Academic Profile

Statistics

Similar Authors

Papers on arXiv

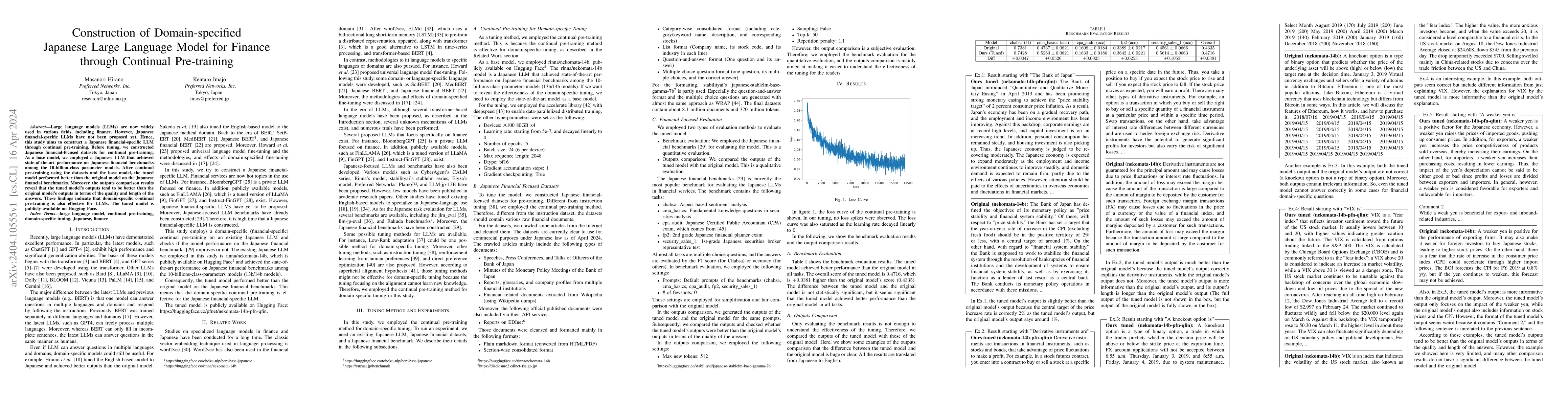

Large language models (LLMs) are now widely used in various fields, including finance. However, Japanese financial-specific LLMs have not been proposed yet. Hence, this study aims to construct a Jap...

Derivative hedging and pricing are important and continuously studied topics in financial markets. Recently, deep hedging has been proposed as a promising approach that uses deep learning to approxi...

With the recent development of large language models (LLMs), models that focus on certain domains and languages have been discussed for their necessity. There is also a growing need for benchmarks t...

Option pricing, a fundamental problem in finance, often requires solving non-linear partial differential equations (PDEs). When dealing with multi-asset options, such as rainbow options, these PDEs ...

