Academic Profile

Statistics

Similar Authors

Papers on arXiv

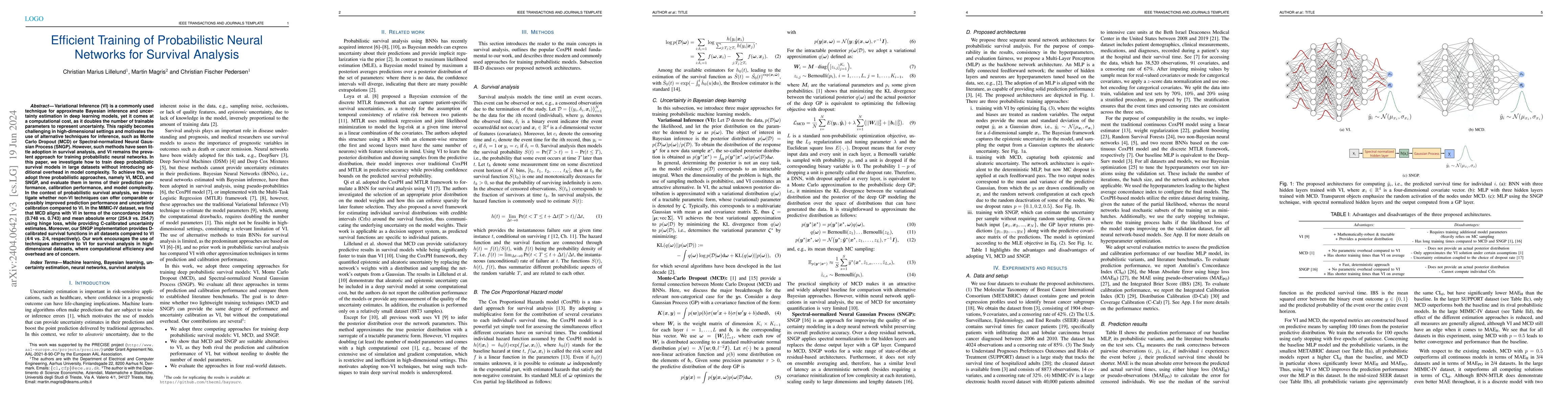

Variational Inference (VI) is a commonly used technique for approximate Bayesian inference and uncertainty estimation in deep learning models, yet it comes at a computational cost, as it doubles the n...

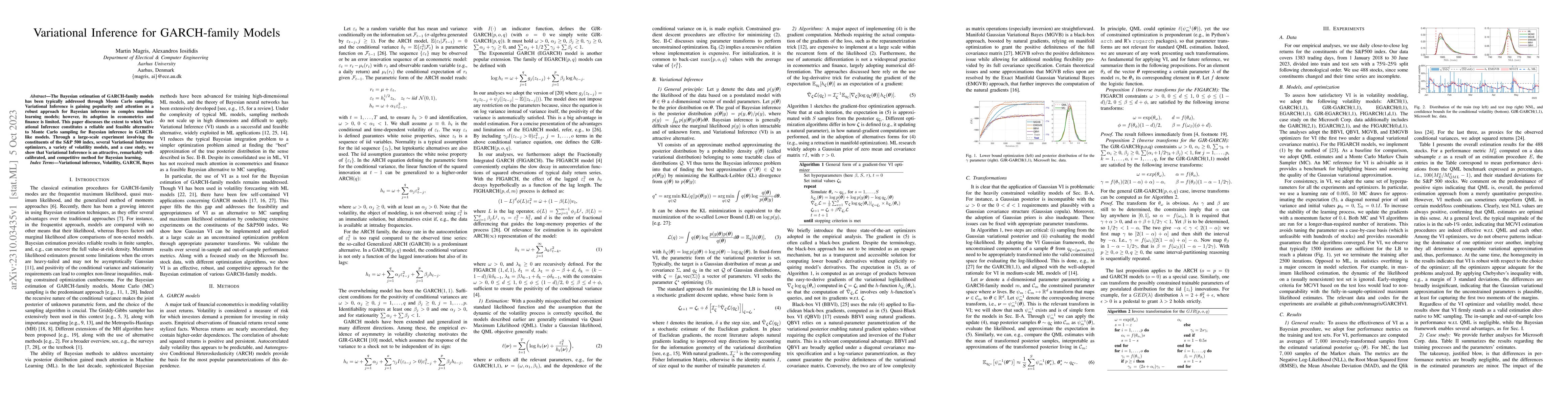

The Bayesian estimation of GARCH-family models has been typically addressed through Monte Carlo sampling. Variational Inference is gaining popularity and attention as a robust approach for Bayesian ...

