Academic Profile

Statistics

Similar Authors

Papers on arXiv

Reduced-rank (RR) regression may be interpreted as a dimensionality reduction technique able to reveal complex relationships among the data parsimoniously. However, RR regression models typically ov...

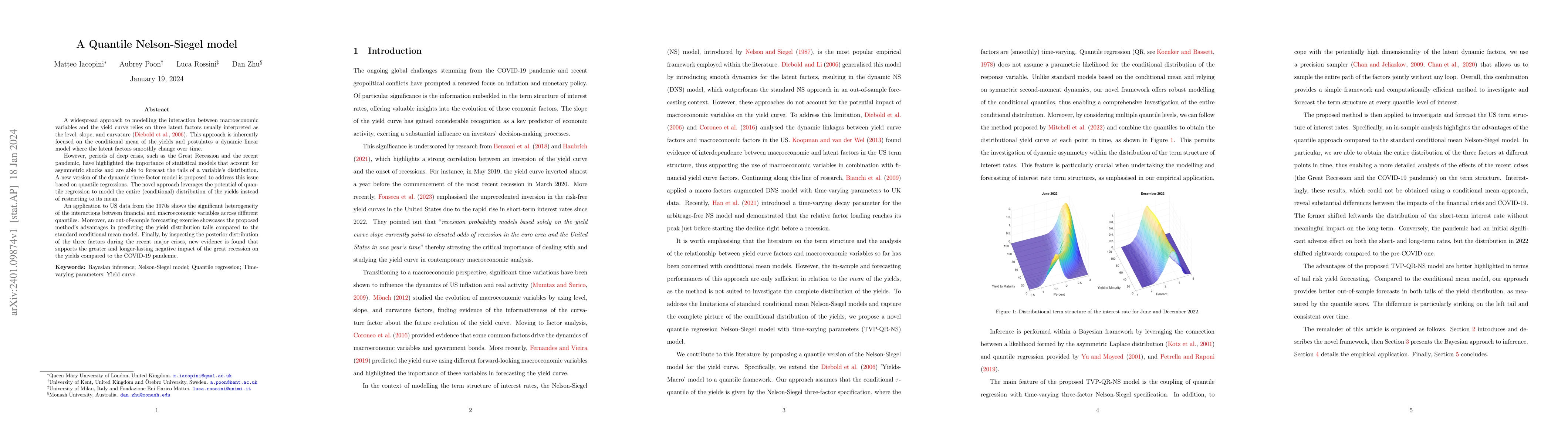

A widespread approach to modelling the interaction between macroeconomic variables and the yield curve relies on three latent factors usually interpreted as the level, slope, and curvature (Diebold ...

The spatial autoregressive (SAR) model is extended by introducing a Markov switching dynamics for the weight matrix and spatial autoregressive parameter. The framework enables the identification of ...

A novel spatial autoregressive model for panel data is introduced, which incorporates multilayer networks and accounts for time-varying relationships. Moreover, the proposed approach allows the stru...

Ranking lists are often provided at regular time intervals by one or multiple rankers in a range of applications, including sports, marketing, and politics. Most popular methods for rank-order data ...

A new discrete-time shot noise Cox process for spatiotemporal data is proposed. The random intensity is driven by a dependent sequence of latent gamma random measures. Some properties of the latent ...

An innovative method is proposed to construct a quantile dependence system for inflation and money growth. By considering all quantiles and leveraging a novel notion of quantile sensitivity, the met...

Reduced-rank regression recognises the possibility of a rank-deficient matrix of coefficients. We propose a novel Bayesian model for estimating the rank of the coefficient matrix, which obviates the...

This article proposes a novel Bayesian multivariate quantile regression to forecast the tail behavior of US macro and financial indicators, where the homoskedasticity assumption is relaxed to allow ...

Timely characterizations of risks in economic and financial systems play an essential role in both economic policy and private sector decisions. However, the informational content of low-frequency v...