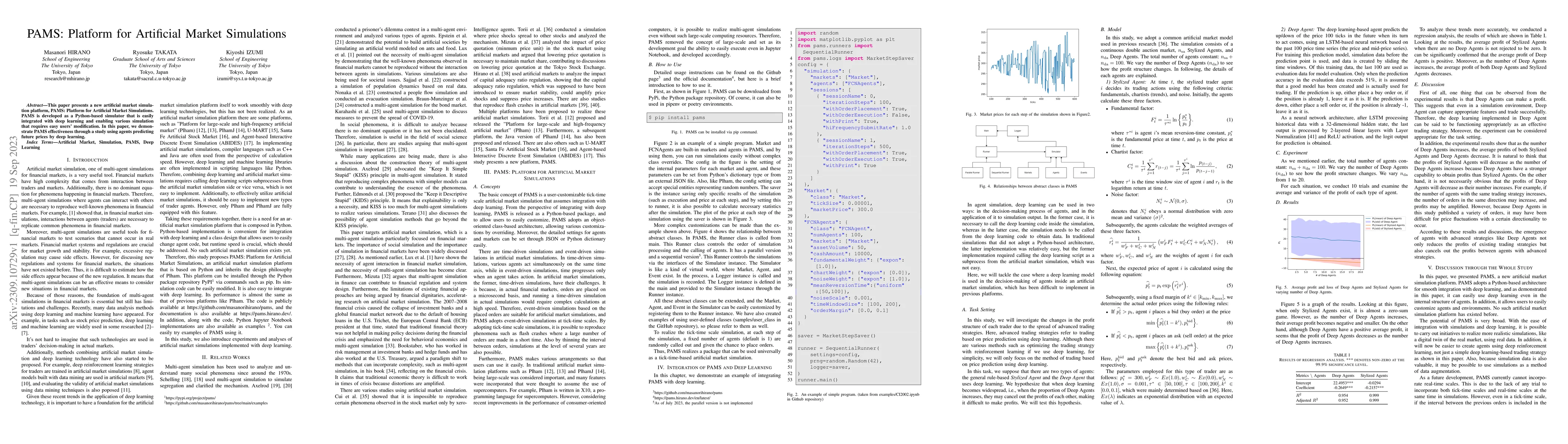

This paper presents a new artificial market simulation platform, PAMS: Platform for Artificial Market Simulations. PAMS is developed as a Python-based simulator that is easily integrated with deep l...

Instruction tuning is essential for large language models (LLMs) to become interactive. While many instruction tuning datasets exist in English, there is a noticeable lack in other languages. Also, ...

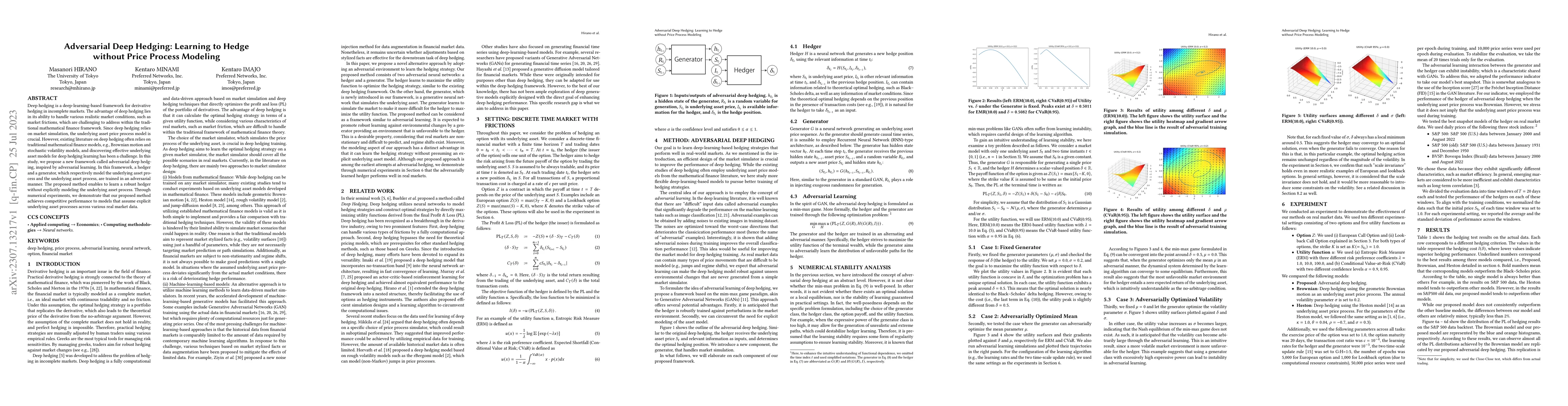

Deep hedging is a deep-learning-based framework for derivative hedging in incomplete markets. The advantage of deep hedging lies in its ability to handle various realistic market conditions, such as...

This study constructed a Japanese chat dataset for tuning large language models (LLMs), which consist of about 8.4 million records. Recently, LLMs have been developed and gaining popularity. However...

