Academic Profile

Statistics

Similar Authors

Papers on arXiv

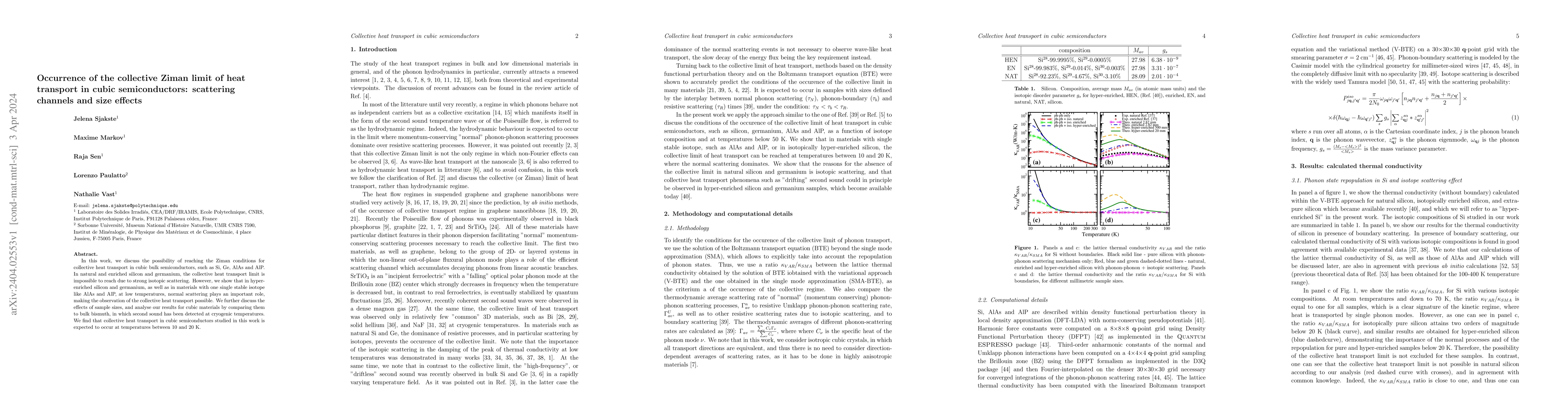

In this work, we discuss the possibility of reaching the Ziman conditions for collective heat transport in cubic bulk semiconductors, such as Si, Ge, AlAs and AlP. In natural and enriched silicon an...

In this paper, we explore the portfolio allocation problem involving an uncertain covariance matrix. We calculate the expected value of the Constant Absolute Risk Aversion (CARA) utility function, m...

In this paper, we revisit the relationship between investors' utility functions and portfolio allocation rules. We derive portfolio allocation rules for asymmetric Laplace distributed $ALD(\mu,\sigm...

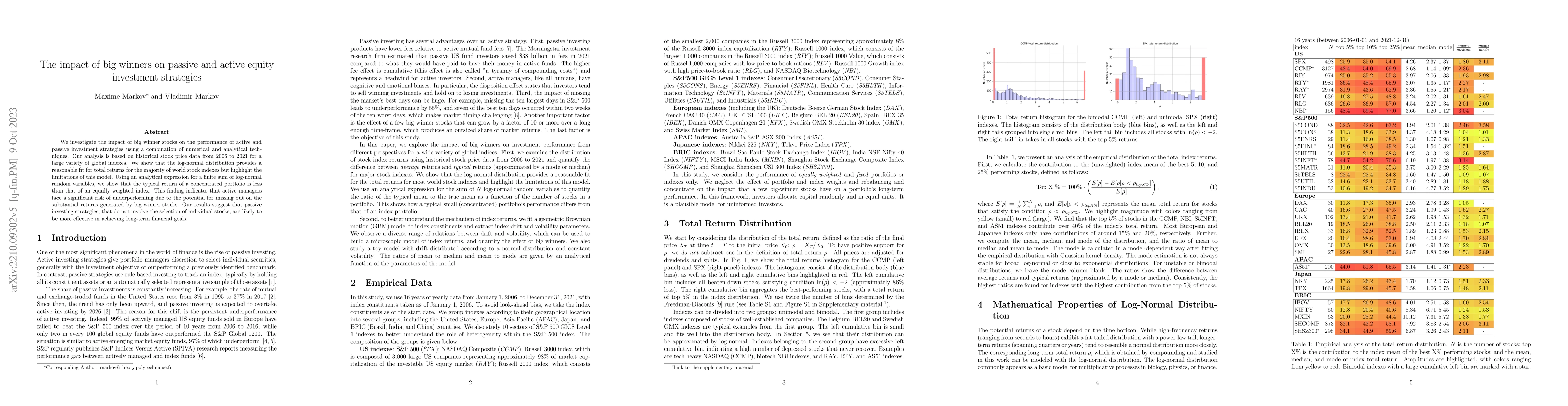

We investigate the impact of big winner stocks on the performance of active and passive investment strategies using a combination of numerical and analytical techniques. Our analysis is based on his...

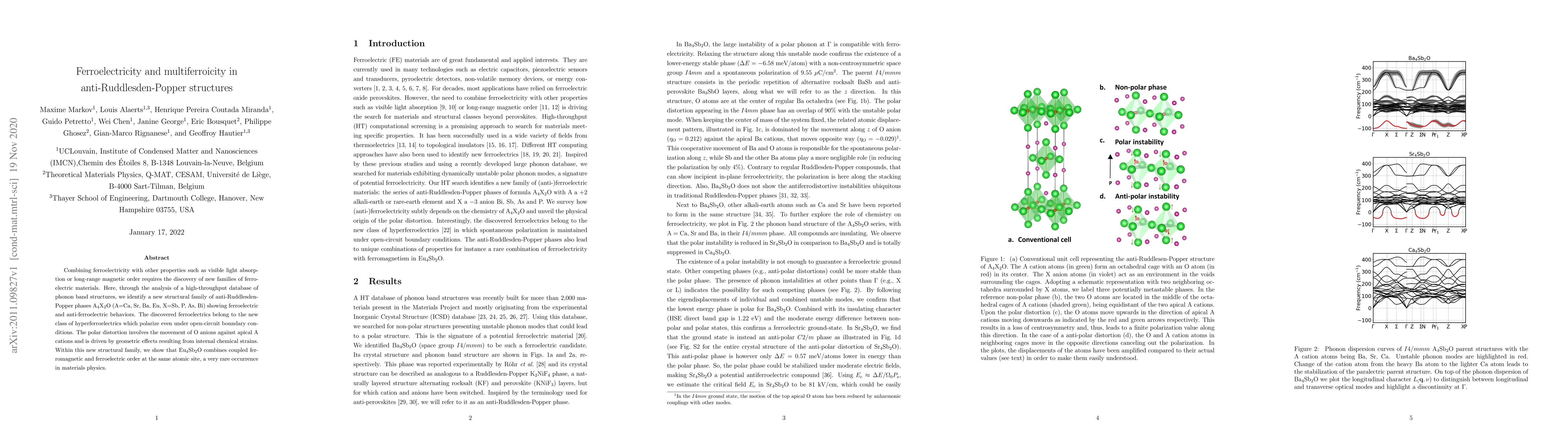

Combining ferroelectricity with other properties such as visible light absorption or long-range magnetic order requires the discovery of new families of ferroelectric materials. Here, through the an...

Heavily doped semiconductors are by far the most studied class of materials for thermoelectric applications in the past several decades. They have Seebeck coefficient values which are 2-3 orders of ...