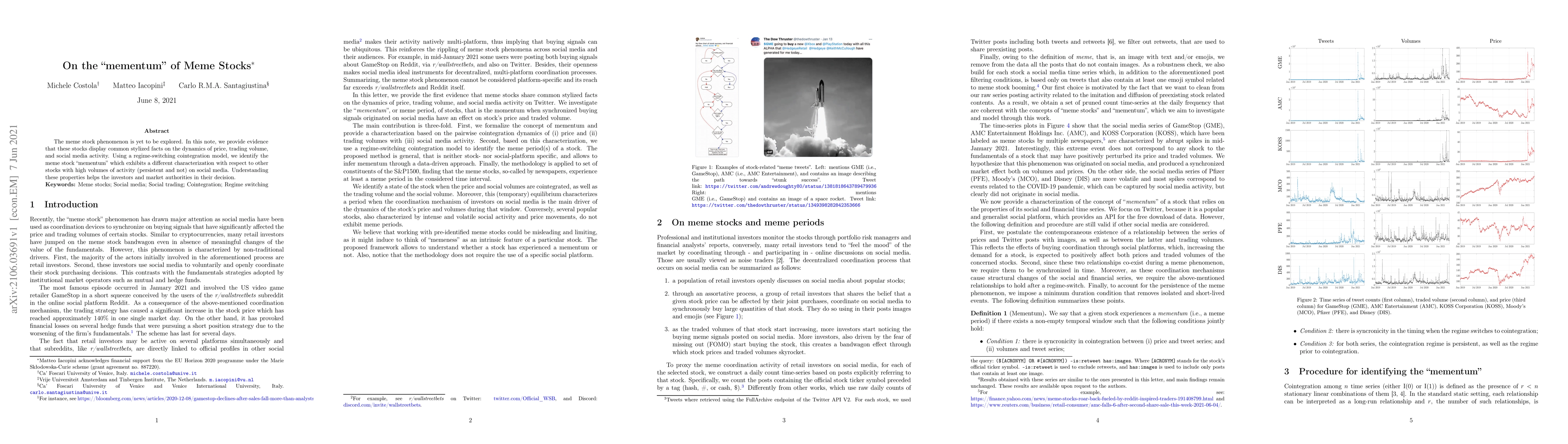

The meme stock phenomenon is yet to be explored. In this note, we provide evidence that these stocks display common stylized facts on the dynamics of price, trading volume, and social media activity...

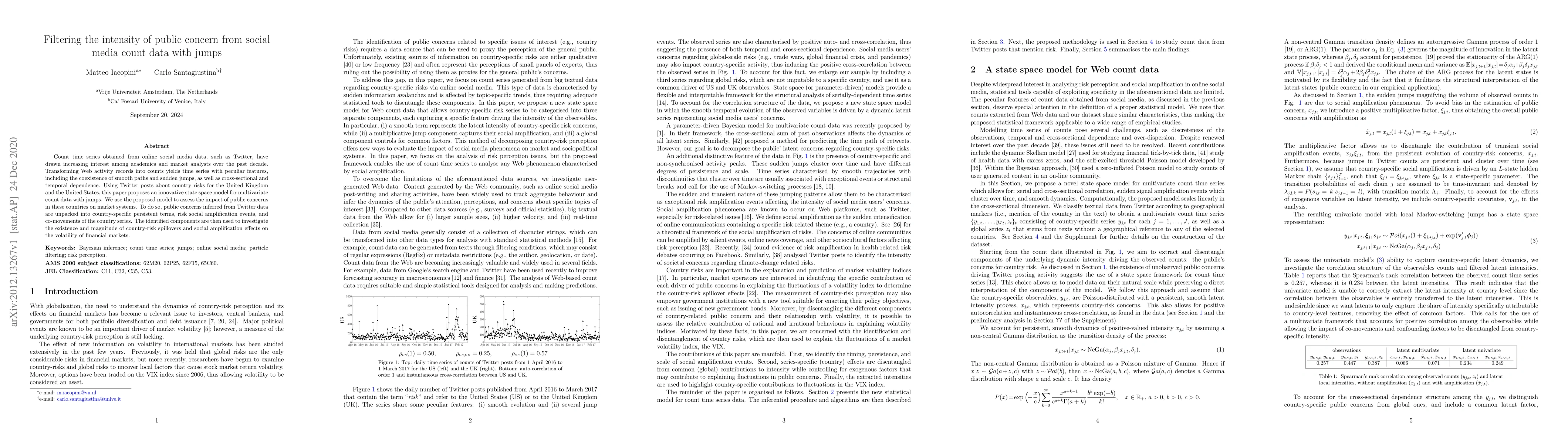

Count time series obtained from online social media data, such as Twitter, have drawn increasing interest among academics and market analysts over the past decade. Transforming Web activity records ...