The last decade witnessed a growing interest in Bayesian learning. Yet, the technicality of the topic and the multitude of ingredients involved therein, besides the complexity of turning theory into...

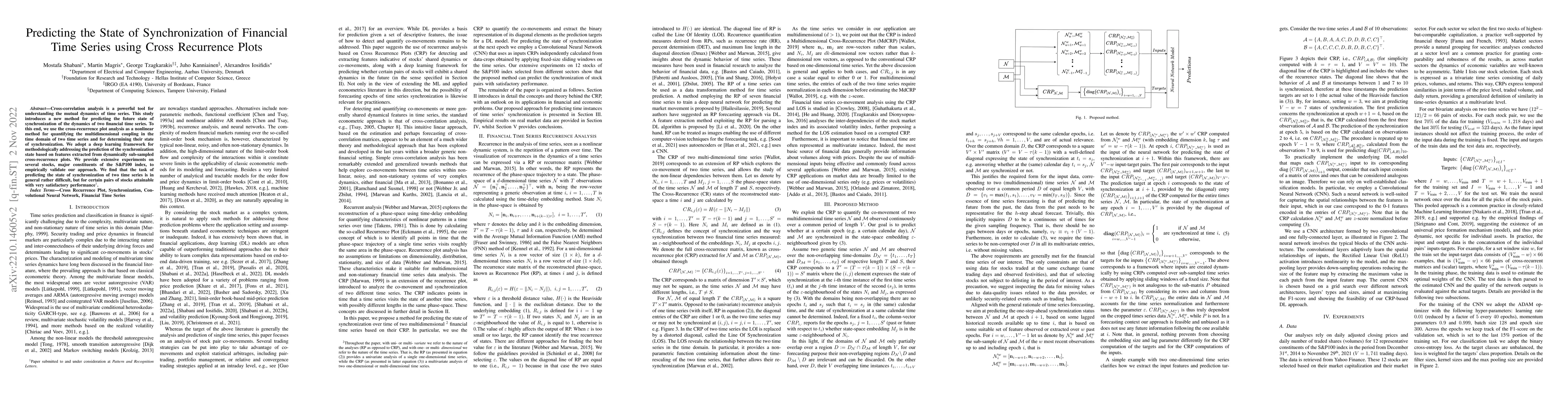

Cross-correlation analysis is a powerful tool for understanding the mutual dynamics of time series. This study introduces a new method for predicting the future state of synchronization of the dynam...

We propose an optimization algorithm for Variational Inference (VI) in complex models. Our approach relies on natural gradient updates where the variational space is a Riemann manifold. We develop a...

We develop an optimization algorithm suitable for Bayesian learning in complex models. Our approach relies on natural gradient updates within a general black-box framework for efficient training wit...

The prediction of financial markets is a challenging yet important task. In modern electronically-driven markets, traditional time-series econometric methods often appear incapable of capturing the ...