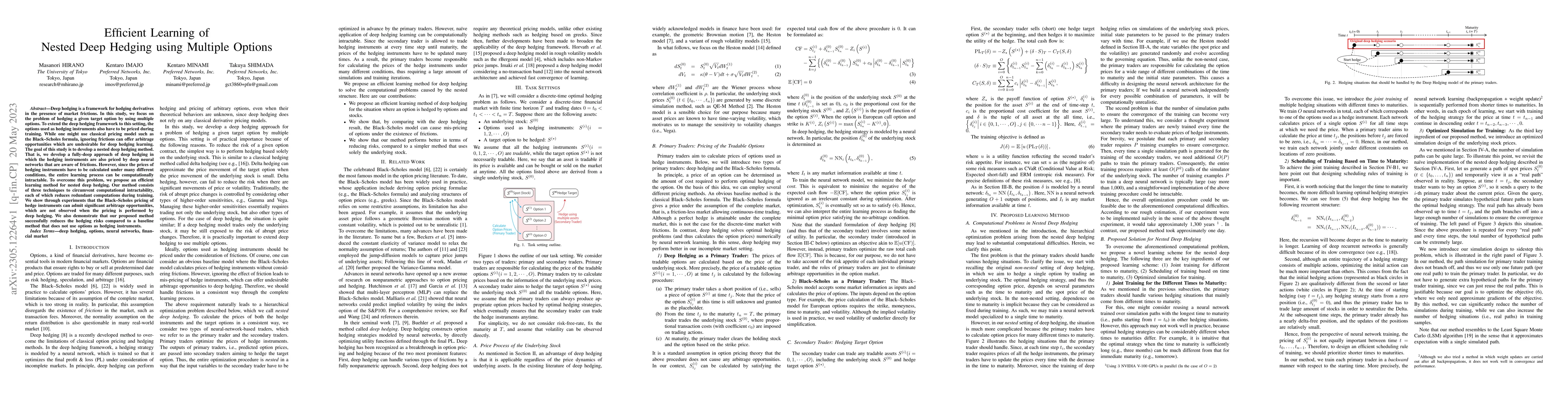

Deep hedging is a framework for hedging derivatives in the presence of market frictions. In this study, we focus on the problem of hedging a given target option by using multiple options. To extend ...

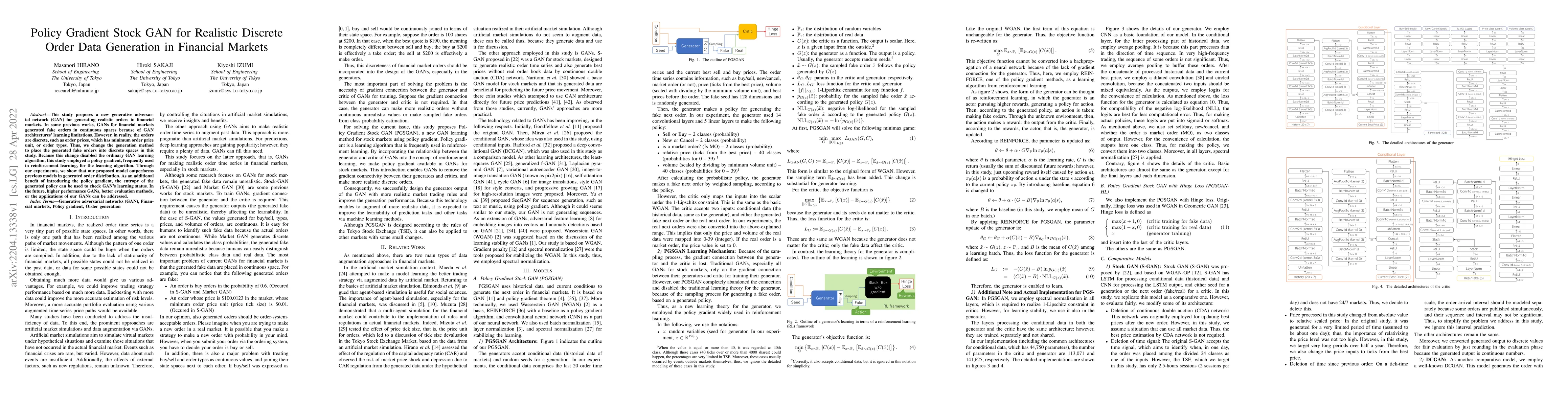

This study proposes a new generative adversarial network (GAN) for generating realistic orders in financial markets. In some previous works, GANs for financial markets generated fake orders in conti...

