Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper develops a method to upper-bound extreme-values of time-windowed risks for stochastic processes. Examples of such risks include the maximum average or 90% quantile of the current along a ...

Recently a moment-sum-of-squares hierarchy for exit location estimation of stochastic processes has been presented. When restricting to the special case of the unit ball, we show that the solutions ...

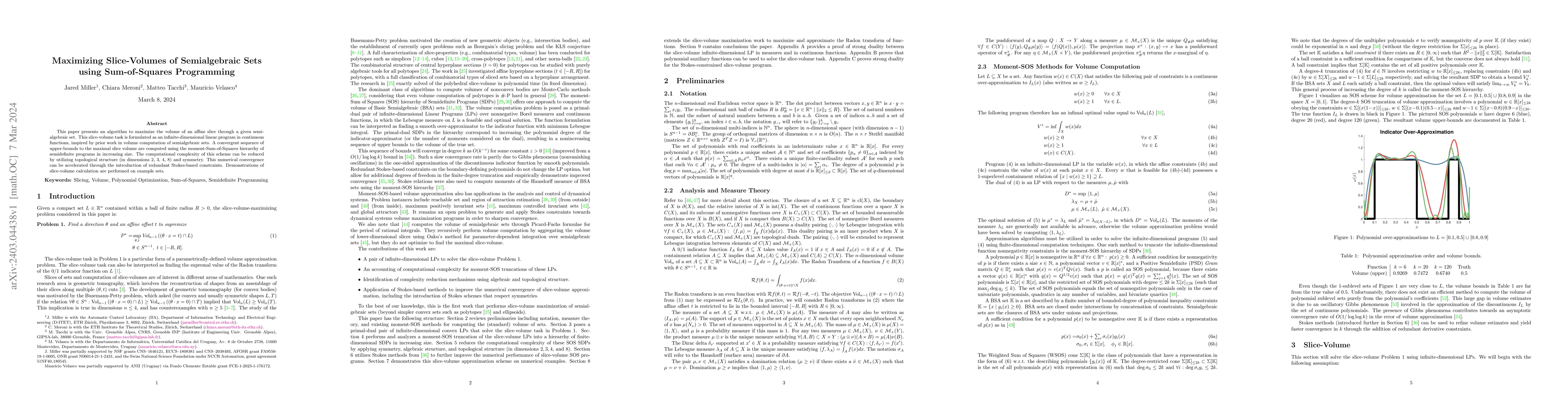

This paper presents an algorithm to maximize the volume of an affine slice through a given semialgebraic set. This slice-volume task is formulated as an infinite-dimensional linear program in contin...

We introduce a comprehensive framework for analyzing convergence rates for infinite dimensional linear programming problems (LPs) within the context of the moment-sum-of-squares hierarchy. Our prima...

This paper proposes an algorithm to calculate the maximal probability of unsafety with respect to trajectories of a stochastic process and a hazard set. The unsafe probability estimation problem is ...

We address the problem of computing a control for a time-dependent nonlinear system to reach a target set in a minimal time. To solve this minimal time control problem, we introduce a hierarchy of l...

This paper presents a new Matlab toolbox, aimed at facilitating the use of polynomial optimization for stability analysis of nonlinear systems. In the past decade several decisive contributions made...

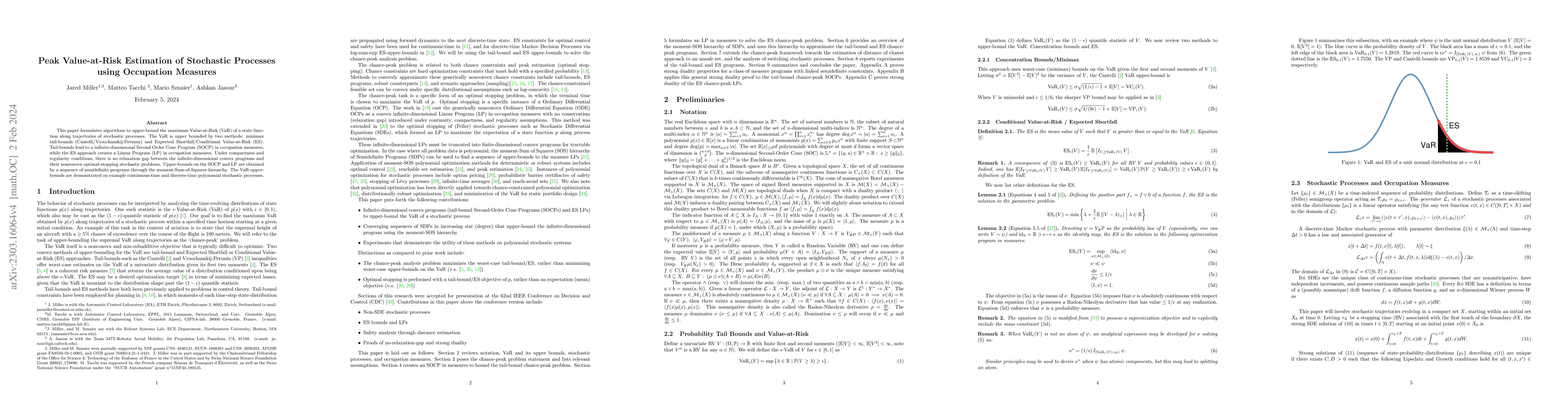

This paper formulates algorithms to upper-bound the maximum Value-at-Risk (VaR) of a state function along trajectories of stochastic processes. The VaR is upper bounded by two methods: minimax tail-...