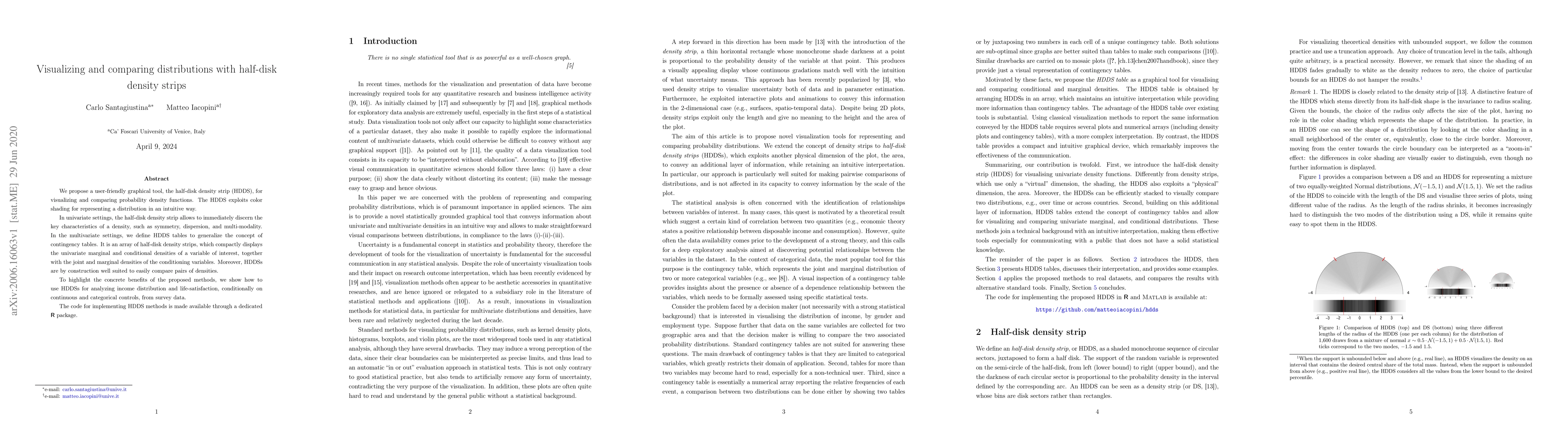

We propose a user-friendly graphical tool, the half-disk density strip (HDDS), for visualizing and comparing probability density functions. The HDDS exploits color shading for representing a distrib...

This paper proposes a novel asymmetric continuous probabilistic score (ACPS) for evaluating and comparing density forecasts. It extends the proposed score and defines a weighted version, which empha...

