Academic Profile

Statistics

Similar Authors

Papers on arXiv

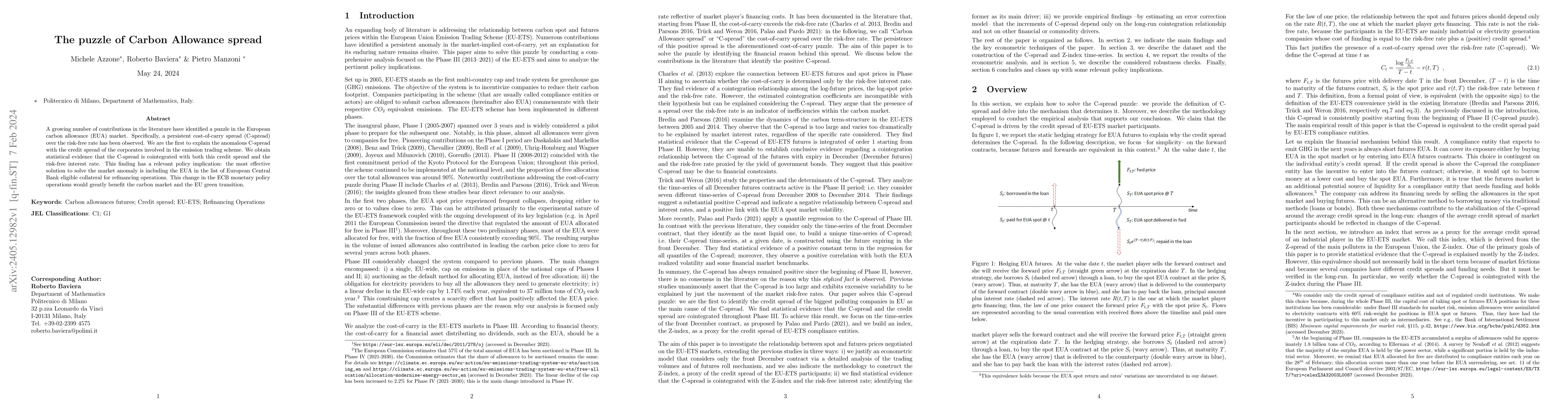

A growing number of contributions in the literature have identified a puzzle in the European carbon allowance (EUA) market. Specifically, a persistent cost-of-carry spread (C-spread) over the risk-f...

We investigate the portfolio frontier and risk premia in equilibrium when an institutional investor aims to minimize the tracking error variance and to attain an ESG score higher than the benchmark'...

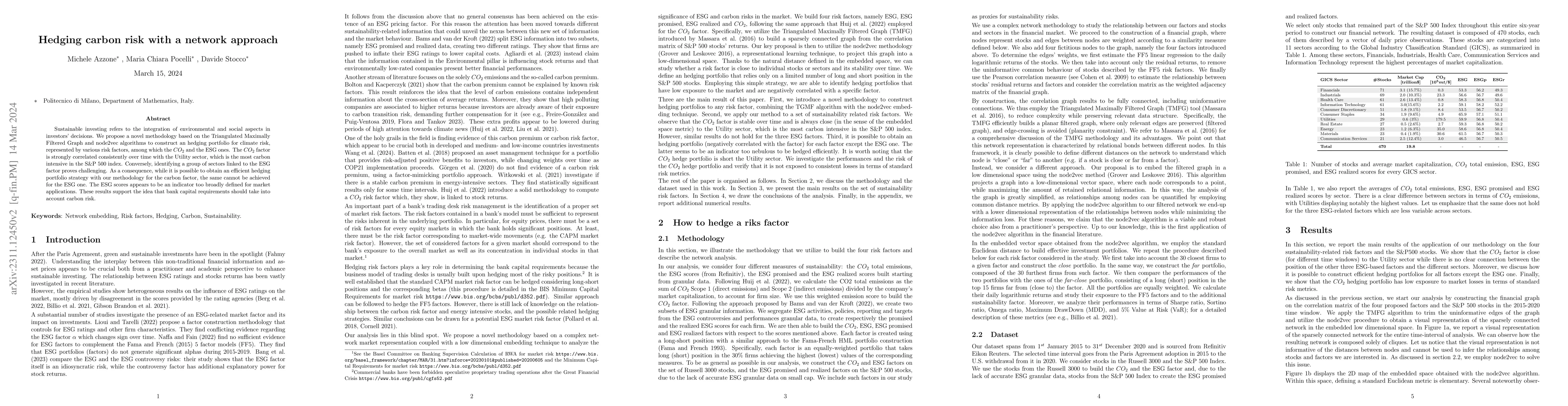

Sustainable investing refers to the integration of environmental and social aspects in investors' decisions. We propose a novel methodology based on the Triangulated Maximally Filtered Graph and nod...