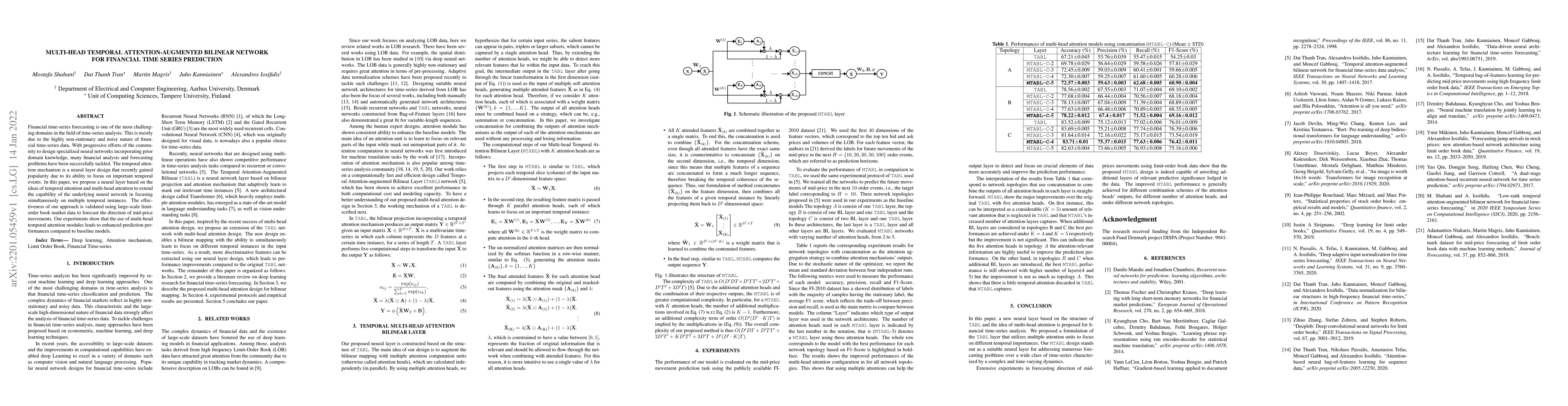

Financial time-series forecasting is one of the most challenging domains in the field of time-series analysis. This is mostly due to the highly non-stationary and noisy nature of financial time-seri...

Several methods have been developed for the simulation of the Hawkes process. The oldest approach is the inverse sampling transform (ITS) suggested in \citep{ozaki1979maximum}, but rapidly abandoned...

The heterogeneous autoregressive (HAR) model is revised by modeling the joint distribution of the four partial-volatility terms therein involved. Namely, today's, yesterday's, last week's and last m...

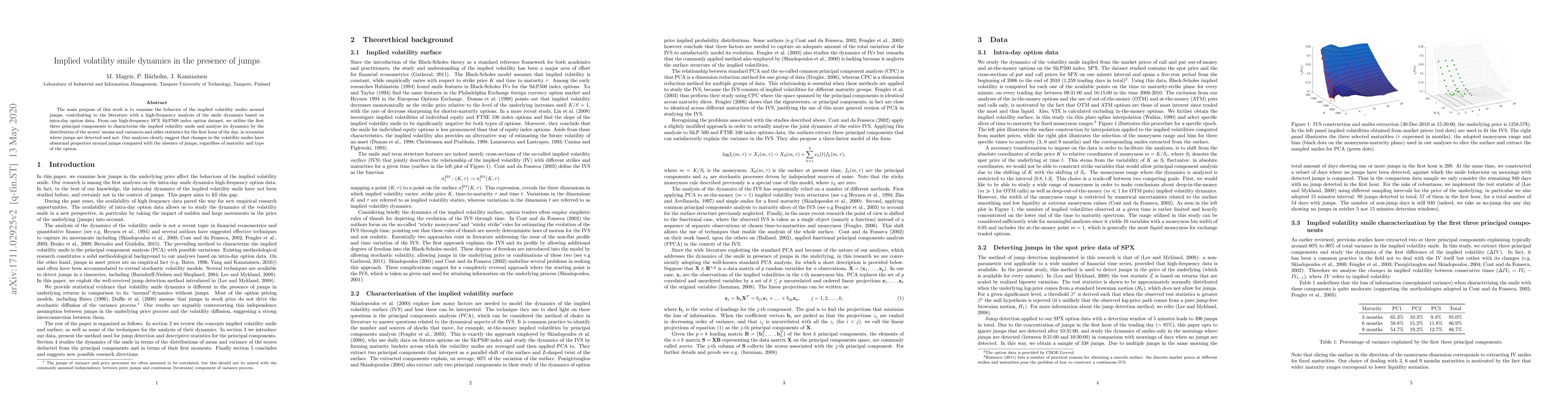

The main purpose of this work is to examine the behavior of the implied volatility smiles around jumps, contributing to the literature with a high-frequency analysis of the smile dynamics based on i...

Time series foundation models (FMs) have emerged as a popular paradigm for zero-shot multi-domain forecasting. These models are trained on numerous diverse datasets and claim to be effective forecaste...