The AI traders in financial markets have sparked significant interest in their effects on price formation mechanisms and market volatility, raising important questions for market stability and regulat...

This paper proposes a novel method for constructing instruction-tuned large language models (LLMs) for finance without instruction data. Traditionally, developing such domain-specific LLMs has been re...

The domain adaptation of language models, including large language models (LLMs), has become increasingly important as the use of such models continues to expand. This study demonstrates the effective...

Inspired by the recently proposed Kolmogorov-Arnold Networks (KANs), we introduce the KAN-based Option Pricing (KANOP) model to value American-style options, building on the conventional Least Square ...

This study aims to evaluate the sentiment of financial texts using large language models~(LLMs) and to empirically determine whether LLMs exhibit company-specific biases in sentiment analysis. Specifi...

Large models have shown unprecedented capabilities in natural language processing, image generation, and most recently, time series forecasting. This leads us to ask the question: treating market pric...

Evaluating the open-ended text generation of large language models (LLMs) is challenging because of the lack of a clear ground truth and the high cost of human or LLM-based assessments. We propose a n...

Accurately forecasting central bank policy decisions, particularly those of the Federal Open Market Committee(FOMC) has become increasingly important amid heightened economic uncertainty. While prior ...

High-dimensional option pricing and hedging present significant challenges in quantitative finance, where traditional PDE-based methods struggle with the curse of dimensionality. The BSDE framework of...

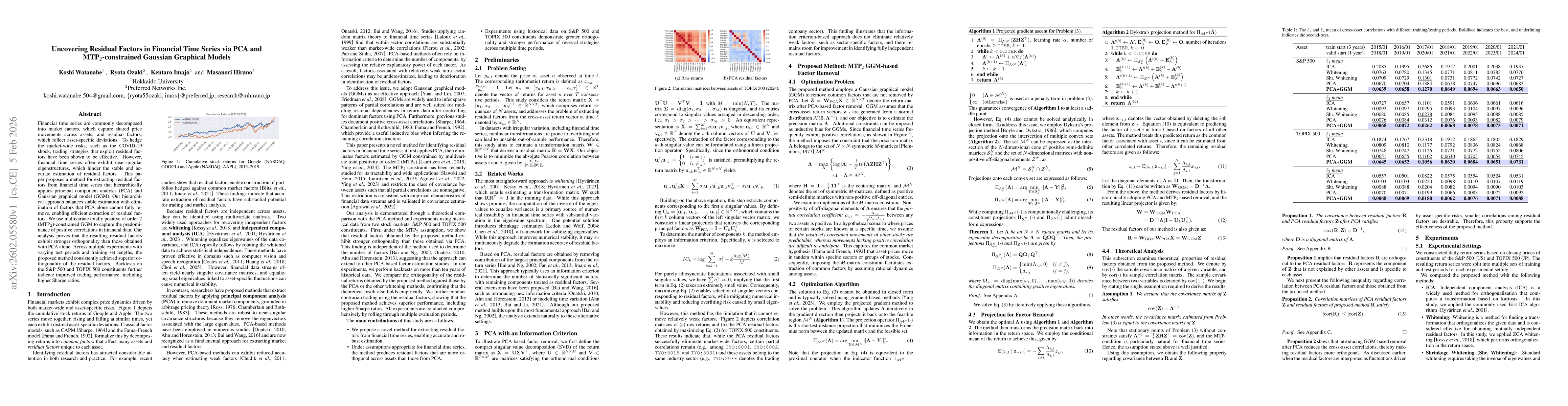

Financial time series are commonly decomposed into market factors, which capture shared price movements across assets, and residual factors, which reflect asset-specific deviations. To hedge the marke...