Monroe (1978) demonstrates that any local semimartingale can be represented as a time-changed Brownian Motion (BM). A natural question arises: does this representation theorem hold when the BM and t...

In this paper, we present a very fast Monte Carlo scheme for additive processes: the computational time is of the same order of magnitude of standard algorithms for Brownian motions. We analyze in d...

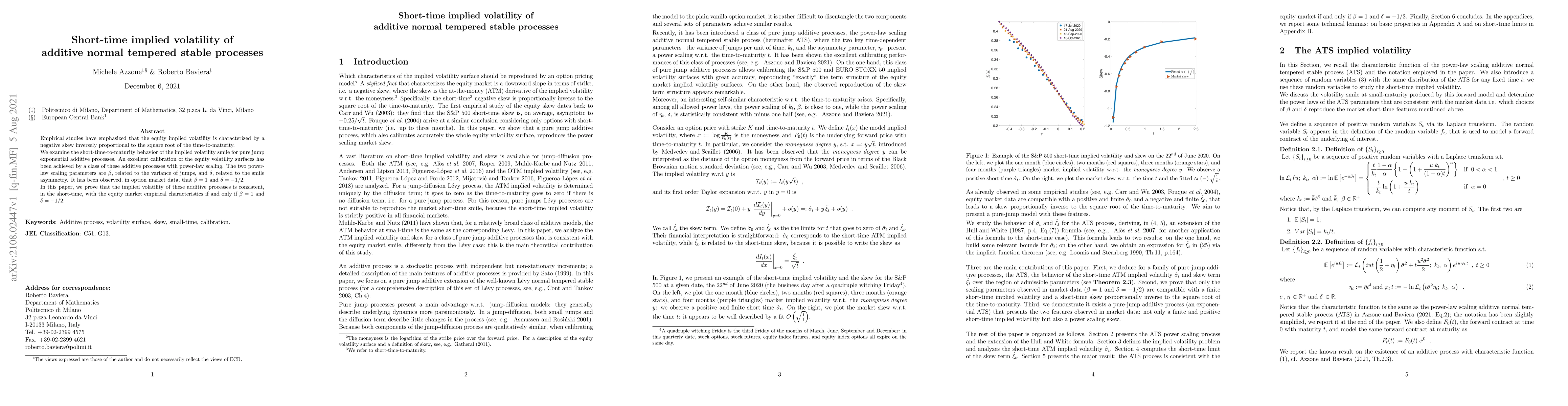

Empirical studies have emphasized that the equity implied volatility is characterized by a negative skew inversely proportional to the square root of the time-to-maturity. We examine the short-time-...

