Academic Profile

Statistics

Similar Authors

Papers on arXiv

We identify a new type of risk, common firm-level investor fears, from commonalities within the cross-sectional distribution of individual stock options. We define firm-level fears that link with up...

This paper characterises dynamic linkages arising from shocks with heterogeneous degrees of persistence. Using frequency domain techniques, we introduce measures that identify smoothly varying links...

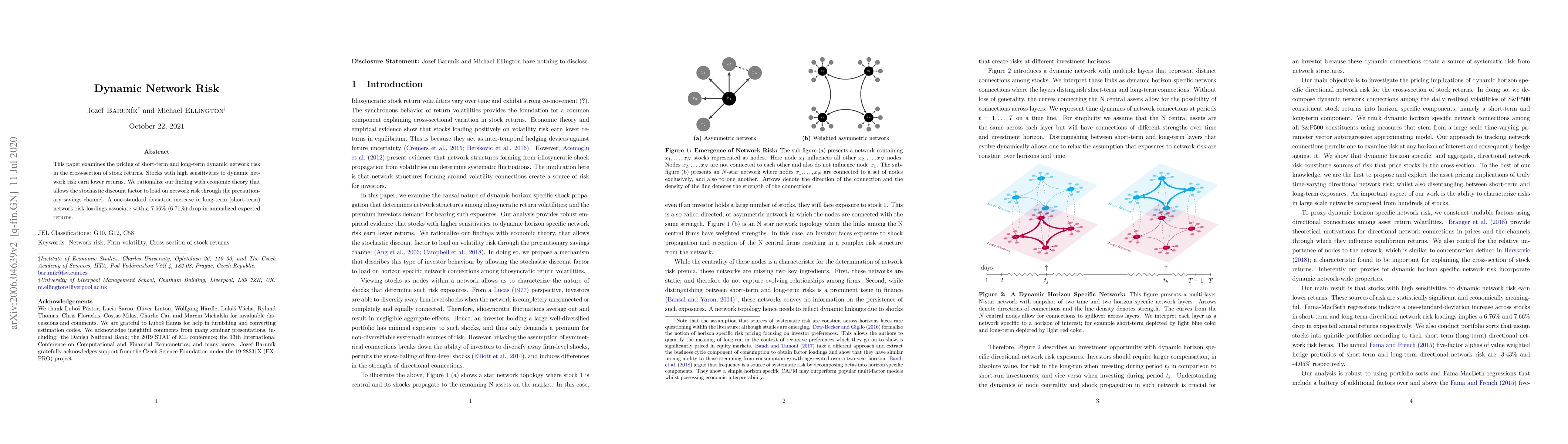

This paper examines the pricing of short-term and long-term dynamic network risk in the cross-section of stock returns. Stocks with high sensitivities to dynamic network risk earn lower returns. We ...