Academic Profile

Statistics

Similar Authors

Papers on arXiv

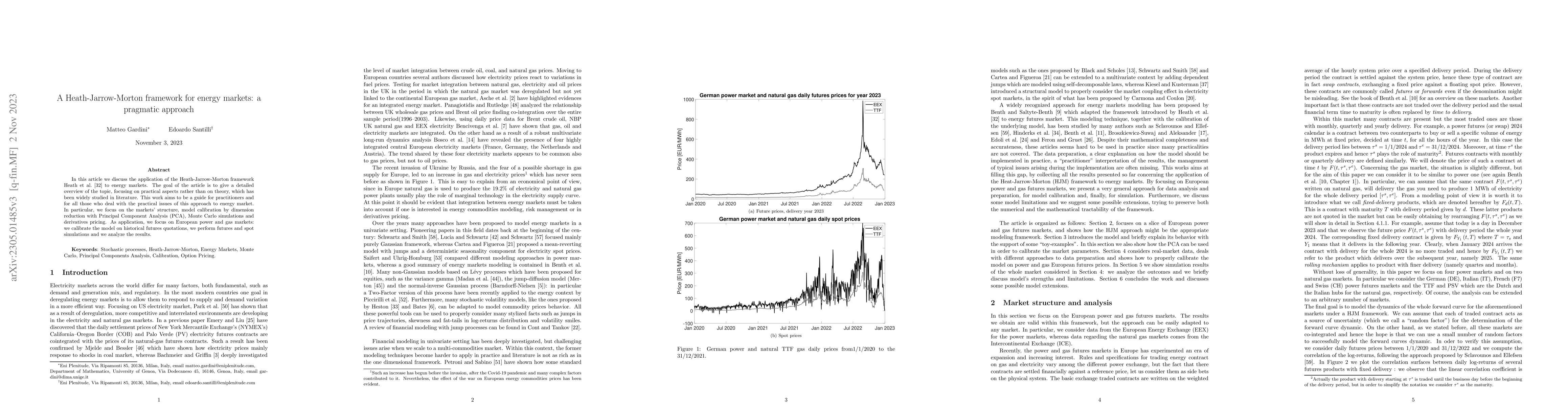

In this article we discuss the application of the Heath-Jarrow-Morton framework Heath et al. [26] to energy markets. The goal of the article is to give a detailed overview of the topic, focusing on ...

In this article we focus on the pricing of exchange options when the dynamic of logprices follows either the well-known variance gamma or the recent variance gamma++ process introduced in Gardini et...

Using the concept of self-decomposable subordinators introduced in Gardini et al. [11], we build a new bivariate Normal Inverse Gaussian process that can capture stochastic delays. In addition, we a...

A definition of a quantum vertex algebra, which is a deformation of a vertex algebra, was proposed by Etingof and Kazhdan in 1998. In a nutshell, a quantum vertex algebra is a braided state-field co...