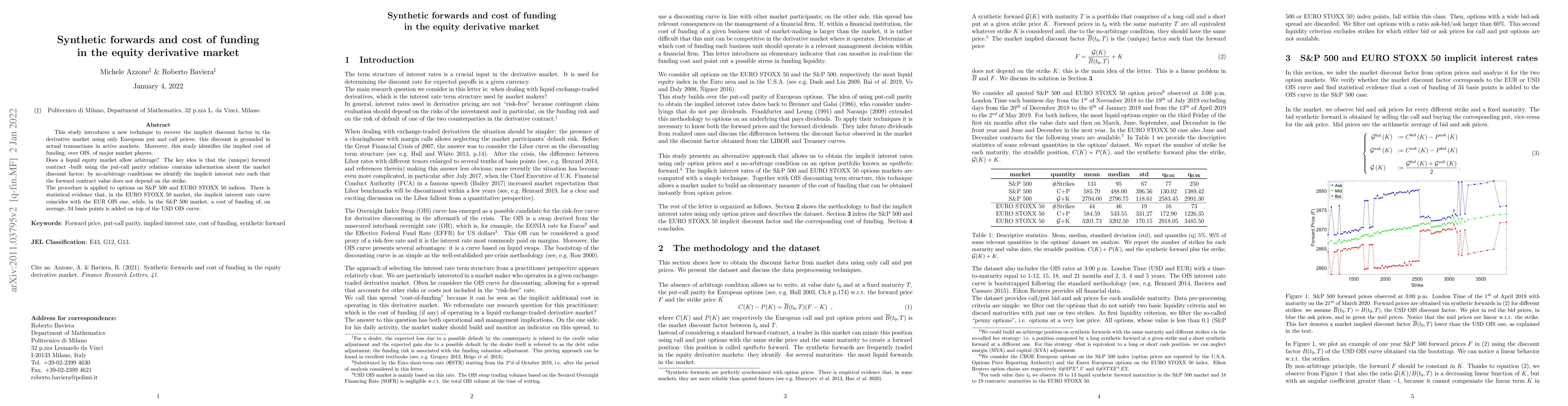

This study introduces a new technique to recover the implicit discount factor in the derivative market using only European put and call prices: this discount is grounded in actual transactions in ac...

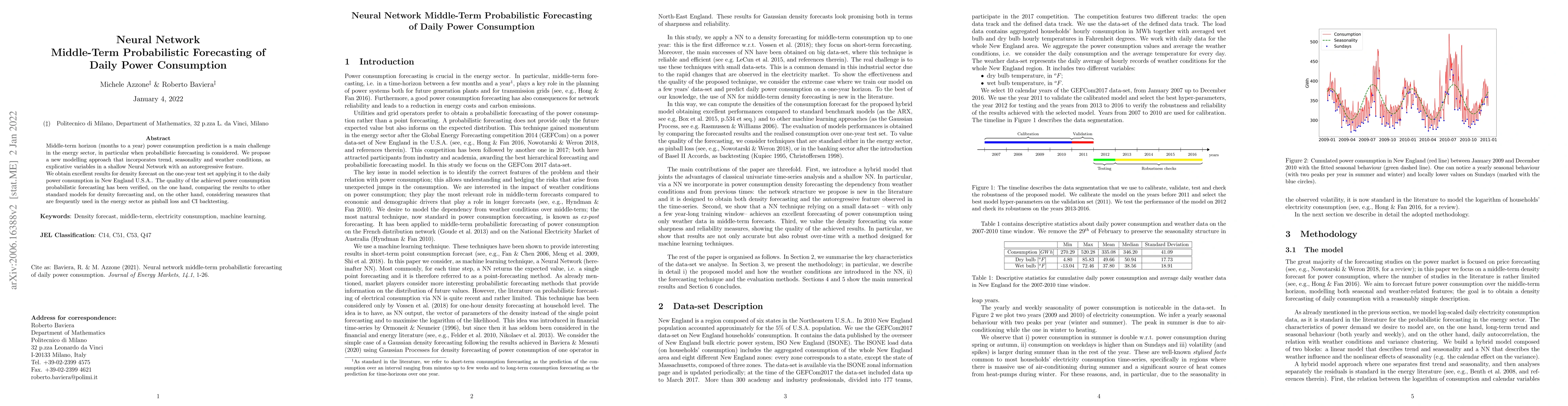

Middle-term horizon (months to a year) power consumption prediction is a main challenge in the energy sector, in particular when probabilistic forecasting is considered. We propose a new modelling a...

We introduce a simple model for equity index derivatives. The model generalizes well known L\`evy Normal Tempered Stable processes (e.g. NIG and VG) with time dependent parameters. It accurately fit...

Climate-related phenomena are increasingly affecting regions worldwide, manifesting as floods, water scarcity, and heat waves, which can significantly impair companies' assets and productivity. We dev...

We analyse financial stability and welfare impacts associated with the introduction of a Central Bank Digital Currency (CBDC) in a macroeconomic agent-based model. The model considers firms, banks, an...

Driven by the increasing frequency and intensity of natural disasters and chronic climate threats, we investigate the impact of physical climate risk on global equity portfolios. By employing a panel ...