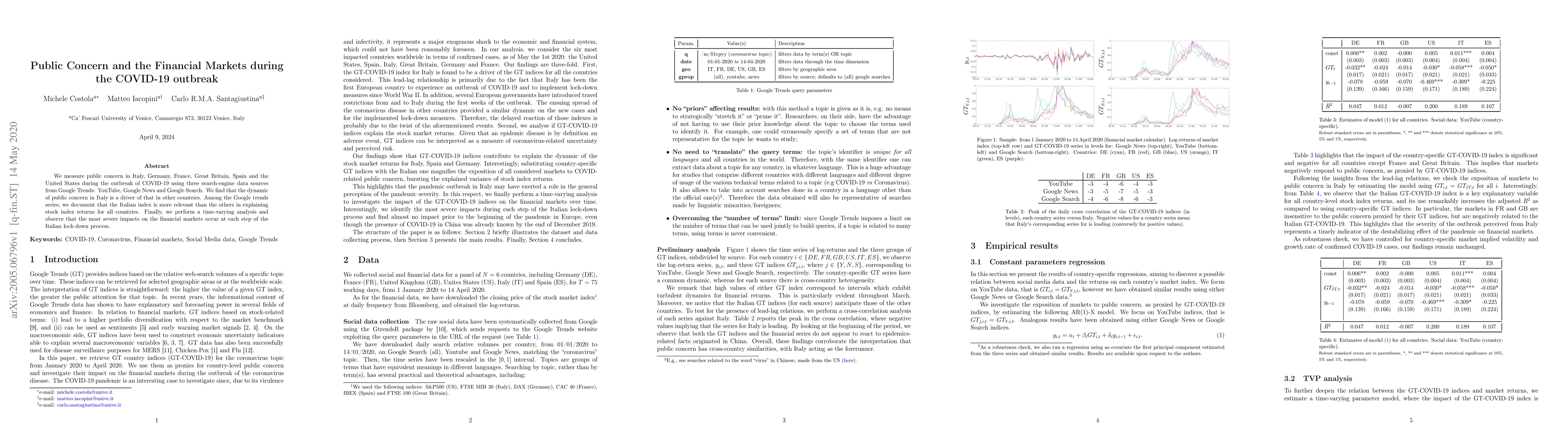

We measure the public concern during the outbreak of COVID-19 disease using three data sources from Google Trends (YouTube, Google News, and Google Search). Our findings are three-fold. First, the p...

Over the last decade, big data have poured into econometrics, demanding new statistical methods for analysing high-dimensional data and complex non-linear relationships. A common approach for addres...

We propose a new Bayesian Markov switching regression model for multidimensional arrays (tensors) of binary time series. We assume a zero-inflated logit regression with time-varying parameters and a...

Tensor-valued data are becoming increasingly available in economics and this calls for suitable econometric tools. We propose a new dynamic linear model for tensor-valued response variables and cova...

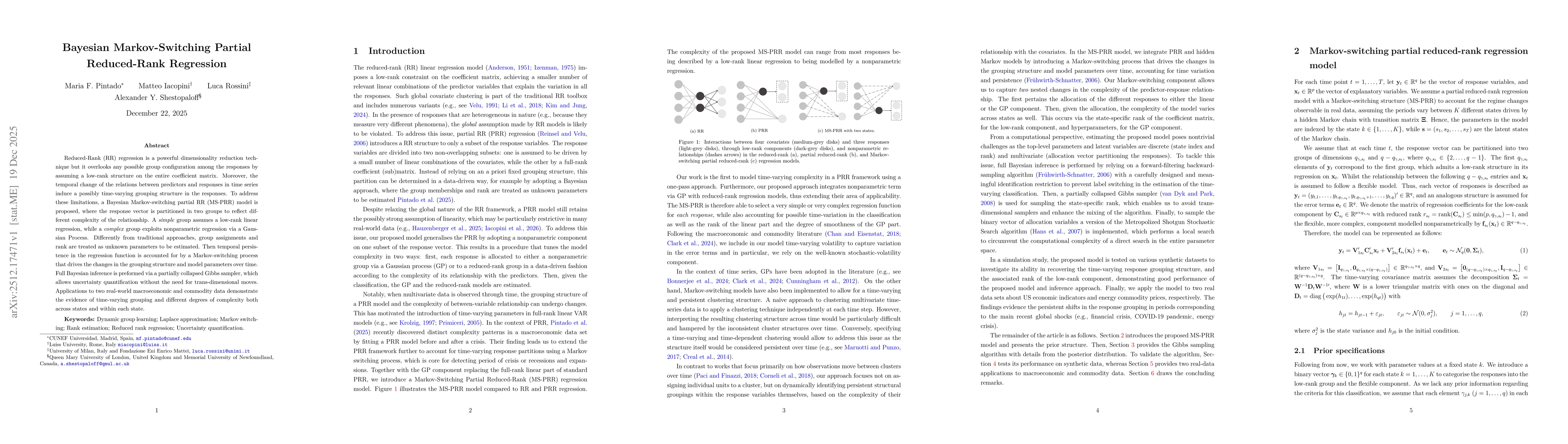

Reduced-Rank (RR) regression is a powerful dimensionality reduction technique but it overlooks any possible group configuration among the responses by assuming a low-rank structure on the entire coeff...

A new dynamic latent space eigenmodel (LSM) is proposed for weighted temporal networks. The model accommodates integer-valued weights, excess of zeros, time-varying node positions (features), and time...