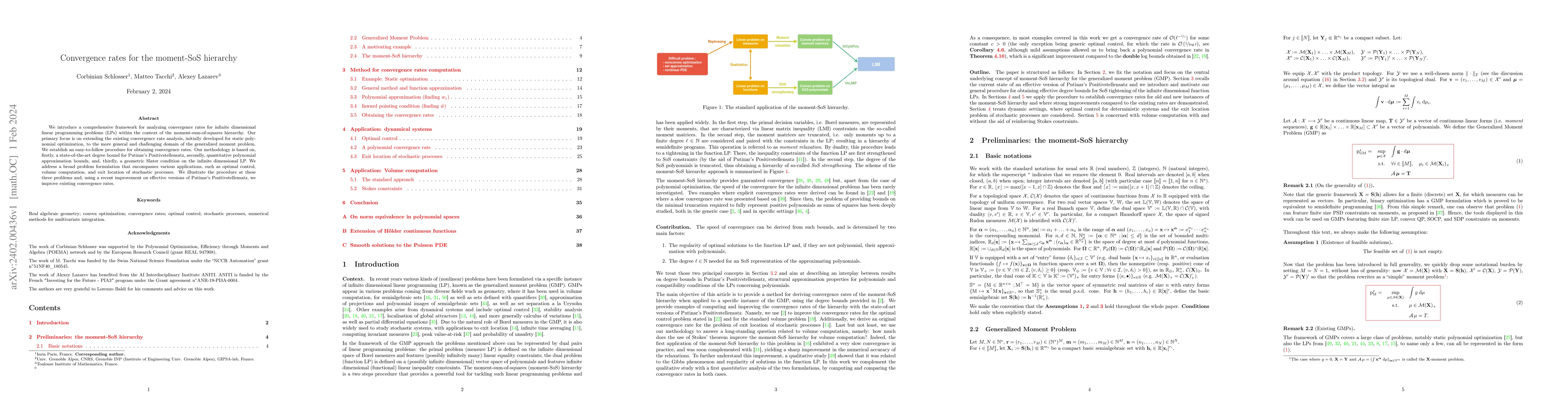

Lasserre's moment-SOS hierarchy consists of approximating instances of the generalized moment problem (GMP) with moment relaxations and sums-of-squares (SOS) strenghtenings that boil down to convex ...

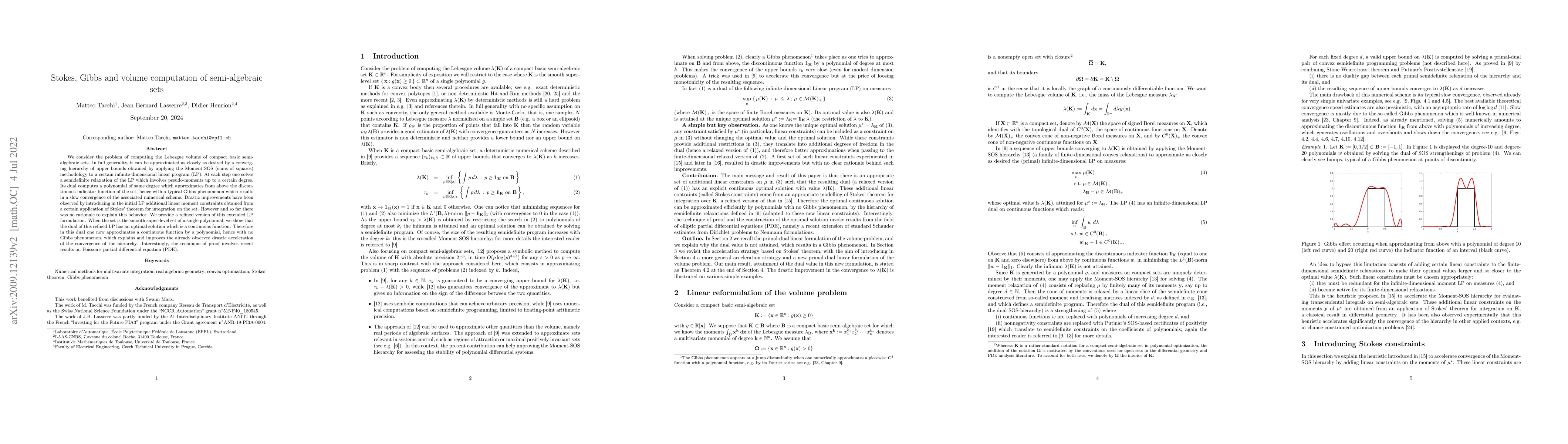

We consider the problem of computing the Lebesgue volume of compact basic semi-algebraic sets. In full generality, it can be approximated as closely as desired by a converging hierarchy of upper bou...

The Lasserre or moment-sum-of-square hierarchy of linear matrix inequality relaxations is used to compute inner approximations of the maximal positively invariant set for continuous-time dynamical s...

We provide a systematic deterministic numerical scheme to approximate the volume (i.e. the Lebesgue measure) of a basic semi-algebraic set whose description follows a sparsity pattern. As in previou...

This work presents a stochastic tube-based model predictive control framework that guarantees hard input constraint satisfaction for linear systems subject to unbounded additive disturbances. The appr...