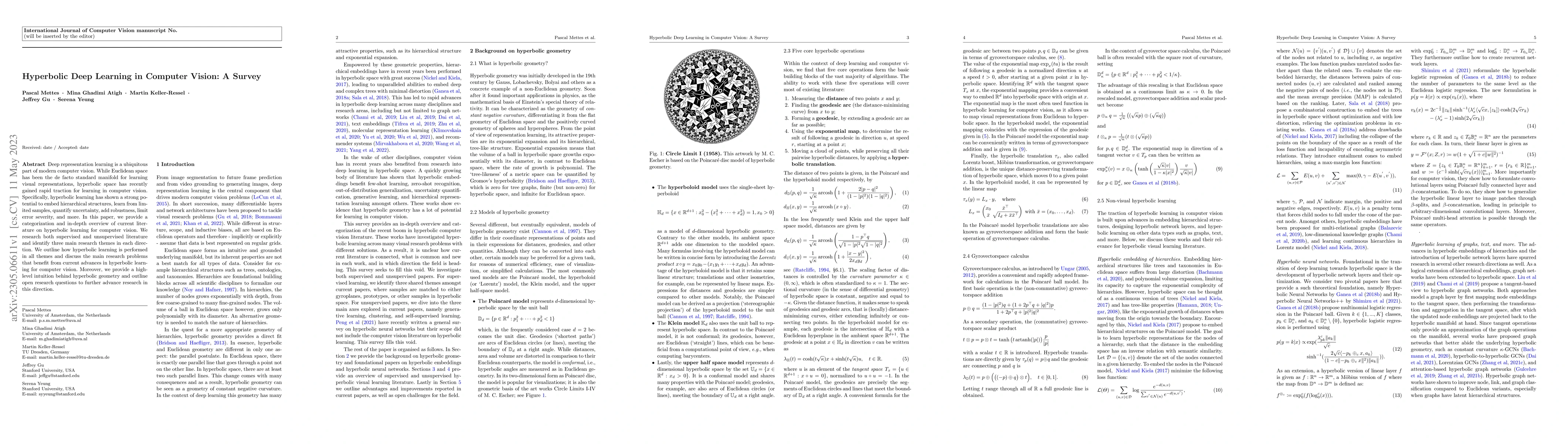

Deep representation learning is a ubiquitous part of modern computer vision. While Euclidean space has been the de facto standard manifold for learning visual representations, hyperbolic space has r...

Using the concept of envelopes we show how to divide the state space $\RR^2$ of the two-factor Vasicek model into regions of identical term-structure shape. We develop a formula for determining the ...

In liquid option markets, W-shaped implied volatility curves have occasionally be observed. We show that such shapes can be reproduced in a mixture of two variance-gamma models. This is in contrast ...

We derive analytic expressions for the variance-optimal hedging strategy and its mean-square hedging error in the lognormal SABR and in the rough Bergomi model. In the SABR model, we show that the v...

We introduce L-hydra (landmarked hyperbolic distance recovery and approximation), a method for embedding network- or distance-based data into hyperbolic space, which requires only the distance measu...

Hyperbolic space has become a popular choice of manifold for representation learning of various datatypes from tree-like structures and text to graphs. Building on the success of deep learning with ...

We introduce Hyperbolic Prototype Learning, a type of supervised learning, where class labels are represented by ideal points (points at infinity) in hyperbolic space. Learning is achieved by minimi...

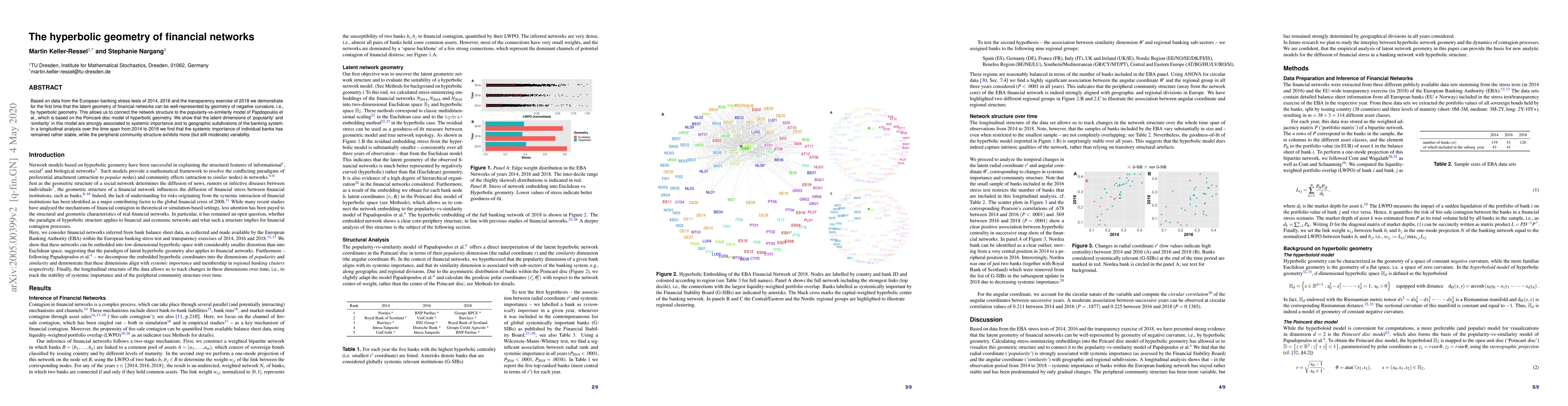

Based on data from the European banking stress tests of 2014, 2016 and the transparency exercise of 2018 we demonstrate for the first time that the latent geometry of financial networks can be well-...

We present a number of related comparison results, which allow to compare moment explosion times, moment generating functions and critical moments between rough and non-rough Heston models of stocha...

We introduce two new measures for the dependence of $n \ge 2$ random variables: distance multivariance and total distance multivariance. Both measures are based on the weighted $L^2$-distance of qua...

We examine the shapes attainable by the forward- and yield-curve in the widely-used Svensson family, including the Nelson-Siegel and Bliss subfamilies. We provide a complete classification of all atta...

We derive a moment formula for generalized fractional polynomial processes, i.e., for polynomial-preserving Markov processes time-changed by an inverse L\'evy-subordinator. If the time change is inver...

We investigate the data-driven discovery of parametric representations for implied volatility slices. Using symbolic regression, we search for simple analytic formulas that approximate the total impli...